A conflict of interest arises when an advisor has a personal, business, or financial interest that could influence their advice and motivate them to make decisions that are not in the best interests of their clients. A typical case of conflict of interest is when advisors make money from equity product sales and receive commissions from them. Conflicts of interest concern financial advising because they can result in biased investment advice. As this information is rarely voluntarily disclosed by advisors, it is prudent for clients to ask the right questions to help them assess if the advisor can truly help them meet their financial goals. Choosing financial advisors with fiduciary duties can minimize exposure to conflicts of interest. Conflict of interest can arise in financial advising in various ways, with potential consequences for investors. The most common types of conflicts include: Conflicts of interest may arise when investments are managed on a commission basis. Examples include allocating investment opportunities to proprietary accounts and accounts that offer performance fees. Another case is when investments are selected because the firm or its employees get an additional financial benefit. Furthermore, they may get to vote on company proxies in a way that affects any associated business arrangements. Financial advisors who trade stocks and securities on behalf of clients may be incentivized to place trades that generate additional fees for themselves. Such could lead to excessive trading or other unnecessary transactions. It may also take the form of trading in personal accounts based on knowledge of client trading and non-public material information. Financial advisors occasionally evaluate private investments at cost rather than carrying out the necessary research to support the value. Incentives or extra services may also be provided by advisors to clients who have larger assets under control. Solicitation arrangements may occur when advisors attempt to receive higher commissions or sales rewards from companies to market specific products. They might also incentivize current clients with lower fees for referring potential clients to the firm. Advisors and employees at advisory firms should note that any activities outside of consulting must adhere to ethical standards. Such activities relate to gifts, entertainment, family business involvement, political contributions, and third-party endorsements. Below are some examples when a conflict of interest might arise when working with a financial advisor: Example 1 A financial advisor charges 0.75% to manage a client's portfolio. The advisor will earn about $22,500 for the first year from a client with $3,000,000 in assets. On the other hand, the advisor may earn referral fees from a business partner's company, and will get a one-time payment of $30,000 for every $5,000,000 referred. This partner company charges the client 1.25% and the advisor is close to reaching the $5,000,000 benchmark in solicitation arrangement. A conflict of interest arises because the financial advisor has an incentive to recommend the partner company’s services despite it being more expensive for the client. Example 2 A securities commission uncovered a case at a certain security company where the company was unable to produce telephone order records for one of its clients. It was eventually revealed that the account executive had been given verbal authorization to make trades on behalf of the client. The company then explained that they had not detected any misconduct since the client and the executive were not part of their sample check each month which only included 10 trades. The commission judged that such low-frequency review could not detect irregularities The commission further discovered that the company did not successfully enforce its policy to prevent conflicts of interest between its research reports and its investment banking relationships. The company did not sufficiently reveal its connection with a listed company. Securities and Exchange Commission (SEC) The SEC is the primary regulatory body overseeing the U.S. securities markets, responsible for enforcing federal securities laws, regulating the industry, and protecting investors. The SEC works to ensure that conflicts of interest are identified, disclosed, and managed to maintain market integrity. FINRA is a self-regulatory organization that oversees brokerage firms and their registered representatives in the United States. It establishes rules and guidelines to protect investors and maintain market integrity, including requirements related to conflicts of interest. Dodd-Frank Wall Street Reform and Consumer Protection Act The Dodd-Frank Act, enacted in response to the 2008 financial crisis, introduced several provisions to address conflicts of interest in the financial industry. These include the Volcker Rule, which limits proprietary trading by banks, and provisions requiring enhanced disclosures and the establishment of internal controls to manage conflicts of interest. Sarbanes-Oxley Act The Sarbanes-Oxley Act, passed in 2002 following a series of corporate scandals, established new corporate governance standards and strengthened financial reporting requirements. Among its provisions are rules related to auditor independence and the disclosure of financial conflicts of interest, aimed at preventing fraud and improving the reliability of financial statements. Fiduciary Duty Standards Fiduciary duty standards require financial professionals to act in the best interest of their clients, putting clients' interests above their own. These standards, which vary depending on the type of financial professional and the jurisdiction, help to mitigate conflicts of interest and ensure that financial advice is objective and unbiased. The Enron scandal, which came to light in 2001, involved a complex web of conflicts of interest, including self-dealing by executives and the failure of the company's auditor, Arthur Andersen, to maintain independence. The scandal led to the collapse of Enron, one of the largest bankruptcies in U.S. history, and significant changes to corporate governance and financial reporting regulations. In 2010, Goldman Sachs faced allegations of conflict of interest related to its marketing of a collateralized debt obligation (CDO) called Abacus 2007-AC1. The SEC claimed that Goldman Sachs failed to disclose to investors that the CDO was structured by a hedge fund that had taken a short position in the underlying securities, betting that they would lose value. The case resulted in a $550 million settlement and heightened scrutiny of conflicts of interest on Wall Street. Bernie Madoff's massive Ponzi scheme, uncovered in 2008, involved numerous conflicts of interest, including self-dealing and the use of affiliated companies to perpetrate the fraud. The scheme, which resulted in an estimated $65 billion in losses for investors, led to Madoff's conviction and life imprisonment, as well as increased regulatory attention to conflicts of interest and the need for stronger oversight of investment managers. Investors seeking information on financial advisors' conflicts of interest have several resources available. They should always do their due diligence when choosing a financial advisor to ensure they get the best advice possible. Financial advisors disclose potential conflicts of interest on their firm's website. Investors can review the firm's disclosure policy to learn more about potential conflicts of interest. The Securities and Exchange Commission (SEC) maintains a database of investment advisors through Form ADVs, which includes information on potential conflicts of interest. This can be accessed through the SEC's Investment Adviser Public Disclosure (IAPD) website. Financial Industry Regulatory Authority (FINRA) is a regulatory organization that oversees the securities industry. Investors can check FINRA's BrokerCheck website to see if a financial advisor has any disciplinary history or conflicts of interest. Some states also have their own securities regulators who maintain databases of financial advisors. Investors can check the websites of these regulators to see if they have any information on the conflict of interest of the financial advisor they are considering. One of the most effective ways to avoid conflicts of interest with financial advisors is to look at their fee structure. Some advisors may be compensated by commissions or other incentives that motivate them to make specific recommendations. These recommendations are often given even if they are not in the client’s best interest. Before deciding, it is essential to review all agreements and understand how the advisor will be compensated for their services. Work with advisors who adhere to the fiduciary standard. Fiduciaries have a duty of loyalty and trustworthiness toward their clients and must always act in their best interests. Clients can be assured that they receive unbiased advice and services. It is also essential for investors to research an advisor’s background before making any decisions. Make sure to know what type of advice they offer and whether it suits the situation. Reading reviews from former clients can also provide valuable insights. A conflict of interest arises when an advisor's objectives can cloud their judgment and cause them to make decisions that are not beneficial for their clients. Such interests may include business or financial interests. Conflicts of interest can be a significant concern for investors when choosing financial advisors. These conflicts can arise in several ways, including portfolio management, brokerage and trading, valuation and fee billing, solicitation arrangements, and employee activities. Investors can find information on the conflict of interest of financial advisors through various resources. They can review the firm's disclosure policy on their website, the SEC's IAPD website, FINRA's BrokerCheck website, and the websites of state securities regulators. Selecting the right financial advisor is crucial to minimize the risk of conflict of interest. Investors should evaluate their fee structure, fiduciary duty, background, experience, and track record and seek opinions from former clients before choosing an advisor. Ultimately, it is up to the investor to research and find an advisor that best fits their needs and objectives. The right decision will go a long way in ensuring a successful investment experience. What Is Conflict of Interest With Financial Advisors?

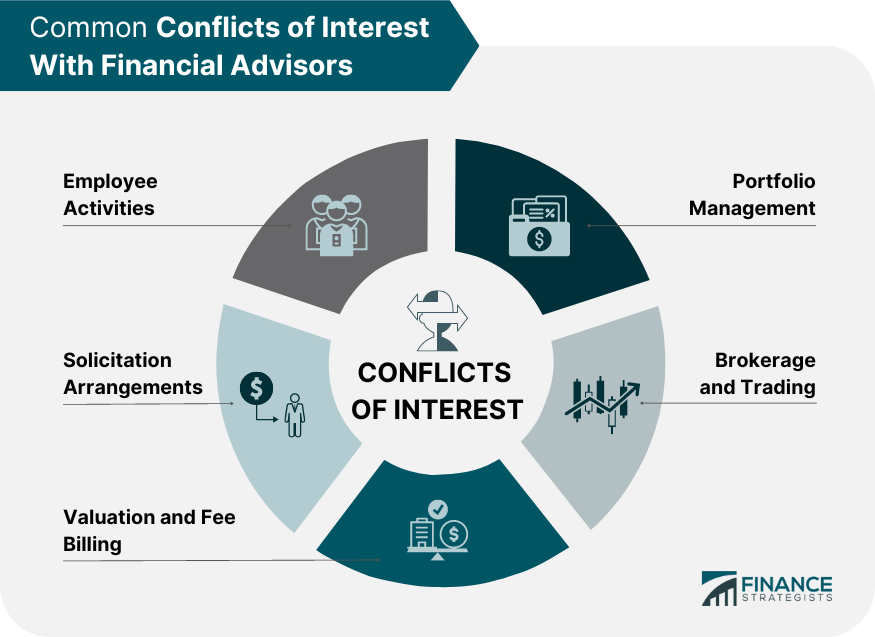

Common Conflicts of Interest With Financial Advisors

Portfolio Management

Brokerage and Trading

Valuation and Fee Billing

Solicitation Arrangements

Employee Activities

Examples of Conflicts of Interest With Financial Advisors

Financial Regulations and Conflict of Interest

Regulatory Bodies

Financial Industry Regulatory Authority (FINRA)

Key Regulations and Acts

Case Studies and Examples

Enron Scandal

Goldman Sachs and the Abacus 2007-AC1 Case

Bernie Madoff Ponzi Scheme

Where to Check the Conflict of Interest of Financial Advisors

How to Avoid Conflicts of Interest With Financial Advisors

Final Thoughts

Conflict of Interest With Financial Advisors FAQs

A conflict of interest among financial advisors can occur when their interests are no longer aligned with their clients. The advisor may be paid a commission and other incentives to recommend specific products or due to a lack of transparency about fees or services being provided.

Common conflicts of interest can include scenarios related to portfolio management, brokerage and trading, valuation and fee billing, solicitation arrangements, and employee activities, which can lead to questionable practices.

Some common signs of potential conflicts of interest include advisors recommending specific products or investments without explaining why they are beneficial. Ask your advisor about their policies and procedures for identifying, avoiding, and managing potential conflicts of interest.

Start by gathering information and talking to other advisors or industry professionals to understand whether the conflict is valid. If necessary, discuss the issue with your advisor directly and ask them to explain their actions. Also, it is essential to reach out to the appropriate securities commission in your state or province.

Use available resources like the SEC's IAPD website, FINRA's BrokerCheck website, and the websites of state securities regulators to check for any financial sanctions against them. Make sure that you understand their fee structure. Take some time to ask them questions about their investment strategies and inquire about any potential conflicts they might have. Additionally, make sure the financial advisor follows a fiduciary rule.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.