The Old Age, Survivors, and Disability Insurance (OASDI) program, often called Social Security, is the most extensive income maintenance program in the United States. It provides monthly compensation to partially substitute income lost due to retirement, disability, or death. The program is administered by the Social Security Administration (SSA). It is funded through taxes collected from workers, employers, and self-employed individuals, known as the OASDI tax. The money is put into the Federal Old Age and Survivors Insurance Trust Fund and Federal Disability Insurance Trust Fund. These funds pay both the benefits and the cost of the whole program. Have a financial question? Click here. The program was set up when Franklin D. Roosevelt signed the Social Security Act on August 14, 1935. During this time, the economy was afflicted by the Great Depression. In 1937, taxes started to be collected to fund the program. The program initially benefited the elderly because it intended to replace retirement income. Then, the 1939 amendment included the dependents or the surviving family members of a deceased wage earner. In 1956, another amendment added disability insurance. Since its inception, the program has also been amended several times to increase benefits and coverage. Today, the program is a cornerstone of income security for the elderly, disabled, and survivors, and millions of Americans are its beneficiaries. The OASDI tax is collected from employers and employees to fund the program. As of 2025, employees are responsible for 6.2%, or half of the total tax, while employers are responsible for another 6.2%. Combined, this is 12.4% OASDI tax for each person’s payroll. Self-employed individuals and independent contractors are responsible for the 12.4% OASDI tax. However, when figuring out their adjusted gross income (AGI), they can deduct 50% of the self-employment tax. The Social Security Administration regulates the annual OASDI rates. The amount of OASDI tax may mostly stay the same, but the maximum wages that are taxed may change depending on inflation and the cost of living index. In 2024, the OASDI maximum taxable wage was $168,600, while in 2025, it is $176,100. People can determine how much tax they owe using tools like the Internal Revenue Service’s (IRS) tax withholding calculator. Meanwhile, self-employed individuals can use Schedule SE to estimate their OASDI contributions. To qualify for the OASDI program, individuals must meet specific criteria. Generally, applicants must have earned a minimum amount of credits based on the years they have worked and paid OASDI taxes. The maximum credit allowed annually is four. Each year, the total earnings required to get one credit can vary. In 2024, one credit was awarded for every $1,730 each individual earned annually, while in 2025, a worker gains one credit for every $1,810 earned. The number of credits needed to apply for retirement benefits, disability benefits, or survivor benefits varies. There are also other requirements, such as age and the number of working years. Retirement benefits require at least 40 credits. Individuals typically need around ten years of employment and the proper payment of OASDI taxes to qualify for retirement benefits. They must also be 62 years old to start collecting retirement benefits. The monthly compensation issued is based on how much each individual earned before retirement. People are eligible for disability payments if they cannot work owing to a serious, long-term physical or mental ailment that negatively impacts their capacity to work and live independently. Recent and duration work tests are typically used to determine the individual's eligibility for disability benefits. The number of credits they need to fulfill these tests are contingent on their age and period of employment. Individuals below 24 years old may qualify for disability benefits if they have earned at least six credits in the three years immediately preceding the onset of their disability. Meanwhile, people aged 24 to 31 can qualify if they earned credits equal to half the period they worked between turning 21 and the beginning of their disability. Thus, the number of credits they need can range from 6 to 20. Individuals older than 31 years old need to have earned 20 or more credits in the ten years before the onset of their disability. The length of employment does not need to fall within a specific time frame for individuals to pass the duration work test. Instead, the table below only estimates the number of work credits required to pass this test. Survivor benefits are available to the spouses or children of a deceased individual. The number of credits required for these benefits will depend on the age of the demise. Fewer credits are needed for younger persons, and 40 credits are the maximum necessary for any individual. Even if an individual lacks the required credits, the SSA may be able to pay benefits to their beneficiaries. The family members of deceased individuals who have earned at least six credits for one-and-a-half years of work in the three years before their death can be entitled to benefits. The OASDI program was designed to provide support and security to those who have worked hard, paid their taxes, and made necessary contributions to society. However, some specific individuals are not eligible for these benefits. Civilian federal employees hired before January 1, 1984, are not covered under the OASDI program. Instead, they contribute to the Civil Service Retirement System (CSRS). Railroad workers are not eligible for OASDI benefits because the Railroad Retirement program covers them. This program works in coordination with Social Security and is funded from payroll taxes paid by railroad employers and employees. These employees might not be covered under the OASDI program if they were hired before 1986. Instead, they may be entitled to pensions from their employers or contribute to other retirement systems, such as the Civil Service Retirement System. Farm and domestic workers who are earning wages below certain levels are also excluded from OASDI benefits. This is because an anticipated administrative problem is associated with pay reporting and tax collection. Individuals with minimal net earnings from self-employment, often less than $400 per year, may also not be eligible for OASDI benefits. The OASDI program, more commonly known as Social Security, is the most comprehensive income maintenance program in the United States. It provides benefits to retired and disabled workers, as well as their dependents and survivors. The program was set up when Franklin D. Roosevelt signed the Social Security Act on August 14, 1935. It initially benefited the elderly by replacing retirement income and was amended several times since then to increase benefits and coverage. The Social Security Administration collects OASDI taxes from employees, employers, and self-employed individuals. As of 2025, the tax rates for both employee and employer are at 6.2% each, for a total of 12.4%. Self-employed individuals must pay the full 12.4% themselves. Retirement benefits require individuals to meet several credit requirements. Meanwhile, disability benefits have recent work tests, duration work tests, and age requirements. Lastly, survivor benefits are based on age and the number of work credits acquired. Some individuals are not eligible to receive OASDI benefits, such as civilian federal employees, railroad workers, some state or local government employees, domestic or farm workers, and self-employed people whose earnings are below $400. Understanding the OASDI program is one of the first steps in preparing for retirement. For more in-depth support on retirement planning, you can consult a financial professional.What Is the Old Age, Survivors, and Disability Insurance (OASDI) Program?

History of the OASDI Program

OASDI Tax

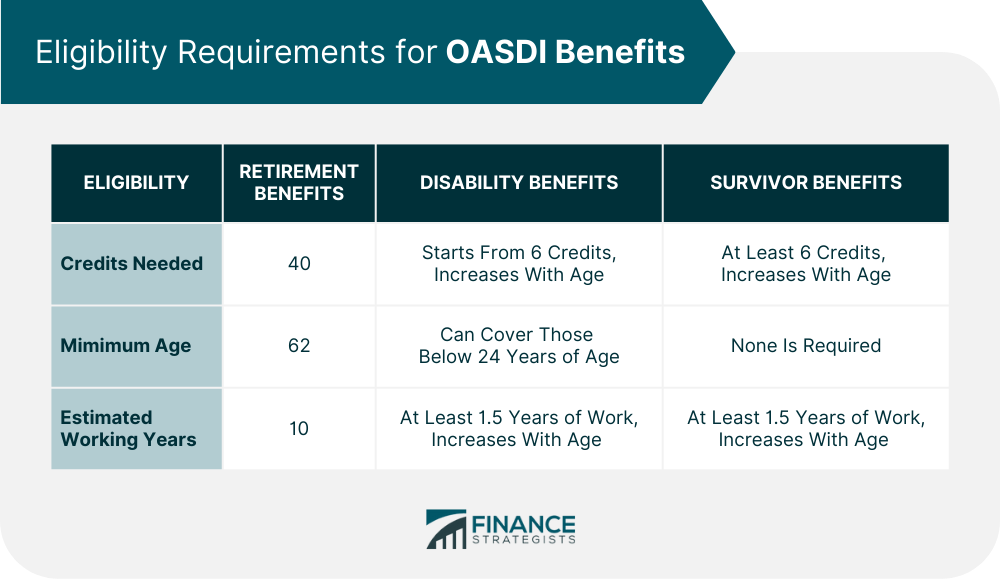

Eligibility for OASDI Program

For Retirement Benefits

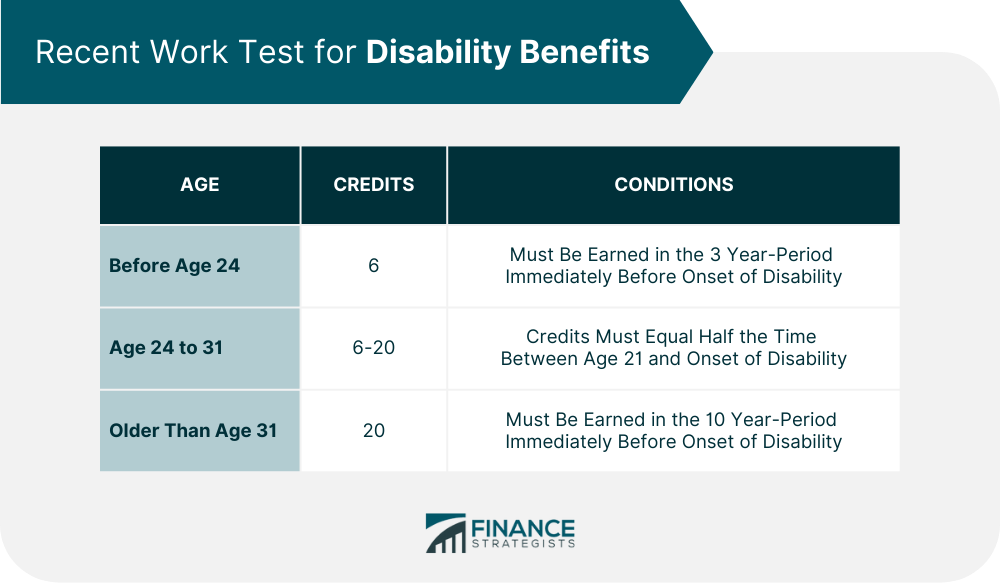

For Disability Benefits

Recent Work Test

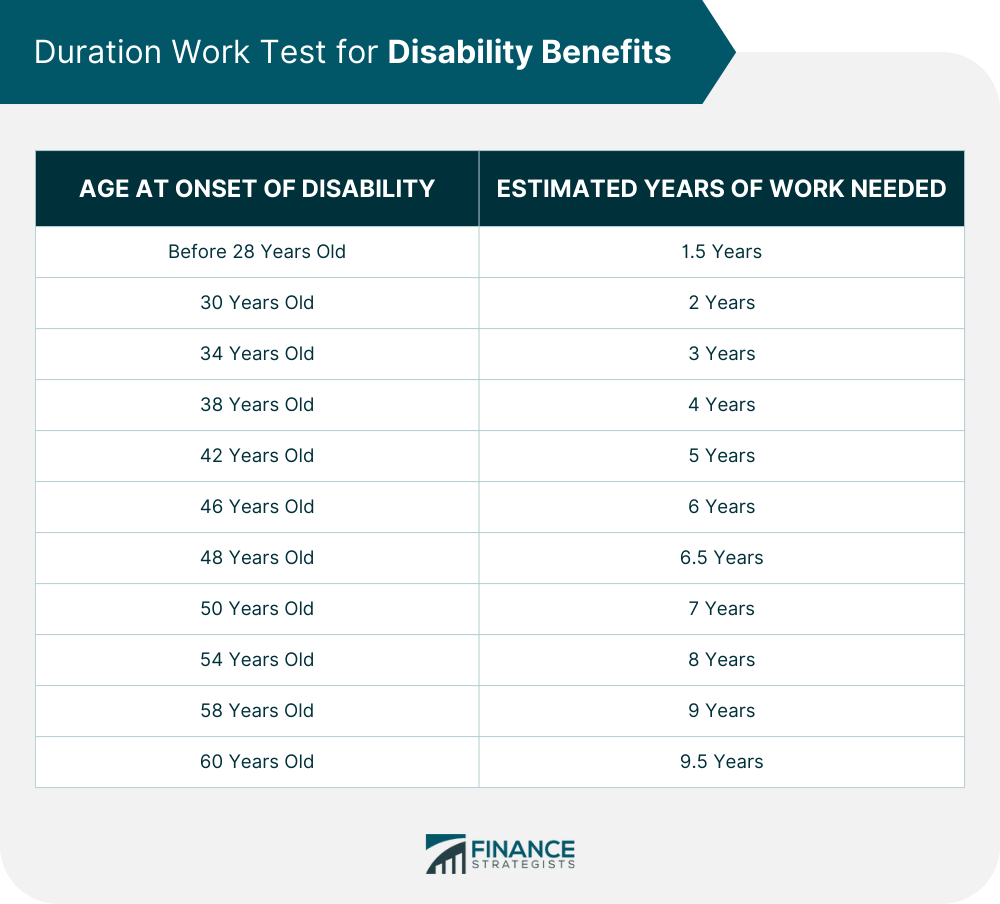

Duration Work Test

For Survivor Benefits

Who Is Excluded From OASDI Program?

Civilian Federal Employees

Railroad Workers

Employees of State and Local Governments

Domestic Workers and Farm Workers

Persons With Very Low Net Earnings

The Bottom Line

Old Age, Survivors, and Disability Insurance (OASDI) Program FAQs

Almost everyone must pay OASDI tax, but once their income reaches a certain limit, a portion can be exempted from taxation. In 2023, income beyond $160,200 will not be subject to OASDI tax. In 2024, earnings beyond $168,600 are exempted from taxation.

OASDI stands for Old Age, Survivors, and Disability Insurance and is the official name for the Social Security program in the United States. Most Americans know this program as Social Security, so both terms are used interchangeably.

Almost everyone who works in the United States needs to pay OASDI tax. The rate for employees and employers is set at 6.2% each for a total of 12.4%. Self-employed individuals must pay the full 12.4% themselves.

The OASDI tax funds the Social Security program, which offers retirement, disability, and survivor benefits. It also helps pay for the administrative costs associated with the program.

OASDI retirement benefits require individuals to earn 40 credits, work at least ten years and reach age 62. Meanwhile, disability benefits have recent work tests, duration work tests, and age requirements that applicants need to pass. Lastly, survivor benefits are based on age and the number of work credits acquired by the deceased individuals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.