Own-occupation disability insurance pays benefits to policyholders who are unable to work in their own occupation due to a disability. This type of coverage is particularly beneficial for individuals in specialized professions. Disability insurance is a critical component of financial planning as it offers income protection in the event of an illness or injury. It ensures financial stability and helps maintain quality of life during recovery. Own-occupation disability insurance focuses on the policyholder's specific job, whereas any-occupation coverage pays benefits only if the insured cannot work in any occupation. Own-occupation policies tend to be more expensive but provide broader protection. Eligibility for own-occupation disability insurance depends on factors such as occupational requirements, income, health status, and age. Understanding these criteria is crucial when applying for coverage. Certain professions are more likely to qualify for own-occupation disability insurance. These include specialized fields like medicine, law, and engineering, where the policyholder's skills are specific to their occupation. Insurers typically require proof of income to determine eligibility and benefit amounts. Stable and consistent income from the applicant's occupation is a key factor in obtaining coverage. Health status and pre-existing conditions can impact eligibility and premium rates. Insurers may exclude certain conditions or charge higher premiums for applicants with significant health risks. Age is another factor that affects eligibility, with younger applicants being more likely to qualify for coverage. Older applicants may face restrictions or higher premiums due to increased risk of disability. Own-occupation disability insurance policies include various features and options. Understanding these elements can help policyholders tailor coverage to meet their unique needs. The benefit period is the length of time for which the policy pays benefits. Shorter benefit periods result in lower premiums, but longer benefit periods provide greater financial security. The elimination period is the waiting period before benefits are paid. Choosing a longer elimination period can lower premium costs, but policyholders must be prepared to cover expenses during the waiting period. The benefit amount is the monthly payment received during disability. It is typically a percentage of the policyholder's income, and it is crucial to choose an adequate amount to maintain financial stability. Partial and residual disability benefits provide coverage for individuals who can still work but experience a reduction in income due to disability. This feature offers additional income protection for those with partial disabilities. COLA riders adjust benefit payments for inflation, ensuring that policyholders maintain their purchasing power over time. This option is particularly valuable for long-term disability claims. Riders and optional enhancements allow policyholders to customize their coverage. These additions may include guaranteed insurability, waiver of premium, and future increase options. Premium costs for own-occupation disability insurance depend on factors such as age, gender, occupation, health, and policy features. Understanding these factors can help policyholders make informed decisions about coverage. Age and gender play significant roles in determining premium costs. Younger individuals typically pay lower premiums, while women generally pay higher premiums due to their longer life expectancy and increased likelihood of disability. The risk associated with a policyholder's occupation impacts premium rates. High-risk professions, such as construction or manual labor, typically result in higher premiums due to the increased likelihood of disability. A policyholder's health and lifestyle affect premium costs. Insurers consider factors such as smoking, obesity, and pre-existing conditions when calculating premiums, with healthier individuals paying lower rates. The chosen policy features and coverage options directly influence premium costs. Higher benefit amounts, longer benefit periods, and additional riders increase the cost of coverage. Selecting the right own-occupation disability insurance policy involves assessing personal needs, comparing options, reviewing exclusions, and seeking professional advice. This process ensures that policyholders obtain the best coverage for their unique situations. Evaluating personal needs and financial goals is crucial when selecting a disability insurance policy. Consider factors such as income replacement, monthly expenses, and future financial obligations when determining the appropriate coverage level. Comparing different policy options and insurance providers is essential to finding the best coverage. Research various companies, policy features, and premium costs to make an informed decision. Understanding policy exclusions and limitations is vital when selecting coverage. Be aware of any restrictions or conditions that may impact the ability to receive benefits, such as pre-existing condition exclusions or specific disability definitions. Consulting with a financial advisor or insurance agent can help navigate the complexities of disability insurance. These professionals can provide guidance and recommendations based on an individual's unique circumstances and financial goals. Filing a claim for own-occupation disability insurance involves understanding the process, providing documentation, working with medical professionals, and appealing denied claims if necessary. Becoming familiar with the claim process is essential when filing for disability benefits. Ensure that all necessary forms and documentation are submitted promptly to avoid delays or denial of benefits. Providing documentation and proof of disability is a critical step in the claim process. This includes medical records, test results, and any other relevant information that demonstrates the policyholder's inability to perform their occupation. Medical professionals play a crucial role in the disability claim process. They provide expert opinions, verify the policyholder's condition, and may be consulted by the insurance company during the claim evaluation. If a claim is denied, policyholders have the option to appeal the decision. Understanding the appeal process and working with legal or professional representation can increase the likelihood of a successful outcome. In today's world, the risk of disability due to illness or injury is ever-present. Without the proper insurance coverage, a disability can lead to a significant loss of income and financial hardship. Own-occupation disability insurance offers policyholders the peace of mind of knowing that their income is protected, even if they can no longer work in their chosen profession. It allows policyholders to maintain their lifestyle and support their families during a challenging time. By carefully considering the eligibility criteria, policy features, and coverage options available, individuals can ensure that they are adequately covered in the event of a disability. Choosing the right policy can make all the difference in securing the financial stability needed to move forward with confidence.What Is Own-Occupation Disability Insurance?

Eligibility Criteria for Own-Occupation Disability Insurance

Occupational Requirements

Income Requirements

Health and Pre-Existing Conditions

Age Limitations

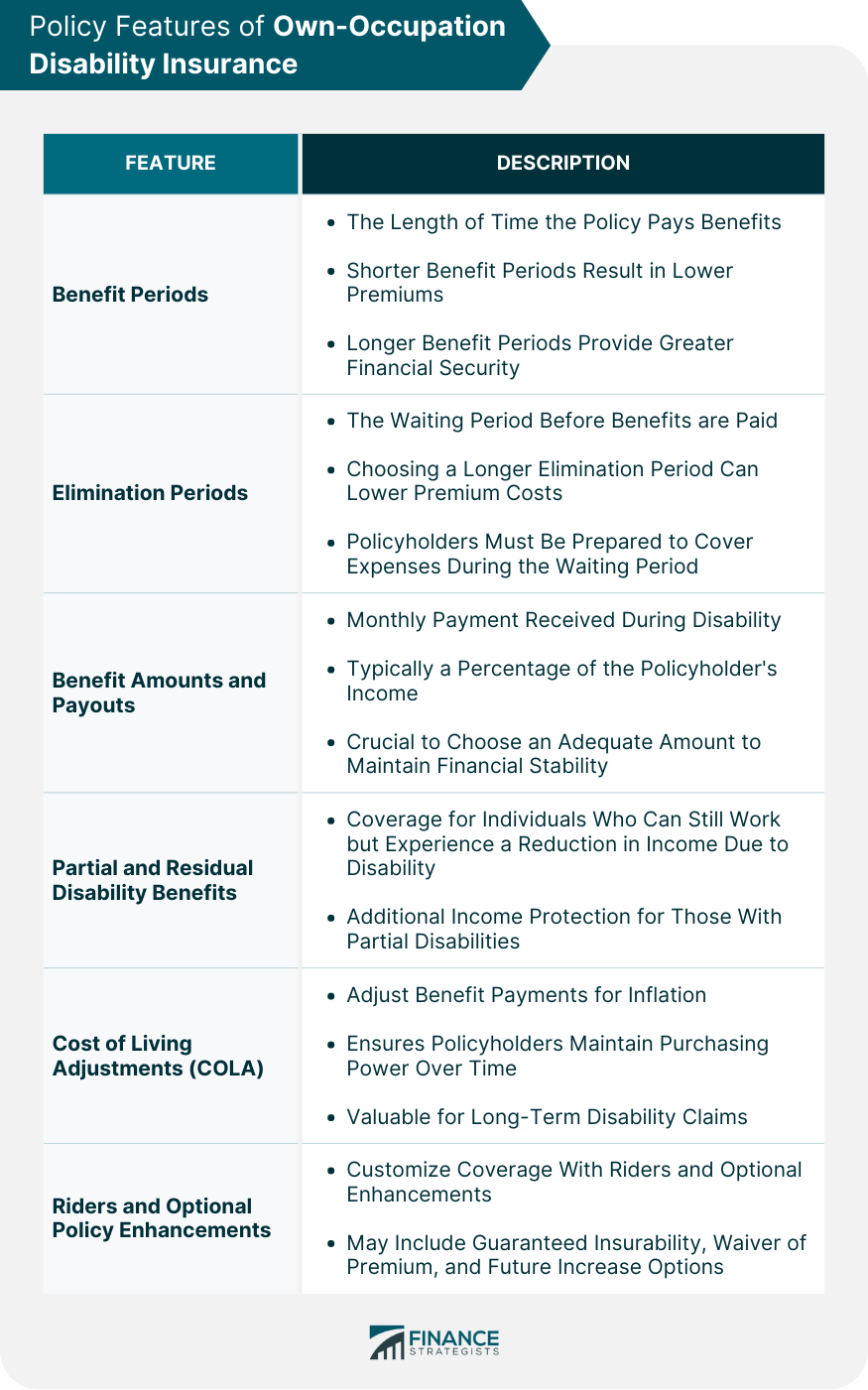

Policy Features of Own-Occupation Disability Insurance

Benefit Periods

Elimination Periods

Benefit Amounts and Payouts

Partial and Residual Disability Benefits

Cost of Living Adjustments (COLA)

Riders and Optional Policy Enhancements

Factors Affecting Own-Occupation Disability Insurance Premiums

Age and Gender

Occupational Risk

Health and Lifestyle Factors

Policy Features and Coverage Options

How to Choose the Right Own-Occupation Disability Insurance Policy

Assessing Personal Needs and Financial Goals

Comparing Policy Options and Providers

Reviewing Policy Exclusions and Limitations

Seeking Professional Advice

How to File a Claim for Own-Occupation Disability Insurance

Understanding the Claim Process

Documentation and Proof of Disability

The Role of Medical Professionals

Appealing Denied Claims

Conclusion

Own-Occupation Disability Insurance FAQs

Own-occupation disability insurance provides coverage if you can't work in your specific occupation due to a disability, even if you can work in another job.

Professionals with highly specialized skills, such as doctors, lawyers, and architects, who rely on their ability to work in their specific field, should consider this type of insurance.

Own-occupation disability insurance provides more comprehensive coverage than other types of disability insurance because it covers you if you can't work in your specific occupation due to a disability.

The cost of own-occupation disability insurance varies depending on several factors, including your occupation, age, health, and the amount of coverage you need.

It may be difficult to obtain own-occupation disability insurance if you have a pre-existing condition, but some insurance companies may still offer coverage with certain restrictions or higher premiums.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.