Disability income insurance is a type of insurance policy that provides financial support to individuals who become unable to work due to a disability. This coverage helps replace a portion of the policyholder's income, making it easier for them to maintain their financial stability and meet their expenses during their recovery period. Disability income insurance is an essential component of financial planning because it helps protect individuals and their families from the potential financial hardships that may result from an unexpected illness or injury. The loss of income during a disability can significantly impact a person's financial situation, making it difficult to cover essential expenses such as housing, medical care, and daily living costs. Disability income insurance policies typically cover a wide range of disabilities, including both physical and mental health conditions that may prevent an individual from working. Some examples include musculoskeletal disorders, cardiovascular diseases, mental health disorders, and neurological conditions. Short-term disability insurance provides coverage for a limited time, usually ranging from three to six months. This type of policy is designed to provide temporary financial support to individuals recovering from a brief illness or injury. Short-term disability insurance policies typically offer a benefit amount that replaces a percentage of the policyholder's pre-disability income, often around 60-80%. This amount is usually paid out on a weekly or monthly basis, depending on the policy terms. Short-term disability insurance policies typically have a waiting period, also known as an elimination period, which is the time between the onset of the disability and when the policyholder starts receiving benefits. Waiting periods can range from a few days to a few weeks, depending on the policy. Long-term disability insurance provides coverage for an extended period, which can last several years or until the policyholder reaches a specified age, such as 65. This type of policy is designed to provide financial support to individuals who are unable to work due to a long-lasting or permanent disability. Long-term disability insurance policies generally offer a benefit amount that replaces a percentage of the policyholder's pre-disability income, similar to short-term disability insurance. However, long-term policies typically have a lower percentage, ranging from 50-70%. The benefit amount is usually paid out on a monthly basis. Long-term disability insurance policies often have a longer waiting period compared to short-term policies. Waiting periods can range from 30 days to several months, depending on the policy. Short-term and long-term disability insurance policies differ in terms of their coverage periods, benefit amounts, and waiting periods. Short-term policies provide temporary financial support for brief periods of disability, while long-term policies offer extended coverage for longer-lasting or permanent disabilities. Additionally, short-term policies typically have shorter waiting periods and higher benefit amounts compared to long-term policies. The benefit period refers to the length of time during which the policyholder receives disability income benefits. Depending on the policy, the benefit period can last from a few months to several years or until the policyholder reaches a specified age. The elimination period, also known as the waiting period, is the time between the onset of the disability and when the policyholder starts receiving benefits. Elimination periods can vary depending on the type of policy and the policyholder's preferences. Disability income insurance policies use different definitions of disability to determine eligibility for benefits, which can significantly impact the scope of coverage. The two most common definitions of disability are: Under the own-occupation definition, a policyholder is considered disabled if they are unable to perform the duties of their specific occupation due to an illness or injury. This definition offers broader coverage, as it considers the policyholder disabled even if they can still work in a different job. The any-occupation definition considers a policyholder disabled only if they are unable to work in any occupation for which they are reasonably suited based on their education, training, and experience. This definition offers narrower coverage and may result in fewer claims being approved. Residual benefits are a feature of some disability income insurance policies that provide partial benefits to policyholders who experience a partial loss of income due to a disability. This feature helps support individuals as they transition back to work or adjust to a reduced work capacity. Cost of Living Adjustments (COLA) is an optional feature in some disability income insurance policies that increases the benefit amount to account for inflation over time. This ensures that the policyholder's benefits maintain their purchasing power throughout the benefit period. Non-cancelable and guaranteed renewable provisions ensure that the insurance company cannot cancel the policy or increase the premiums as long as the policyholder continues to pay their premiums on time. These features provide long-term stability and peace of mind for the policyholder. Several factors can influence the cost of disability income insurance premiums, including: Premiums typically increase with age, as older individuals have a higher likelihood of experiencing a disability. Women often pay higher premiums than men, as they generally have a higher risk of experiencing a disability during their working years. High-risk occupations, such as construction or manual labor, can result in higher premiums due to the increased likelihood of work-related injuries and disabilities. Individuals with pre-existing health conditions or risky lifestyle habits, such as smoking, may face higher premiums due to the increased likelihood of experiencing a disability. The coverage and benefit options chosen by the policyholder, such as the elimination period, benefit period, and optional riders, can significantly impact the cost of premiums. Group disability income insurance is a type of coverage that is commonly offered by employers as part of their employee benefits package. Some advantages of group coverage include lower premiums, simplified underwriting, and easy enrollment. However, group coverage may offer limited customization options, and benefits may be taxable if the employer pays the premiums. Many employers offer group disability income insurance to their employees as a way to attract and retain talent. Employees can often choose to enroll in the coverage during their annual benefits enrollment period. Individual disability income insurance policies are tailored to the specific needs and preferences of the policyholder. Advantages of individual coverage include customizable benefit options, portability, and non-taxable benefits (when premiums are paid with after-tax dollars). However, individual policies may have higher premiums and require a more thorough underwriting process compared to group coverage. Individual disability income insurance policies can be customized to suit the unique needs and preferences of the policyholder, including their preferred elimination period, benefit period, and optional riders. Before choosing a disability income insurance policy, it's important to assess your financial situation and determine how much coverage you need. Consider factors such as your current income, expenses, existing savings, and any other financial resources you have access to in case of a disability. Once you have a clear understanding of your needs, compare different policies and insurance providers. Look for features that are important to you, such as the definition of disability, elimination period, benefit period, and optional riders. Additionally, compare premium costs and the financial strength of the insurance companies. A financial advisor or insurance agent can provide expert guidance and help you navigate the process of choosing the right disability income insurance policy. They can help you assess your needs, compare policies, and ensure you make an informed decision. As your financial situation and needs change over time, it's important to periodically review your disability income insurance coverage to ensure it remains adequate. Consider updating your coverage if you experience significant life changes, such as a change in income, family status, or job. If you become disabled and need to file a claim for disability income insurance benefits, you will need to follow your insurance provider's specific claims process. This typically involves submitting a claim form, along with any required documentation and medical records. When filing a claim, you may need to provide documentation, such as proof of your income and employment status, as well as medical records and reports from your healthcare providers. This information will be used by the insurance company to assess your claim and determine your eligibility for benefits. If your claim is denied, you have the right to appeal the decision. The appeals process may involve submitting additional documentation or evidence to support your claim. It's essential to follow your insurance provider's specific appeals process and timelines to ensure your appeal is properly considered. In conclusion, disability income insurance is a critical component of a comprehensive financial plan, offering vital protection against the financial challenges that may arise due to an unexpected disability. This type of insurance can help replace a portion of a person's income, enabling them and their families to maintain financial stability and cover essential expenses, such as housing, medical care, and daily living costs. As the impact of a disability can be significant, it is crucial for individuals to carefully consider their insurance needs and options to ensure they have adequate coverage in place. To find the most suitable disability income insurance policy, individuals should thoroughly research different policies and providers, comparing key features such as the definition of disability, elimination period, benefit period, and optional riders. Additionally, working with a financial advisor or insurance agent can provide valuable guidance and expertise to help navigate the selection process. Periodic reviews of coverage are also essential, as financial situations and needs change over time, necessitating adjustments to insurance policies. By taking these steps, individuals can better safeguard their financial well-being and have greater peace of mind in the face of potential disabilities.What Is Disability Income Insurance?

Types of Disability Income Insurance

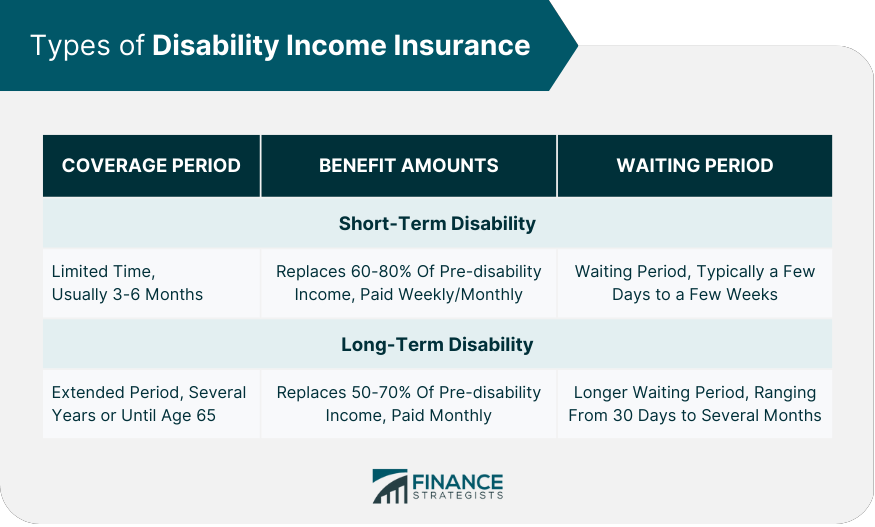

Short-Term Disability Insurance

Coverage Period

Benefit Amounts

Waiting Period

Long-Term Disability Insurance

Coverage Period

Benefit Amounts

Waiting Period

Comparison of Short-Term and Long-Term Disability Insurance

Key Features of Disability Income Insurance

Benefit Period

Elimination Period

Definition of Disability

Own-Occupation

Any-Occupation

Residual Benefits

Cost of Living Adjustments (COLA)

Non-cancelable and Guaranteed Renewable

Factors Affecting Disability Income Insurance Premiums

Age

Gender

Occupation

Health and Lifestyle

Coverage and Benefit Options

Understanding Group and Individual Disability Income Insurance

Group Disability Income Insurance

Pros and Cons

Commonly Offered by Employers

Individual Disability Income Insurance

Pros and Cons

Tailored to Individual Needs

How to Choose the Right Disability Income Insurance Policy

Assessing Your Needs and Financial Situation

Comparing Policies and Providers

Working With a Financial Advisor or Insurance Agent

Periodically Reviewing Your Coverage

Claims Process for Disability Income Insurance

Filing a Claim

Providing Documentation and Medical Records

Appeals Process for Denied Claims

Conclusion

Disability Income Insurance FAQs

Disability income insurance is a type of insurance policy that provides financial protection for individuals who are unable to work due to a disability or injury. It pays out a portion of your income to help you cover your living expenses while you are unable to work.

Anyone who relies on their income to cover their living expenses should consider disability income insurance. This includes people who are self-employed, freelance workers, and those who do not have access to disability benefits through their employer.

The cost of disability income insurance varies depending on several factors, including your age, occupation, and health status. Generally, the younger and healthier you are, the lower your premiums will be. Premiums can range from a few hundred dollars to several thousand dollars per year.

Disability income insurance covers a portion of your income if you are unable to work due to a disability or injury. The amount of coverage you receive depends on the terms of your policy. Some policies may also provide additional benefits, such as coverage for medical expenses or rehabilitation.

When choosing a disability income insurance policy, it's important to consider factors such as the amount of coverage you need, the length of the benefit period, and the waiting period before benefits begin. It's also a good idea to compare policies from multiple insurers to find the best coverage at a price you can afford. Working with an experienced insurance agent can also help you navigate the process and find the right policy for your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.