Financial planning for non-profit employees refers to the process of developing and implementing a comprehensive financial strategy tailored to the unique circumstances, challenges, and opportunities associated with working in the non-profit sector. Non-profit employees often earn lower salaries compared to their counterparts in for-profit industries but may have access to different benefits and retirement plans. Financial planning for non-profit employees involves setting short-term and long-term financial goals, creating and managing a budget, building an emergency fund, saving for retirement, managing debt, obtaining appropriate insurance coverage, tax planning, and potentially working with a financial planner. The main objective is to help non-profit employees achieve financial stability and security while they continue pursuing their passion for positively impacting society. Non-profit organizations can include charities, educational institutions, religious groups, and community service organizations. These organizations primarily focus on promoting a social cause or providing public benefit, and their profits are reinvested into the organization's mission. Non-profit employees may receive lower salaries compared to their counterparts in the for-profit sector. However, many non-profit organizations offer generous benefits packages that can help offset the lower wages. These packages may include health insurance, retirement savings plans, and professional development opportunities. Working for a non-profit organization can be a rewarding experience, as employees can contribute to a cause they are passionate about. However, non-profit employees may need more money due to lower salaries and limited resources. These individuals need to take control of their finances and plan for their future. Short-term financial goals are objectives that can be achieved within one year. Examples include paying off a credit card, building an emergency fund, or saving for a vacation. Mid-term goals have a timeframe of one to five years and may include saving for a down payment on a home, purchasing a vehicle, or starting a small business. Long-term financial goals are those that take more than five years to achieve, such as saving for retirement, funding a child's college education, or paying off a mortgage. Non-profit employees should prioritize their financial goals based on their personal values and objectives. Aligning financial goals with personal values can help maintain motivation and focus during planning. A budget is a financial plan that outlines expected income and expenses over a specific period. Non-profit employees should create a detailed budget that includes all sources of income and expenses, such as housing, utilities, food, transportation, and entertainment. Tracking expenses is crucial for understanding spending habits and identifying areas for improvement. Non-profit employees can use budgeting apps, spreadsheets, or pen and paper to record their daily expenses. After tracking expenses, non-profit employees should review their spending patterns and identify areas where they can cut costs. Reducing expenses and increasing savings will help create a financial buffer and pave the way for achieving financial goals. Non-profit employees may experience income fluctuations due to funding changes, grant cycles, or seasonal employment. Adjusting budgets accordingly to maintain financial stability during these periods is essential. An emergency fund is a cash reserve set aside to cover unexpected expenses or income loss. Having an emergency fund is crucial for non-profit employees to maintain financial stability during challenging times. Financial experts recommend having three to six months' worth of living expenses in an emergency fund. Non-profit employees should consider their job stability, financial obligations, and personal circumstances when determining the appropriate size for their emergency fund. Non-profit employees can build and maintain an emergency fund by: Setting a monthly savings goal and automating transfers to a designated emergency fund account. Allocating a portion of windfalls, such as bonuses or tax refunds, to the emergency fund. Reducing discretionary expenses and redirecting the savings to the emergency fund. Periodically reviewing and adjusting the emergency fund size based on changing financial circumstances. Non-profit employees may have access to various retirement plans, including: These tax-deferred retirement plans are designed for employees of non-profit organizations, public schools, and certain religious institutions. Contributions to 403(b) plans are made pre-tax, reducing taxable income and allowing investments to grow tax-deferred until withdrawn during retirement. These deferred compensation plans are available for employees of state and local governments and some non-profit organizations. Similar to 403(b) plans, contributions to 457(b) plans are made pre-tax, and investments grow tax-deferred. The Savings Incentive Match Plan for Employees (SIMPLE) IRA is a retirement plan designed for small businesses and non-profit organizations with 100 or fewer employees. The Simplified Employee Pension (SEP) IRA is another retirement plan option for small organizations, including non-profits. Employers make tax-deductible contributions to the SEP-IRA on behalf of their employees, and investments grow tax-deferred. Non-profit employees should familiarize themselves with their employer's retirement plan offerings and take advantage of any matching or non-elective contributions provided. These contributions can significantly boost retirement savings and help achieve long-term financial goals. Non-profit employees can also consider other retirement savings options, such as: Traditional IRA: An individual retirement account that allows pre-tax contributions and tax-deferred investment growth. Roth IRA: A retirement account that allows after-tax contributions, tax-free investment growth, and withdrawals during retirement. Investment Accounts: Non-retirement brokerage accounts that allow for investing in various assets, such as stocks, bonds, and mutual funds. Non-profit employees should estimate their retirement expenses and determine how much they need to save to maintain their desired lifestyle during retirement. Factors to consider include expected Social Security benefits, anticipated retirement age, and desired retirement income. Non-profit employees may have various types of debt, including: Student loans Credit card debt Personal loans Non-profit employees can use the following strategies to pay down debt: Debt Avalanche: Prioritize paying off debts with the highest interest rates first, while making minimum payments on other debts. Debt Snowball: Focus on paying off the smallest debts first, while making minimum payments on larger debts, to build momentum and motivation. Debt Consolidation: Combine multiple high-interest debts into a single lower-interest loan, simplifying repayment and potentially reducing interest costs. Non-profit employees may qualify for student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness. These programs can help reduce the burden of student loan debt for eligible borrowers working in qualifying non-profit organizations. Non-profit employees should consider obtaining the following types of insurance to protect their financial well-being: Health insurance Life insurance Disability insurance Renters/homeowners insurance Non-profit employees should assess their insurance needs based on their personal circumstances, financial obligations, and risk tolerance. They should carefully review and compare different coverage options to find the best balance between cost and protection. To reduce insurance costs, non-profit employees can: Shop around and compare quotes from multiple insurance providers. Bundle policies, such as home and auto insurance, with the same provider. Increase deductibles, which can lower premium costs but will require a larger out-of-pocket expense in the event of a claim. Maintain a good credit score, as it may influence insurance premium rates. Non-profit employees are subject to federal, state, and local income taxes and Social Security and Medicare taxes. It's essential to understand tax liabilities and make timely estimated tax payments to avoid penalties and interest. Non-profit employees may be eligible for various tax deductions and credits, such as: Student loan interest deduction Retirement savings contributions credit (Saver's Credit) Educator expenses deduction (for qualified teachers) Charitable contributions deduction To minimize taxes and maximize refunds, non-profit employees can: Contribute to pre-tax retirement accounts, such as a 403(b) or Traditional IRA. Itemize deductions if they exceed the standard deduction. Take advantage of available tax credits and deductions. Consult with a tax professional for personalized advice. Non-profit employees should consider the tax implications of their retirement savings strategies. Contributing to pre-tax retirement accounts, such as 403(b) or Traditional IRA, can lower taxable income, while Roth IRA contributions offer tax-free growth and withdrawals in retirement. A financial planner can help non-profit employees navigate complex financial situations, set realistic financial goals, and develop a comprehensive financial plan. To find and select a financial planner, non-profit employees should: Seek referrals from friends, family, or colleagues. Ensure the planner holds relevant certifications, such as Certified Financial Planner (CFP). Verify the planner's fee structure and ensure it aligns with their budget and preferences. Schedule a consultation to discuss financial goals and determine if the planner is a good fit. Working with a financial planner involves discussing financial goals, sharing personal financial information, and collaborating to develop a customized financial plan. The planner will provide guidance and recommendations to help non-profit employees make informed financial decisions and achieve their goals. In conclusion, financial planning is crucial for non-profit employees who may earn lower salaries compared to their for-profit counterparts but often have access to different benefits and retirement plans. Financial planning for non-profit employees involves setting short-term and long-term financial goals, creating and managing a budget, building an emergency fund, saving for retirement, managing debt, obtaining appropriate insurance coverage, tax planning, and potentially working with a financial planner. It is essential for non-profit employees to prioritize their financial goals based on their personal values and objectives and take control of their finances to plan for their future. By implementing these strategies, non-profit employees can achieve financial stability and security while they continue pursuing their passion for positively impacting society. Working with a financial planner can also help non-profit employees navigate complex financial situations, set realistic financial goals, and develop a comprehensive financial plan.Overview of Financial Planning for Non-Profit Employees

Understanding Non-Profit Employment

Types of Non-Profit Organizations

Typical Non-Profit Employee Compensation Structure

Benefits and Drawbacks of Non-Profit Employment

Setting Financial Goals for Non-Profit Employees

Short-Term Goals

Mid-Term Goals

Long-Term Goals

Prioritizing and Aligning Financial Goals With Personal Values

Budgeting and Expense Management for Non-Profit Employees

Creating a Budget

Tracking Expenses

Reducing Expenses and Increasing Savings

Adjusting Budgets Based on Income Fluctuations

Building an Emergency Fund for Non-Profit Employees

Importance of an Emergency Fund

Determining the Appropriate Emergency Fund Size

Strategies for Building and Maintaining an Emergency Fund

Saving for Non-Profit Employees’ Retirement

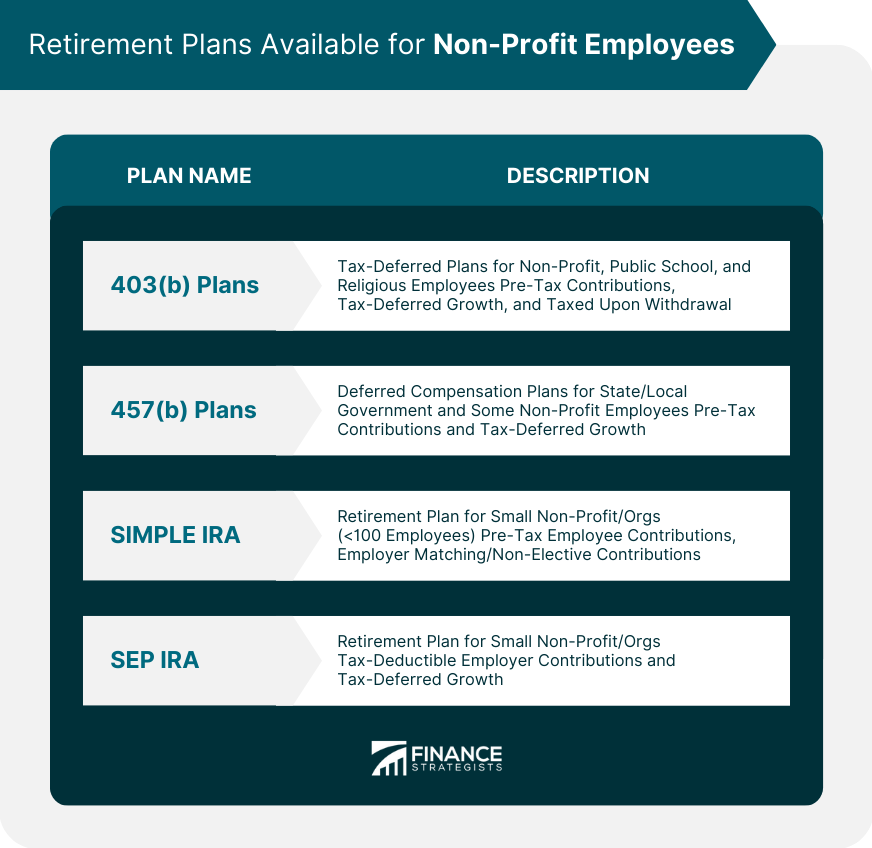

Retirement Plans Available for Non-Profit Employees

403(b) Plans

457(b) Plans

SIMPLE IRA

SIMPLE IRAs allow employees to contribute pre-tax dollars, and employers must make either matching or non-elective contributions.SEP IRA

Understanding Employer Retirement Plan Contributions

Additional Retirement Saving Options

Determining Retirement Savings Goals

Managing Debt for Non-Profit Employees

Types of Debt Common to Non-Profit Employees

Strategies for Paying Down Debt

Student Loan Forgiveness Programs for Non-Profit Employees

Insurance and Risk Management for Non-Profit Employees

Types of Insurance

Evaluating Insurance Needs and Coverage Options

Strategies for Reducing Insurance Costs

Tax Planning for Non-Profit Employees

Understanding Non-Profit Employee Tax Liabilities

Tax Deductions and Credits for Non-Profit Employees

Strategies for Minimizing Taxes and Maximizing Refunds

Tax Planning for Non-Profit Employee Retirement Plans

Working With a Financial Planner

Benefits of Working With a Financial Planner

Finding and Selecting a Financial Planner

Establishing a Financial Plan With a Professional

Conclusion

Financial Planning for Non-Profit Employees FAQs

Financial planning for non-profit employees often involves addressing lower salaries, fluctuating income due to funding changes or grant cycles, and navigating the specific retirement plans and benefits offered by non-profit organizations. Non-profit employees need to create a solid financial plan to achieve their goals while working towards their organization's mission.

Financial planning helps non-profit employees set realistic short-term and long-term financial goals, manage their budget, save for emergencies and retirement, reduce and manage debt, obtain appropriate insurance, and minimize tax liabilities. This comprehensive approach ensures financial stability and security, allowing them to focus on their passion for making a positive impact.

Non-profit employees may have access to specific retirement plans such as 403(b) plans, 457(b) plans, SIMPLE IRAs, and SEP IRAs. Additionally, they can consider other retirement savings options like Traditional IRAs, Roth IRAs, and investment accounts to supplement their retirement savings and achieve their long-term financial goals.

Financial planning for non-profit employees includes strategies for paying down various types of debt, such as student loans, credit card debt, and personal loans. It can also help them explore student loan forgiveness programs, like Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness, which can reduce the burden of student loan debt for eligible borrowers working in qualifying non-profit organizations.

An emergency fund is essential in financial planning for non-profit employees because it provides a financial safety net to cover unexpected expenses or income loss. Given the potential income fluctuations and funding uncertainties in the non-profit sector, having an emergency fund ensures financial stability and peace of mind during challenging times.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.