A Qualified Terminable Interest Property (QTIP) trust is an estate planning tool designed to provide financial support to a surviving spouse while ensuring that the remaining assets are passed on to the grantor's chosen beneficiaries after the spouse's death. These trusts offer tax advantages, flexibility, and control over the distribution of assets. QTIP trusts serve the purpose of balancing the interests of different beneficiaries in an estate plan, particularly in cases involving blended families, where the grantor wants to provide for their spouse as well as children from a previous relationship. The trust also offers protection from creditors and lawsuits, while allowing the grantor to maintain control over the assets during the spouse's lifetime. To set up a QTIP trust, the grantor must be a U.S. citizen, and the trust must be irrevocable. The surviving spouse must also be a U.S. citizen and the trust's only beneficiary during their lifetime. Additionally, the trust must meet specific requirements related to income distribution and the ability to change beneficiaries. Setting up a QTIP trust involves drafting a trust document, which outlines the terms and provisions of the trust, and appointing a trustee to manage the trust assets. It is advisable to consult with an estate planning attorney to ensure that the trust document complies with federal and state laws and regulations. The grantor must carefully select a trustee, who will be responsible for managing the trust assets and making distributions to the beneficiaries. The trustee can be an individual or a corporate entity, such as a bank or trust company. The beneficiaries of the trust include the surviving spouse and any other individuals or entities the grantor chooses to receive the remaining trust assets after the spouse's death. The QTIP trust must provide the surviving spouse with a lifetime income interest in the trust assets. This means that the spouse must receive all income generated by the trust, typically distributed at least annually. The trust document may restrict the distribution of the trust principal to the surviving spouse, ensuring that the remaining assets are preserved for the grantor's chosen beneficiaries. However, in certain circumstances, the trustee may have the discretion to distribute the principal to the spouse, depending on the trust's provisions. The marital deduction allows for the unlimited transfer of assets between spouses without incurring federal estate tax. QTIP trusts take advantage of this deduction by allowing the grantor to transfer assets to the trust, which then qualifies for the marital deduction, thereby reducing or eliminating the estate tax liability. Estate tax implications arise when the surviving spouse dies, and the remaining trust assets pass to the other beneficiaries. At this point, the assets are included in the spouse's estate for estate tax purposes. However, the overall tax burden may be reduced through proper estate planning and the use of other tax-saving strategies. A QTIP trust allows the grantor to retain control over the trust assets by providing the option to change the trust's beneficiaries during the spouse's lifetime. This flexibility ensures that the grantor can respond to changes in family dynamics or other circumstances that may warrant a change in the distribution of assets. QTIP trusts can include provisions that grant the trustee discretion to deal with unforeseen changes in circumstances, such as financial hardship, health issues, or changes in tax laws. These provisions help ensure that the trust can adapt to the evolving needs of the beneficiaries and the grantor's intentions. QTIP trusts offer the advantage of deferring estate taxes until the death of the surviving spouse, which can provide significant tax savings. This deferral allows for the efficient use of the marital deduction and minimizes the overall estate tax burden on the family's wealth. The marital deduction is a valuable estate planning tool, and QTIP trusts help maximize its benefits by allowing assets to be transferred to the trust without incurring estate taxes. This strategy helps preserve wealth for future generations while providing financial support to the surviving spouse. QTIP trusts help ensure that the grantor's assets remain within the family by specifying the beneficiaries who will receive the remaining trust assets after the surviving spouse's death. This strategy can be particularly beneficial in cases of blended families, where the grantor wants to provide for their spouse while also ensuring that their children from a previous relationship ultimately receive the assets. Assets held within a QTIP trust are generally protected from the claims of the surviving spouse's creditors and potential lawsuits, helping to safeguard the family's wealth for future generations. QTIP trusts enable the grantor to retain control over the trust assets during the surviving spouse's lifetime by allowing them to change beneficiaries and providing flexibility in dealing with changes in circumstances. This level of control ensures that the grantor's intentions for the distribution of assets are fulfilled. The flexibility offered by QTIP trusts allows the grantor to respond to changes in family dynamics, such as the addition of new family members or changes in the relationships between beneficiaries. This adaptability helps ensure that the estate plan remains aligned with the grantor's wishes over time. Setting up and maintaining a QTIP trust can be complex, involving legal formalities and ongoing administrative tasks. These complexities may require the assistance of professional advisors, such as estate planning attorneys and accountants, which can be costly. QTIP trusts can sometimes lead to conflicts between the surviving spouse and other beneficiaries, particularly if the trust restricts access to the principal. These conflicts may require the intervention of the trustee or legal proceedings to resolve. While restrictions on the distribution of trust principal can help protect assets for future generations, they may also limit the financial resources available to the surviving spouse, potentially leading to financial hardship in certain circumstances. Qualified Terminable Interest Property (QTIP) trusts are a valuable estate planning tool. They provide financial support to a surviving spouse while ensuring assets pass to chosen beneficiaries after their death. Setting up a QTIP trust involves eligibility criteria, required documentation, choosing a trustee, and identifying beneficiaries. QTIP trusts offer tax benefits, such as deferring estate taxes and maximizing the marital deduction. They protect assets, provide control and flexibility, and address changes in family dynamics. However, potential drawbacks include legal complexities, conflicts between beneficiaries, and limitations on access to trust principal. Overall, QTIP trusts offer significant advantages in balancing the interests of multiple beneficiaries and preserving wealth for future generations. Consulting with estate planning professionals is essential for properly establishing and managing a QTIP trust. Given the complexities and nuances of QTIP trusts, it is crucial to consult with professional advisors to ensure that your estate plan aligns with your goals and complies with applicable laws and regulations. Definition of Qualified Terminable Interest Property (QTIP) Trusts

Purpose of QTIP Trusts

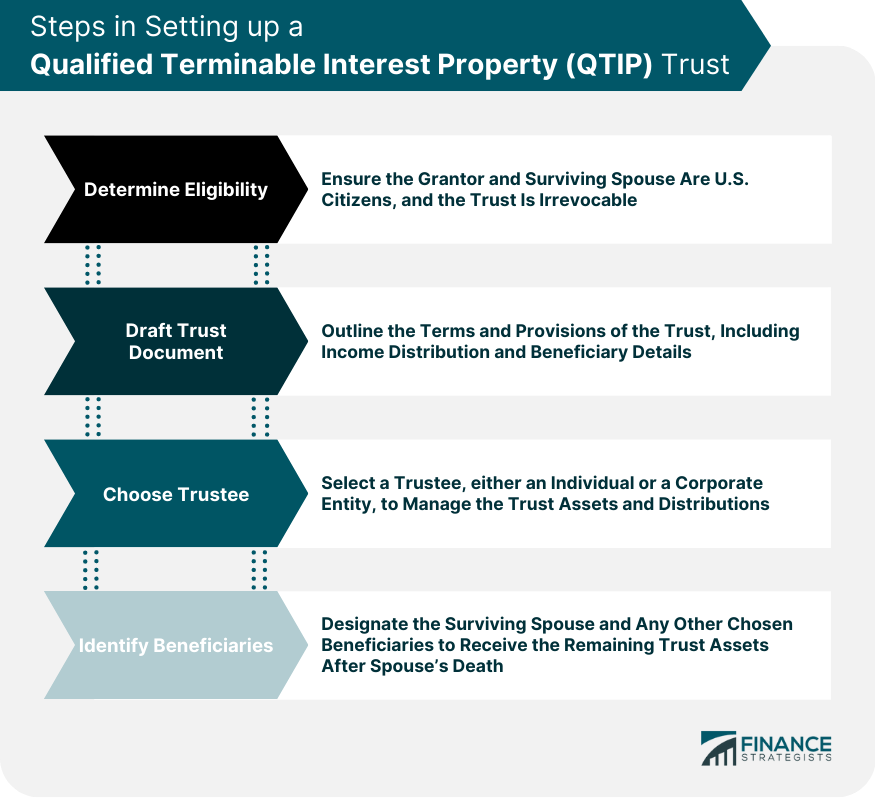

Setting up a QTIP Trust

Eligibility Criteria for QTIP Trusts

Required Documentation and Legal Formalities

Choosing a Trustee and Beneficiaries

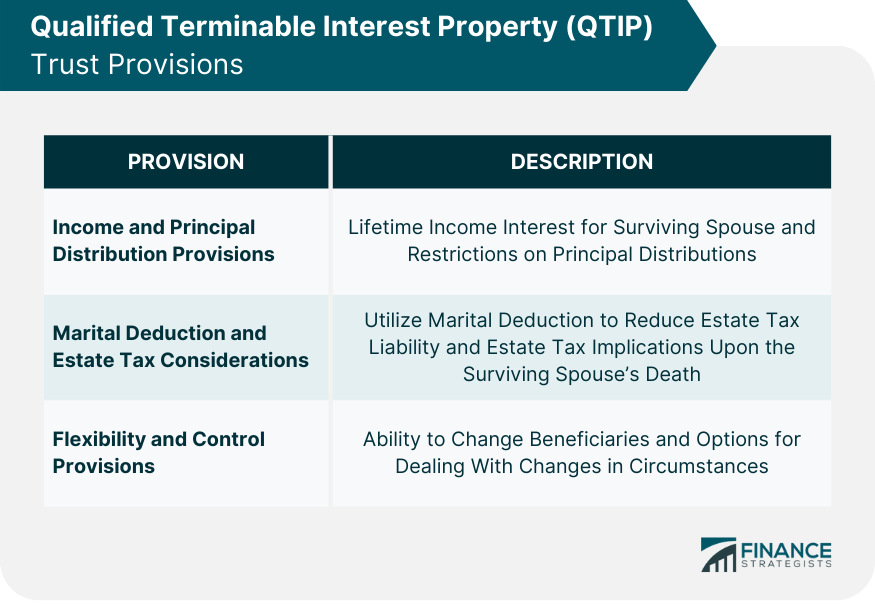

QTIP Trust Provisions

Income and Principal Distribution Provisions

Lifetime Income Interest for Surviving Spouse

Restrictions on Principal Distributions

Marital Deduction and Estate Tax Considerations

Role of Marital Deduction in QTIP Trusts

Estate Tax Implications

Flexibility and Control Provisions

Ability to Change Beneficiaries

Options for Dealing With Changes in Circumstances

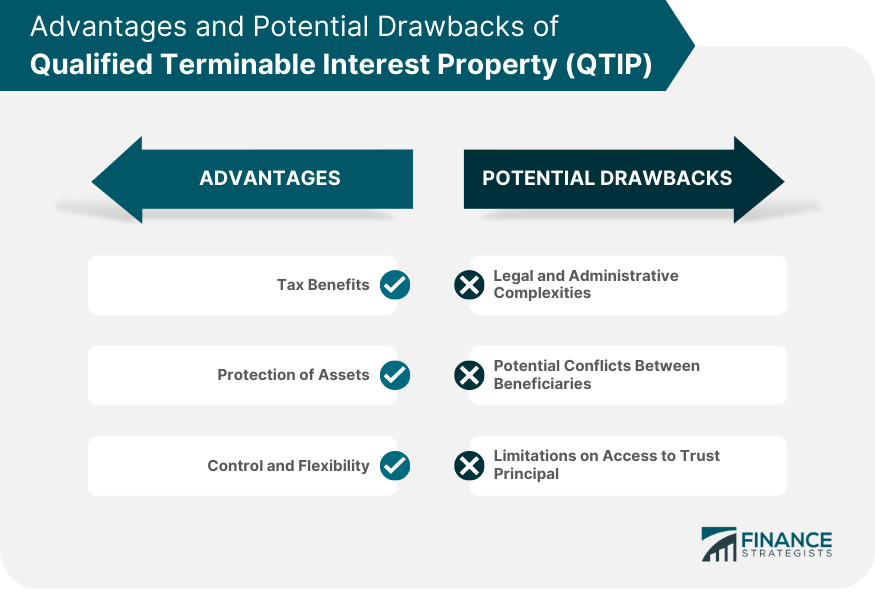

Advantages of QTIP Trusts

Tax Benefits

Deferral of Estate Taxes

Maximizing the Marital Deduction

Protection of Assets

Ensuring Assets Remain in the Family

Protection from Creditors and Lawsuits

Control and Flexibility

Retaining Control Over Assets During Spouse's Lifetime

Ability to Address Changes in Family Dynamics

Potential Drawbacks of QTIP Trusts

Legal and Administrative Complexities

Potential Conflicts Between Beneficiaries

Limitations on Access to Trust Principal

Conclusion

Qualified Terminable Interest Property (QTIP) FAQs

A QTIP trust is an estate planning tool designed to provide financial support to a surviving spouse while ensuring that the remaining assets are passed on to the grantor's chosen beneficiaries after the spouse's death. It offers tax advantages, flexibility, and control, making it an essential tool for preserving and transferring wealth.

A QTIP trust offers two primary tax benefits: deferral of estate taxes and maximization of the marital deduction. By qualifying for the marital deduction, the trust allows the grantor to transfer assets without incurring estate taxes, reducing the overall estate tax burden and preserving wealth for future generations.

A QTIP trust provides asset protection by ensuring that the grantor's assets remain within the family and are passed on to the chosen beneficiaries after the surviving spouse's death. Additionally, assets held within the trust are generally protected from the claims of the spouse's creditors and potential lawsuits.

The main drawbacks and limitations of a QTIP trust include legal and administrative complexities, potential conflicts between beneficiaries, and limitations on access to the trust principal. These factors may require the intervention of professional advisors or legal proceedings to address, which can be costly.

QTIP trusts offer tax benefits by deferring estate taxes until the death of the surviving spouse and maximizing the marital deduction, which allows for unlimited asset transfers between spouses without incurring federal estate tax. These tax advantages help minimize the overall estate tax burden and preserve wealth for future generations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.