A savings account is a deposit account that a customer can open at a financial institution, primarily banks or credit unions. Unlike checking accounts, which are primarily designed for frequent transactions, savings accounts are structured to hold deposits over a longer period. They are one of the most familiar types of accounts, often representing the first step individuals take in their banking journey. The fundamental purpose of a savings account is to provide a safe and secure place for individuals and businesses to deposit money that they do not need immediate access to. It's like having a personal vault, only more accessible and with the added benefit of earning interest over time. People use savings accounts to park their emergency funds, save for short-term goals, or simply as a place to accumulate wealth. Banks, available both in your local neighborhood and online, offer a multitude of services tailored to diverse needs. Choosing a local bank provides the convenience of in-person consultations and proximity for quick visits. On the other hand, credit unions, being non-profit organizations, often offer more attractive interest rates and lower fees, all while keeping the community's best interests at heart. It's important to reflect upon one's own priorities, be it global access, community-driven initiatives, or a mix of both, before settling on a decision. While many prefer the personal touch of traditional banks, the digital age has heralded the rise of online banking. Online banks often operate without physical branches, translating into lower overhead costs. A savings account isn't a one-size-fits-all solution. Standard savings accounts offer a simple, no-frills approach to saving, usually accompanied by minimal fees and standard interest rates. However, for those seeking more from their deposits, high-yield savings accounts promise better returns, albeit often paired with higher minimum balance requirements. Additionally, some banks and credit unions offer specialized savings accounts. These are tailor-made for specific goals or needs, such as saving for a vacation, a holiday fund, or even tax-saving purposes. When deciding on the type of account, it's crucial to evaluate not just immediate needs but also long-term financial goals. This usually includes a valid identification document, like a driver's license or passport. A proof of address is also typically required, which could be a recent utility bill, lease agreement, or any official document stating your residence. For those who aren't citizens, an Individual Taxpayer Identification Number might be required in place of a Social Security Number. This ensures that the bank can verify the identity of the individual, promoting secure and transparent financial transactions. With documents in hand, you're ready to initiate the account opening process. If you've opted for a traditional bank or credit union, a visit to the nearest branch is in order. Here, a financial representative will guide you through the application process. If you've leaned towards the digital side, most online banks offer a straightforward online application process. The form usually requires personal details such as name, address, contact information, and financial information. Employment details, income source, and other financial commitments might also be requested. While the process is intuitive, it's essential to be accurate and truthful when providing information. Any discrepancies can lead to delays or even rejection of the application. The data provided also helps banks offer personalized services and financial products in the future. The terms and conditions document, though often lengthy, is a critical part of the application process. This document lays out the rights and responsibilities of both the bank and the account holder. It will detail the fees, withdrawal limits, penalties, and other crucial aspects of the savings account. While it might be tempting to skim through, understanding these terms is vital. It ensures that there are no unpleasant surprises in the future and that the account holder can make the most of the services offered. Once the application is approved, most banks require an initial deposit to activate the account. The amount varies from one institution to another. While some might have a nominal requirement, others, especially high-yield accounts, might stipulate a more substantial initial deposit. This deposit is not a fee but rather the first step in your savings journey. It signifies the start of a relationship between the individual and the bank, a partnership geared towards financial growth and stability. By setting up online access, you can monitor your balance, transfer funds, set up automatic deposits, and manage many other banking functions from the comfort of your home or on the go. Security is a paramount concern for banks. With multi-factor authentication, encrypted transactions, and constant monitoring, online banking has become safer than ever. For those unfamiliar with the digital landscape, banks often offer tutorials and helplines to guide customers through the online banking experience. Characterized by its simplicity and user-friendliness, this account type is a go-to for those taking their initial steps into the world of personal finance. While it provides a secure space to store and grow funds, the interest rates are generally on the lower spectrum compared to other savings vehicles. These accounts are especially appealing to those aiming to earn a more substantial return on their savings without diving into riskier investments. Often provided by online banks, which can afford higher interest rates due to lower overhead costs, these accounts are a bridge between conventional savings and investment options. MMA strikes a balance between a checking and savings account. Offering competitive interest rates, often higher than regular savings accounts but slightly lower than high-yield accounts, MMAs also provide some check-writing privileges. This makes them suitable for those looking for a mix of decent returns with some transactional flexibility. They're ideal for individuals who can maintain a higher balance and want a blend of savings and checking features. This is a time-bound savings tool. When you open a CD, you agree to deposit a sum of money for a specified period, ranging from a few months to several years. In return, the bank offers a fixed interest rate, typically higher than what regular savings accounts provide. CDs are excellent for individuals with a clear understanding of their financial needs in the coming years. If you're sure you won't need the deposited money within the CD's tenure, they offer a risk-free way to get a higher return on your savings. IRAs are tax-advantaged savings accounts designed to help individuals save for retirement. Two primary types exist: Traditional and Roth IRAs. With Traditional IRAs, contributions are often tax-deductible, but withdrawals during retirement are taxed. In contrast, Roth IRA contributions are made with post-tax dollars, but withdrawals during retirement are typically tax-free. HSAs are another type of tax-advantaged account, but these are explicitly designed to help individuals save for medical expenses. HSAs are paired with high-deductible health insurance plans. Contributions to HSAs are tax-deductible, and the money grows tax-free if used for qualified medical expenses. Moreover, HSAs often come with a debit card, making it convenient to pay for medical expenses directly from the account. When it comes to selecting the right savings account, the vast number of options can seem overwhelming. By considering the following factors and steps, you'll be better equipped to make a choice that aligns with your needs and aspirations. Short-Term vs Long-Term: Are you saving for a short-term goal like a vacation, or are you looking at long-term objectives like retirement or buying a house? Different accounts cater to various timeframes. Accessibility: If you anticipate needing frequent access to your funds, a regular savings or money market account might be more appropriate. On the other hand, if you're setting aside money for the distant future, CDs or retirement accounts could be more fitting. Competitive Rates: Compare the annual percentage yields (APY) of various banks. Online banks often offer higher interest rates because they have lower overhead costs. Compound Interest: Consider how often the interest is compounded. Daily compounding can grow your money faster than monthly or yearly compounding. Monthly Fees: Some banks charge monthly maintenance fees, which can eat into your savings. Look for accounts that either don't have these fees or offer ways to waive them. Minimum Balance Requirements: Ensure you're comfortable with any minimum balance requirements, especially if not maintaining that balance results in fees. ATM Access: If you value being able to withdraw money from an ATM, check whether the bank offers a broad network of fee-free ATMs. Online and Mobile Banking: In today's digital age, robust online banking features, including mobile check deposit, fund transfers, and digital statements, can be invaluable. Loyalty Programs and Bonuses: Some banks offer sign-up bonuses or loyalty rewards for maintaining a certain balance or setting up regular deposits. Overdraft Protection: If you also have a checking account with the same bank, some savings accounts offer overdraft protection, which can be a lifesaver. FDIC or NCUA Insurance: Ensure the bank or credit union is insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA). This insurance covers up to $250,000 per depositor, per institution. Customer Service: Sometimes, the quality of customer service can make all the difference, especially if you run into any issues. Recommendations: Speak to family and friends about their experiences with their banks. Personal recommendations can often provide insights that you might not find in official reviews. A savings account serves as a secure and accessible deposit option for individuals and businesses to set aside funds they don't need immediate access to. When opening a savings account, choosing the right bank or credit union is crucial, considering factors like global access, community-driven initiatives, or online convenience. Deciding on the type of account, be it a standard savings account, high-yield savings account, money market account, certificate of deposit (CD) account, or an Individual Retirement Account (IRA), depends on specific financial goals and risk preferences. With a focus on fees, minimum balance requirements, interest rates, and technology, individuals can make an informed decision to ensure their savings grow efficiently. A well-chosen savings account can provide financial stability and growth, supporting individuals in achieving both short-term and long-term financial objectives.What Is a Savings Account?

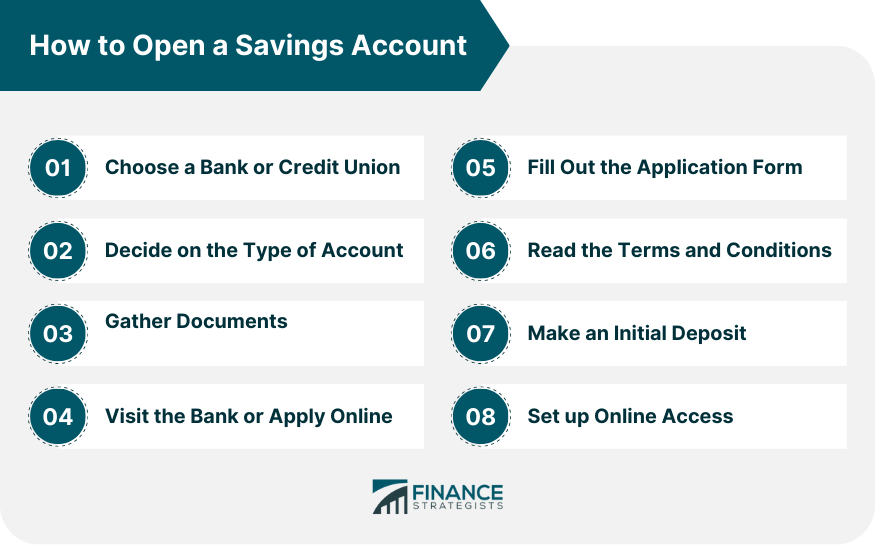

How to Open a Savings Account

Choose a Bank or Credit Union

Decide on the Type of Account

Gather Documents

Visit the Bank or Apply Online

Fill Out the Application Form

Read the Terms and Conditions

Make an Initial Deposit

Set up Online Access

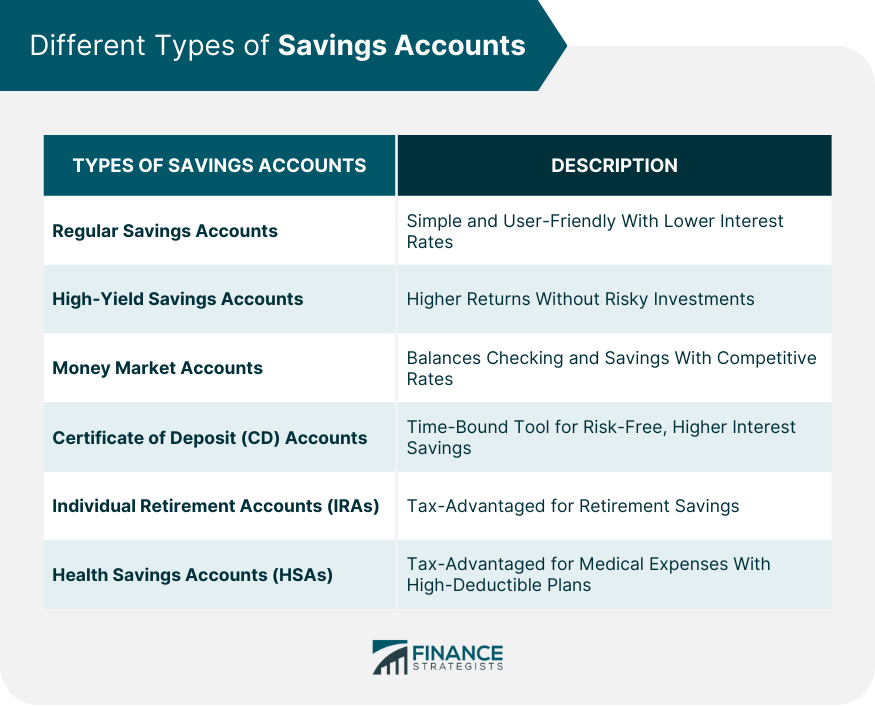

Types of Savings Accounts

Regular Savings Accounts

High-Yield Savings Accounts

Money Market Accounts

Certificate of Deposit (CD) Accounts

Individual Retirement Accounts (IRAs)

Health Savings Accounts (HSAs)

How to Choose a Savings Account

Determine Financial Goals

Research Interest Rates

Evaluate Fees and Minimums

Consider Accessibility and Technology

Review Additional Features

Understand the Safety of Your Money

Personal Preferences and Recommendations

Conclusion

How to Open a Savings Account FAQs

To open a savings account at a bank, visit the nearest branch, bring valid identification and proof of address, fill out the application form, and make an initial deposit.

To open a savings account online, choose a reputable online bank, visit their website, fill out the online application form, and provide the required documents electronically.

To open a savings account at a credit union, find a local credit union that suits your needs, visit their branch or website, provide necessary documents, and complete the account opening process.

If you don't have a Social Security Number, you can use an Individual Taxpayer Identification Number (ITIN) to open a savings account at some banks or credit unions.

To choose the right type of savings account, consider your financial goals, time horizon, interest rates, fees, and accessibility. Evaluate options like regular savings, high-yield savings, money market accounts, CDs, or IRAs to find the best fit for your needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.