A checking account is a type of bank account designed for everyday financial transactions, including deposits, withdrawals, payments, and transfers. Unlike savings accounts, which are typically used to store money over time, checking accounts are built for frequent use and easy access to funds. Checking accounts generally come with features such as debit cards, online and mobile banking, and the ability to send or receive electronic payments. These tools make it possible to manage money efficiently, whether paying for goods and services, transferring funds, or monitoring account activity in real time. Minors generally cannot open checking accounts independently due to legal restrictions around contracts. A parent or legal guardian must be involved as a co-owner or custodian of the account. This adult assumes responsibility for overseeing the account and, in many cases, shares liability for any overdrafts or misuse. Age requirements vary by institution, but most banks offer accounts for children as young as 13, with some allowing even younger minors to participate under stricter parental control. The structure ensures that financial institutions can maintain accountability while still providing access to basic banking services. The first decision involves selecting between a joint checking account and a youth-specific account. A joint account typically gives both the parent and the minor equal access, with the parent retaining full oversight and legal responsibility. In contrast, youth or teen accounts are often structured with built-in safeguards, such as spending limits or restricted features, to encourage responsible usage. The right choice depends on how much independence the parent is comfortable granting and how much guidance the child needs. Not all financial institutions approach minor accounts the same way. Traditional banks may offer stability and in-person support, while online banks and fintech platforms often provide more intuitive apps and real-time monitoring tools. The decision should center on usability, fee structure, and the availability of parental controls. A well-designed mobile experience can be particularly valuable, as it allows both the parent and the child to engage consistently with the account. Opening the account requires verifying both the minor’s identity and the parent’s authority. This typically includes the child’s Social Security number or equivalent identification, as well as government-issued identification for the parent or guardian. Financial institutions may also request proof of address and documentation confirming the relationship between the adult and the minor. Preparing these materials in advance can significantly streamline the process. Many banks now allow accounts for minors to be opened online, though some still require an in-person visit, particularly for younger children. The application process involves entering personal details, verifying identity, and agreeing to account terms. In some cases, both the parent and the minor must be present during account setup, especially when signatures are required. Once the account is approved, an initial deposit is typically required. At this stage, parents can also establish key controls, such as transaction alerts, spending limits, and withdrawal permissions. These settings are essential in shaping how the child interacts with money and can serve as a practical tool for financial education. Joint accounts are the most traditional option and provide full access to both the parent and the minor. This structure allows parents to monitor activity closely and intervene when necessary. However, it also places full legal responsibility on the adult, making it important to establish clear expectations with the child. Youth accounts are specifically designed for minors and often include features that promote financial literacy. These may include spending insights, savings tools, and limited transaction capabilities. Because they are tailored for younger users, they tend to strike a balance between independence and supervision. Prepaid debit cards are sometimes used as a substitute for checking accounts, particularly for younger children. While they offer controlled spending and eliminate the risk of overdraft, they lack the broader functionality of a traditional bank account. As a result, they are often best viewed as a transitional tool rather than a long-term solution. A checking account introduces minors to foundational financial concepts such as budgeting, tracking expenses, and understanding account balances. By interacting with real money in a structured environment, children begin to develop habits that can carry into adulthood, making financial education more practical and less theoretical. Having access to a checking account allows minors to engage in everyday financial activities, such as making purchases, receiving allowances, or saving for goals. This hands-on experience helps them understand the consequences of spending decisions, reinforcing accountability and awareness. A checking account simplifies routine financial interactions, including digital payments, debit card usage, and transferring funds. It provides a centralized system for managing money, which can be more efficient and secure than relying on cash or informal methods. Without proper guidance, minors may spend impulsively or fail to track their balances effectively. This can lead to poor financial habits early on, particularly if there are no safeguards or parental controls in place to reinforce discipline. Certain accounts may include fees for overdrafts, ATM usage, or maintenance. If these are not clearly understood, minors can inadvertently incur charges that diminish their account balance and create confusion about how banking systems work. In joint accounts, parents or guardians are typically held responsible for any negative balances or misuse. This shared liability means that a child’s financial mistakes can directly impact the adult, making oversight and communication essential. Determining the right balance between control and independence is one of the most important aspects of managing a minor’s checking account. Too much control can limit learning opportunities, while too little can expose the child to unnecessary risks. An effective approach often involves gradually increasing autonomy over time. Parents can begin with strict oversight and progressively relax restrictions as the child demonstrates responsible behavior. This method not only builds trust but also reinforces financial accountability. One of the most overlooked issues when opening a checking account for a minor is the fee structure. Some accounts advertise themselves as “free” but include charges for overdrafts, ATM usage, inactivity, or falling below a minimum balance. These fees can quietly erode the account balance and create confusion for minors who are still learning how money works. Parents should carefully review the terms and conditions to ensure the account truly supports learning rather than penalizing inexperience. A checking account without clear expectations can quickly become a source of poor financial habits. If minors are not given boundaries around spending, saving, and account usage, they may treat the account as unlimited access to money. Establishing simple rules—such as how much can be spent, what types of purchases are allowed, and how often balances should be checked—helps create structure and reinforces accountability. Many modern accounts offer built-in features such as transaction alerts, spending limits, and real-time monitoring. Failing to activate or use these tools removes an important layer of guidance. These features are not meant to restrict independence entirely, but rather to provide visibility and opportunities for discussion. When used effectively, they can turn everyday transactions into teachable moments. Overdrafts can be one of the most costly and confusing aspects of a checking account. If overdraft protection is not clearly understood or properly configured, minors may accidentally spend more than what is available in the account. This can result in fees or negative balances, which the parent is often responsible for covering. It is important to either disable overdraft features or explain them thoroughly so the minor understands the consequences. Some parents choose accounts solely based on ease of use or brand familiarity, without considering their educational value. While convenience is important, the primary goal of opening a checking account for a minor should be to build financial skills. Accounts that include spending insights, savings tools, or educational features can provide significantly more long-term benefit than those that simply function as a place to store money. Many parents focus on the initial setup of the account but fail to consider what happens when the minor turns 18. Without planning, this transition can lead to confusion around account ownership, access, and responsibility. Discussing this shift early and understanding the bank’s policies ensures a smoother transition and reinforces the idea that financial independence is a gradual process rather than an abrupt change. Opening a checking account for a minor can be a highly effective way to introduce financial responsibility, provided it is done thoughtfully. The decision should be guided by the child’s maturity level, the parent’s willingness to stay involved, and the features offered by the financial institution. When implemented correctly, a checking account becomes more than just a financial tool. It becomes a practical framework for teaching discipline, decision-making, and long-term financial awareness—skills that extend far beyond childhood.Overview of Checking Accounts

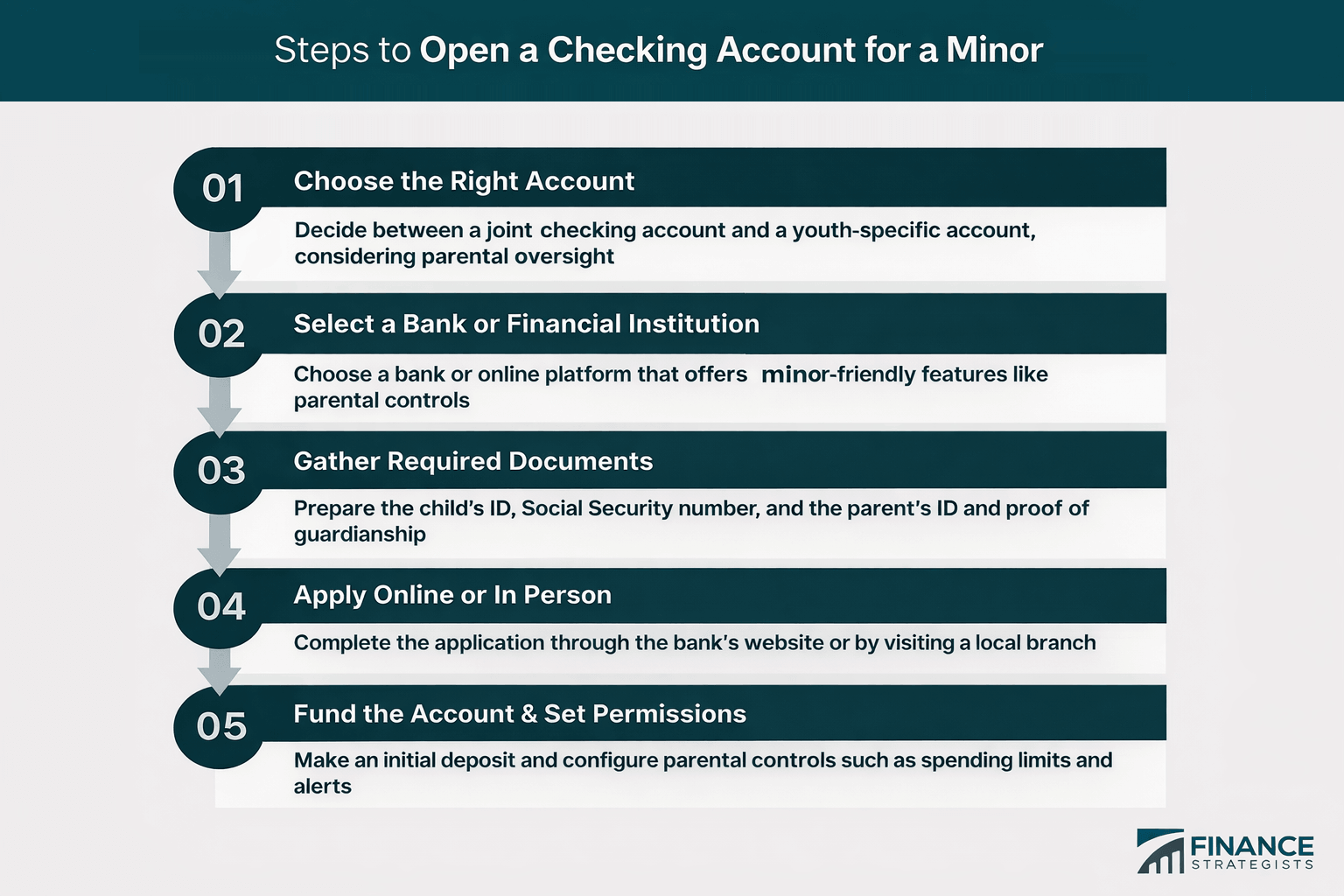

Steps to Open a Checking Account for a Minor

Step 1: Choose the Right Type of Account

Step 2: Select a Bank or Financial Institution

Step 3: Gather Required Documents

Step 4: Apply Online or In Person

Step 5: Fund the Account and Set Permissions

Types of Checking Accounts for Minors

Joint Checking Accounts

Teen or Youth Checking Accounts

Prepaid Debit Alternatives

Benefits of Opening a Checking Account for a Minor

Early Financial Literacy Development

Real-World Money Management Experience

Convenience and Practical Use

Potential Drawbacks of Opening a Checking Account for a Minor

Risk of Overspending

Exposure to Fees and Penalties

Parental Financial Liability

How Much Control Should Parents Have?

Common Mistakes to Avoid

Choosing Accounts With Hidden Fees

Failing to Set Clear Usage Guidelines

Not Using Parental Controls and Monitoring Tools

Ignoring Overdraft Policies

Prioritizing Convenience Over Education

Not Preparing for the Transition to Adulthood

Final Thoughts

How to Open a Checking Account for a Minor FAQs

In most cases, minors cannot open a checking account independently. A parent or legal guardian is required to serve as a co-owner or custodian due to legal limitations.

The minimum age varies by institution, but many banks offer accounts starting around age 13. Some institutions provide options for younger children with additional parental controls.

Many banks offer fee-free accounts for minors, though this is not universal. It is important to review the fee structure carefully before opening an account.

Yes, most minor accounts include a debit card and access to online or mobile banking. These features are typically accompanied by parental controls to ensure safe usage.

The account typically converts into a standard adult checking account, and the parent may be removed as a co-owner depending on the bank’s policies.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.