A bank account signifies a financial contract between a bank and the account holder, an individual or an organization. Under this contract, the bank holds and safeguards the account holder's funds while also tracking all associated transactions. These funds can be deposited, withdrawn, and managed by the account holder in adherence to the bank's policies. A bank account serves as a reliable and secure place to store money. Unlike physical cash, money in a bank account is not susceptible to loss or theft. Moreover, a bank account plays a pivotal role in the economic lives of people and businesses. It simplifies financial transactions, such as receiving salaries, paying bills, or transferring money to different accounts. Bank accounts also help build a credible financial history, which can prove beneficial when seeking credit or loans in the future. The process of opening a bank account involves several requirements and procedures that ensure the legitimacy and security of the account. Here's a more detailed explanation: To open a bank account, you need to start by filling out an application provided by the financial institution. The application collects essential information about you and the type of account you wish to open. As part of the application, you'll be required to provide valid identification, such as a government-issued driver's license, passport, or any other form of official identification. This helps the bank verify your identity and comply with anti-money laundering regulations. In many countries, banks require applicants to provide their social security number or a similar identification number unique to that country. This further aids in confirming your identity and ensures proper taxation and financial reporting. You'll also need to present proof of your residential address. This could be in the form of utility bills, rental agreements, or official government documents that show your name and address. Once you've submitted the application and necessary documents, the bank will verify the information provided. This verification process is essential for preventing identity theft and fraudulent activities. After successful verification, the bank will review your application and determine whether you meet their account-opening criteria. If approved, you'll be notified, and the bank will proceed with the account opening process. In most cases, banks require an initial deposit to officially open the account. This deposit amount may vary depending on the type of account you're opening and the bank's policies. Once your account is officially open, you'll receive your account details, which typically include an account number, routing number (for checking accounts), and other relevant information. You can then start using your bank account for various financial transactions and benefit from the numerous advantages it offers, such as secure money storage, access to financial services, and potential interest earnings on your deposits. Money can be deposited into a bank account through various modes. Cash deposits can be made at bank branches or ATMs. Checks can be deposited at the bank, via ATMs, or even through mobile banking apps in many cases. Electronic transfers, direct deposits of wages, and wire transfers are other common methods of depositing money. Banks offer multiple channels to withdraw money from an account. Account holders can write checks, withdraw cash at ATMs, or use debit cards for purchases where the money gets deducted directly from the account. Electronic payments for bills or other services also result in the withdrawal of money. While many banks offer unlimited withdrawals, some might have restrictions on the number and type of withdrawals made within a specific period. Modern banking systems have made fund transfers quite straightforward. Money can be moved between accounts within the same bank or transferred to accounts at different banks. These transfers can be scheduled or made instantly, and can usually be executed via online banking, phone, or in person. Many banks offer wire transfer services for both domestic and international transfers. Furthermore, integration with mobile payment services has simplified peer-to-peer transactions. Account holders typically receive monthly statements from their banks, detailing the account's transaction history, current balance, accrued interest, and any fees incurred. With the advent of online and mobile banking, account management has expanded beyond traditional banking hours and locations. These platforms offer real-time balance checks, mobile check deposit features, bill payment options, and even more sophisticated services like budgeting tools and financial planning. Banks play a pivotal role in financial ecosystems, serving as intermediaries that channel deposited funds into profitable lending ventures. Here's an elucidated overview of how banks manage and distribute interest: When you entrust your money to a bank, it's not merely stored. Banks utilize these deposits as a reservoir to offer loans to individuals, enterprises, and various entities. These loans span multiple needs: mortgages, automobile financing, personal loans, or business expansions. Banks levy an interest charge on the lent amount to borrowers. Notably, the interest rate imposed on these loans usually surpasses the rate given to depositors. This rate differential is the cornerstone of a bank's earning strategy. Interest accrued from loans isn't just revenue; it's a lifeline. It shoulders the bank's operational expenses, fortifies financial reserves, and ensures shareholders receive their due dividends. Banks reward depositors by disbursing a part of their loan interest earnings. This interest, however, is contingent on several determinants: Account Type: Distinct accounts like savings or high-yield accounts traditionally proffer superior interest rates than standard checking accounts. Institutional Policies: Individual bank regulations, shaped by market dynamics, competitive pressures, or regulatory financial policies, dictate interest rates. Economic Climate: Macro-economic indicators, such as inflation rates or central bank directives, can modulate the interest dispensed to depositors. Banks impose various fees to cover their operational costs and generate revenue. Some of the common fees include: Monthly Maintenance Fees: These fees are charged for keeping your account active and may vary based on the type of account you have. Overdraft Charges: If you spend more money than you have in your account, resulting in a negative balance, the bank may charge overdraft fees. ATM Usage Fees: When you use an ATM that is not affiliated with your bank's network, the bank may charge an ATM usage fee in addition to any fees charged by the ATM operator. Minimum Balance Fees: Some accounts require you to maintain a minimum balance, and failure to do so may result in a minimum balance fee. Transaction Fees: Certain transactions, such as wire transfers or cashier's checks, may incur additional fees. Foreign Transaction Fees: If you use your debit card for transactions in foreign countries, the bank may charge foreign transaction fees. However, many of these fees can be avoided by being aware of your bank's fee structure and following some simple practices: Choose the Right Account: Research different account options and choose one that aligns with your banking habits. Some accounts may offer fee waivers or lower fees based on certain criteria. Maintain Minimum Balance: Regularly check your account balance to ensure it meets the minimum requirements. Keeping the minimum balance can help avoid minimum balance fees. Monitor Transactions: Keep track of your spending and avoid overdrawing your account. Set up alerts for low balances to avoid accidental overdrafts. Use In-Network ATMs: Stick to your bank's ATM network to avoid additional ATM usage fees. Alternatively, consider banks with widespread ATM networks. Online Banking: Opt for online banking services to perform transactions and check account details, reducing the need for in-branch transactions and associated fees. Review Fee Schedules: Familiarize yourself with your bank's fee schedule to know which actions may incur charges. Negotiate With the Bank: In some cases, you may be able to negotiate fee waivers or reduced fees, especially if you have a long-standing relationship with the bank. Banks employ robust security measures to protect the financial assets and personal information of their customers. These measures include advanced encryption for online transactions, secure ATM technologies, and continuous fraud monitoring systems. These layers of protection help ensure the safety of transactions and prevent unauthorized access to account information. In the United States, deposits in a bank account are insured by the Federal Deposit Insurance Corporation (FDIC). The FDIC guarantees that even if a bank were to fail, each account holder would still receive their deposits up to a limit of $250,000 per bank. This guarantee instills confidence in the banking system and protects account holders from losing their money. While banks implement rigorous security measures, account holders also bear responsibility for protecting their accounts. This can be achieved by routinely monitoring account activities, using secure internet connections for transactions, promptly reporting any suspicious transactions to the bank, and keeping banking credentials confidential. Storing money in a bank account is significantly safer than keeping large amounts of cash. Money in the bank is not only protected from physical theft but also insured against bank failure. Bank accounts provide easy access to funds through various channels, like ATMs, checks, debit cards, and online banking. This easy access makes handling financial transactions a convenient process, whether you're paying bills, purchasing goods, or transferring money. Bank accounts play a crucial role in managing personal or business finances. By tracking income and expenditure, they facilitate budgeting, planning, and overall financial management. This tracking can also prove beneficial during tax preparation and any situation where financial documentation is required. Bank accounts often act as gateways to other financial services and products. Account holders may have access to credit cards, loans, mortgages, and investment options. Some banks also offer premium services to account holders who maintain a certain balance. Despite their many benefits, bank accounts can come with potential downsides. If not managed well, account holders can incur various fees. These can include account maintenance fees, minimum balance fees, overdraft charges, and penalties for excessive transactions. While online banking has revolutionized the accessibility of banking services, it can pose challenges for certain demographics. Individuals in rural areas without reliable internet access or those not comfortable with digital technology may find it difficult to access or manage their accounts online. As much as technology has improved banking accessibility, it has also introduced risks. Cybersecurity threats such as phishing, identity theft, and fraud can compromise a bank account's security. Account holders must therefore be vigilant and follow best practices to protect their account information. Bank accounts are secure places to store money and conduct financial transactions. They can be opened by submitting an application, valid identification, social security number, and proof of residence. Banks facilitate deposits, withdrawals, fund transfers, and account management. Interest on deposits is paid from the profit banks earn from lending deposited funds. To avoid incurring fees such as monthly maintenance, overdraft charges, and ATM usage fees, it is important to maintain a minimum balance, monitor transactions, and use in-network ATMs. Banks employ security measures and are insured by organizations like the FDIC in the U.S., ensuring account holders' deposits up to a certain limit. Although online and mobile banking has revolutionized accessibility, potential risks include cyber threats like phishing and fraud. Regular account monitoring, making the most of online services, and utilizing additional bank services can optimize the use of bank accounts.Overview of Bank Accounts

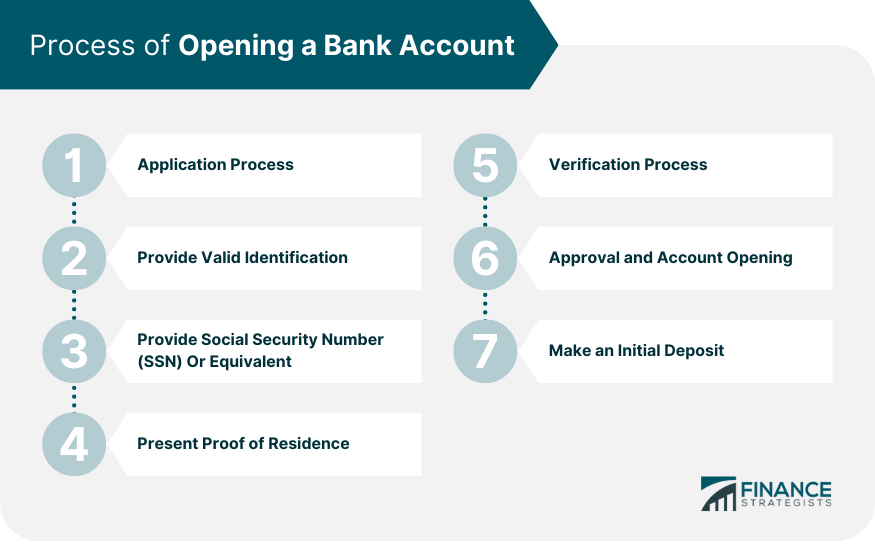

Process of Opening a Bank Account

Application Process

Provide Valid Identification

Provide Social Security Number (SSN) or Equivalent

Present Proof of Residence

Verification Process

Approval and Account Opening

Make an Initial Deposit

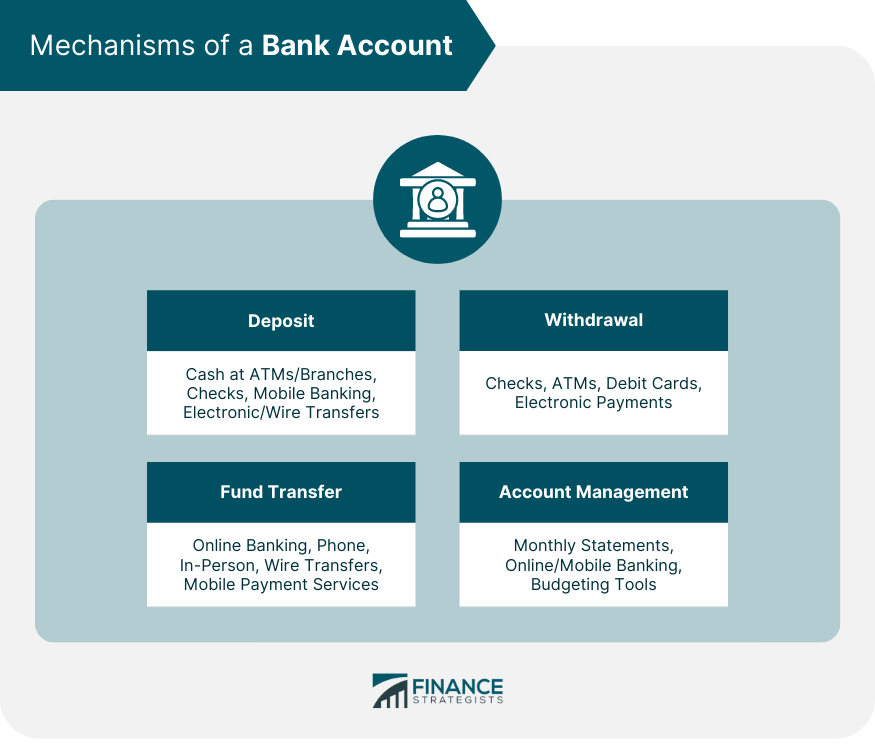

Mechanisms of a Bank Account

Deposit

Withdrawal

Fund Transfer

Account Management

Interests and Bank Fees

How Banks Allocate and Earn Interest

Leveraging Deposits for Loans

Earning Through Loan Interest

Income Generation

Distributing Interest to Depositors

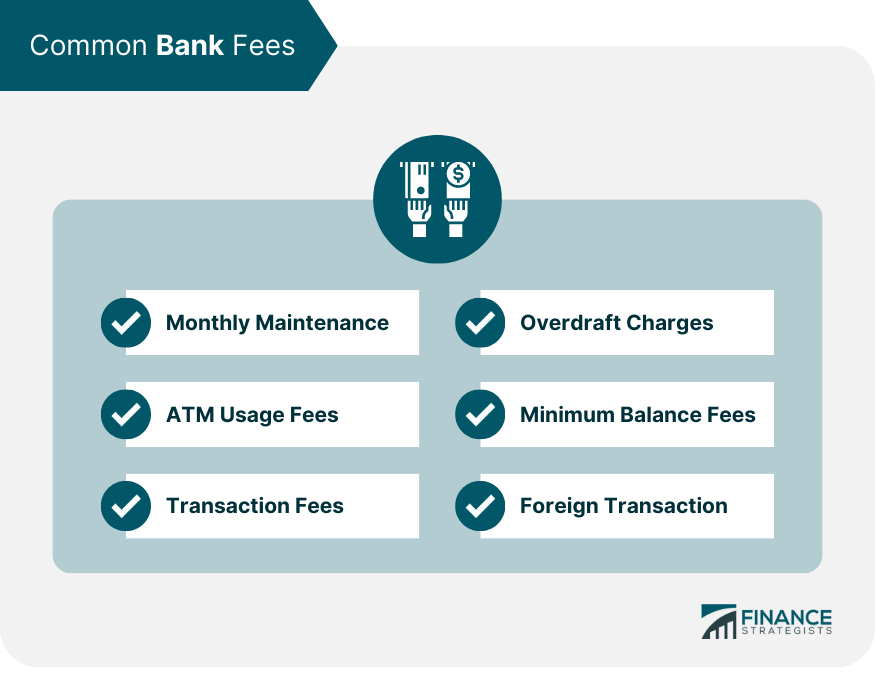

Common Fees

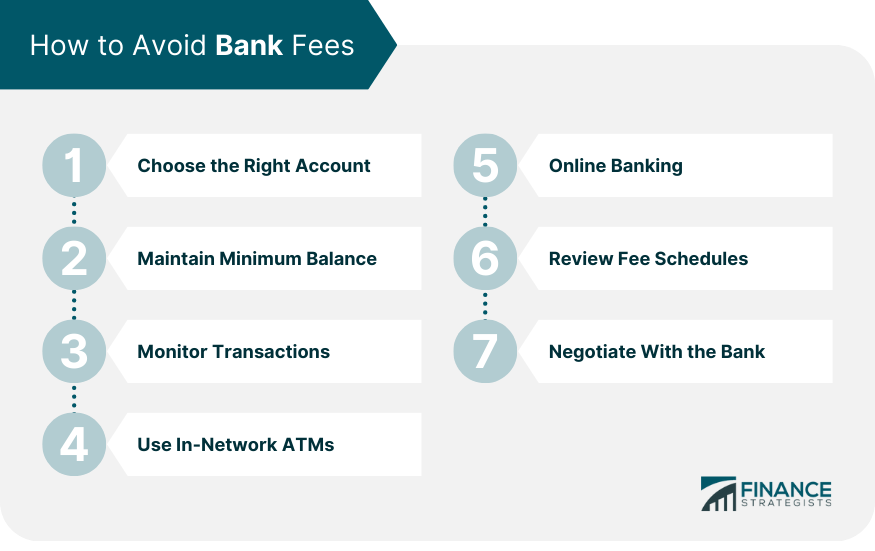

How to Avoid Bank Fees

Safety and Security in Banking

Bank's Security Measures

FDIC Insurance

How to Protect Your Bank Account

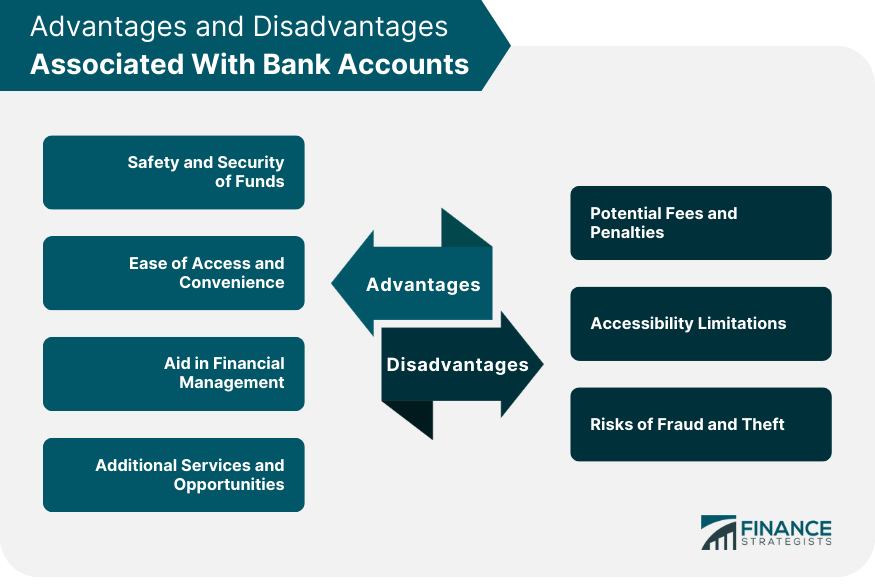

Advantages of Using Bank Accounts

Safety and Security of Funds

Ease of Access and Convenience

Aid in Financial Management

Additional Services and Opportunities

Challenges Associated With Bank Accounts

Potential Fees and Penalties

Accessibility Limitations

Risks of Fraud and Theft

Conclusion

How Bank Accounts Work FAQs

Bank accounts work as a financial contract between an individual or organization and a bank. The bank holds and safeguards the account holder's funds while allowing deposits, withdrawals, and fund transfers as per their policies.

To open a bank account, start by filling out an application with essential information. Provide valid identification, such as a driver's license and proof of residence. The bank will verify the details, and upon approval, an initial deposit is required to officially open the account.

Bank interest rates are typically determined by the central bank's policies, market conditions, and competition among banks. The rate paid to account holders may vary based on the type of account and the prevailing economic environment.

To avoid bank fees, choose the right account based on your banking habits, maintain the minimum balance required, monitor transactions to avoid overdrafts, and use in-network ATMs. Utilize online banking services and negotiate with the bank for possible fee waivers.

Banks employ robust security measures, including advanced encryption for online transactions, secure ATM technologies, and continuous fraud monitoring systems. In the United States, deposits in bank accounts are insured by the FDIC, guaranteeing up to $250,000 per bank in case of a failure. Account holders must also protect their accounts by monitoring activity, using secure internet connections, and keeping credentials confidential.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.