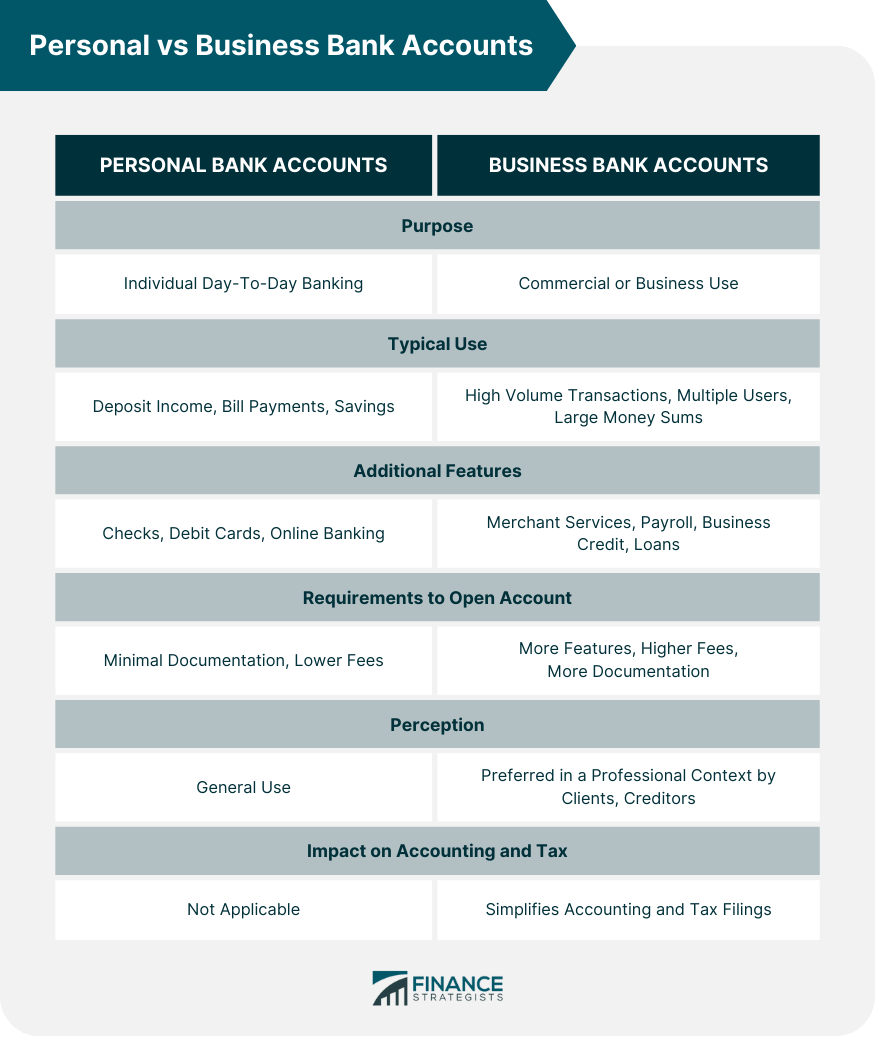

Using a Personal Bank Account for Business is the practice of managing both personal and business finances through a single account. This approach might initially seem convenient, reducing the number of accounts to manage and potentially lower banking fees. However, the disadvantages often outweigh these benefits. Mixing personal and business finances can result in confusion in record-keeping and tax reporting, restrict business growth due to transaction limits, and expose you to legal risks, especially for LLCs and corporations. Separating business and personal finances is generally advised, offering better financial organization, clearer tax filings, and protection of personal assets. Despite the simplicity of using a personal bank account, transitioning to a dedicated business account is recommended for the sustainable growth and success of a business. Personal bank accounts are generally designed for individual use, covering day-to-day banking needs. They're used for depositing income, withdrawing cash, paying bills, and saving. They typically come with personal checks, debit cards, and options for online banking and automatic payments. Some personal accounts also offer interest-earning savings options. On the other hand, business bank accounts are built specifically for commercial or business use. They're designed to handle a higher volume of transactions, multiple users, and large sums of money. Business bank accounts may offer a variety of services, including merchant services, payroll processing, business credit, and loan options. They are usually required for corporations, but even for sole proprietorships and partnerships, it can be beneficial. While personal and business bank accounts might seem similar, they cater to different needs. Business accounts typically come with more features, higher fees, and require more documentation to open. They are also seen more favorably in a professional context by clients and creditors. Most importantly, keeping business transactions separate simplifies accounting and tax filings. Operating a business through a personal bank account can seem simpler. It means one less account to manage, one less set of banking fees to pay, and one less relationship to maintain with a bank. Starting a business often involves many costs. By using a personal account for business transactions, you can avoid the additional charges that come with business accounts, such as maintenance fees, transaction fees, and other banking service fees. Opening a business bank account often requires more paperwork and more time than opening a personal account. It may also require a business license or incorporation documents. As your business grows, it might outgrow the limits of a personal account. A business account can handle more transactions and larger sums of money. For corporations and limited liability companies (LLCs), maintaining separate business and personal finances is crucial to preserve the business's limited liability status. Mixing personal and business finances can result in a court "piercing the corporate veil," which can make you personally liable for business debts. Mixing personal and business expenses in a single account can make it difficult to track business income and expenses. This could lead to errors in financial reporting and tax filings. Using a personal bank account for business can blur the line between personal and business finances. This could have serious implications, particularly for corporations and LLCs. Sole proprietorships face fewer legal risks from using a personal account for business. However, for LLCs and corporations, the risks can be significant. Mixing personal and business finances can jeopardize the company's limited liability status, potentially exposing personal assets to business debts. Mixing personal and business finances can make it harder to accurately report income and expenses. This can lead to incorrect tax returns, penalties, and even audits. Keeping business and personal transactions separately can simplify record keeping. Clear financial records make it easier to prepare financial statements, file taxes, and provide a clear trail for auditors. To avoid complications, it's advisable to keep business and personal transactions separate. Consider using software to track expenses, and consult with a tax advisor to ensure you're following best practices. Set up a Separate Business Bank Account: A separate business bank account helps ensure clear financial record keeping, protects the owner's personal assets, and adds legitimacy to the business. Use of Online Financial Management Tools: Digital financial management tools can help keep track of business expenses, even when using a personal bank account for business. Hybrid Accounts: Some banks offer hybrid accounts, designed for freelancers or micro-businesses, that provide the benefits of business accounts while maintaining the simplicity of personal ones. Steps in Opening a Business Account: To open a business account, you'll generally need your business's EIN (or your SSN if you're a sole proprietor), your business's legal documents, and a business license. Transition Business Finances: Once your business account is open, start moving business transactions to the new account. It might take some time, but separating your personal and business finances is worth the effort. Potential Challenges and How to Overcome Them: Transitioning can be a complex process, especially if business transactions are entwined with personal ones. It's advisable to consult with a business accountant to navigate this process. While using a personal bank account for business might initially seem simpler and cost-effective, it presents significant limitations and risks. It can constrain business growth, introduce legal liabilities, and complicate record-keeping and tax reporting. Business bank accounts, on the other hand, are tailored for commercial use and facilitate clear financial management. They are generally perceived more favorably in professional contexts, and they simplify tax filing and accounting processes. The legal implications of mixing personal and business finances can be serious, particularly for corporations and LLCs. For seamless and effective financial management, it is advisable to establish a separate business bank account, make use of online financial management tools, or consider hybrid accounts. Transitioning from a personal to a business account may present challenges, but it is a worthwhile endeavor that can be facilitated by consulting with a business accountant.Using a Personal Bank Account for Business

Distinguish Between Personal and Business Bank Accounts

Features of Personal Bank Accounts

Features of Business Bank Accounts

Key Differences Between Personal and Business Accounts

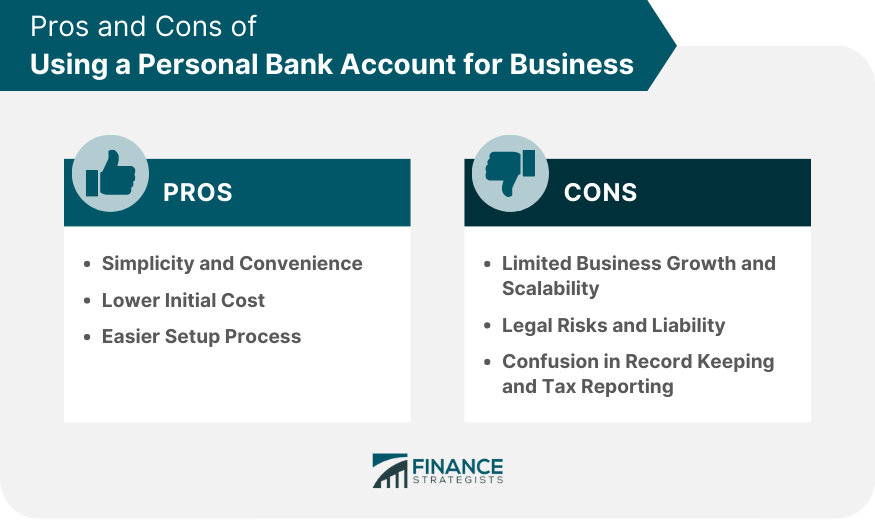

Pros and Cons of Using a Personal Bank Account for Business

Pros

Simplicity and Convenience

Lower Initial Cost

Easier Setup Process

Cons

Limited Business Growth and Scalability

Legal Risks and Liability

Confusion in Record Keeping and Tax Reporting

Legal Implications of Using a Personal Bank Account for Business

Overview of Legal Aspects

Potential Risks for Different Business Structures

Tax Implications of Using a Personal Bank Account for Business

Explanation of Potential Tax Issues

Importance of Clear Financial Record Keeping

Tips for Avoiding Tax Complications

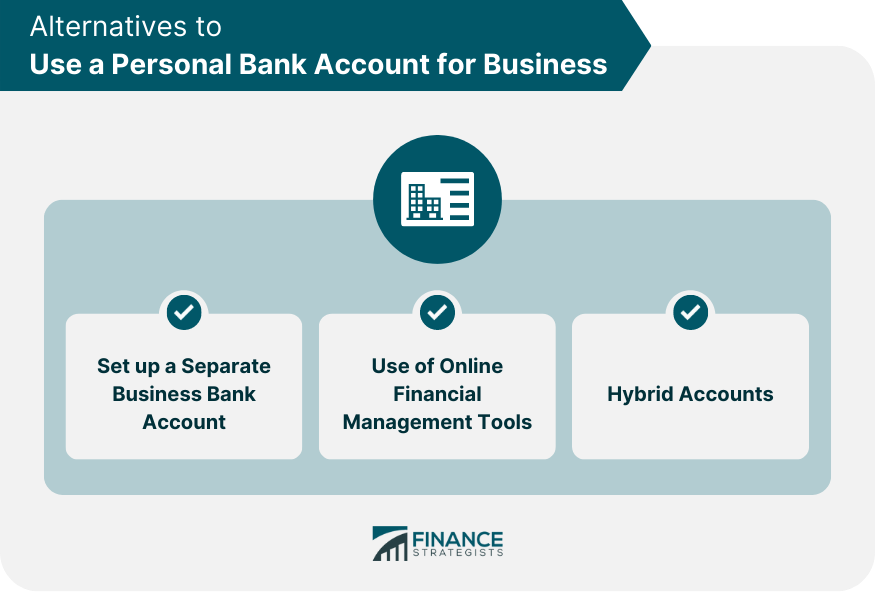

Alternatives to Use a Personal Bank Account for Business

How to Transition From Personal to Business Bank Account

Bottom Line

Using a Personal Bank Account for Business FAQs

Yes, you can, especially if you're a sole proprietor. However, it's not advisable due to potential legal and tax complications, and it may limit your business's growth.

The main advantages include simplicity, lower initial costs, and an easier setup process. You have one less account to manage, you avoid the extra fees of a business account, and the process of setting up a personal account is usually simpler.

The disadvantages include potential legal risks, confusion in record keeping and tax reporting, and limitations to business growth and scalability. If you operate an LLC or corporation, using a personal bank account for business can endanger your limited liability status.

For corporations and LLCs, using a personal account for business transactions can potentially expose your personal assets to business debts and liabilities. This is due to a legal principle known as "piercing the corporate veil."

Start by opening a business bank account with your EIN (or SSN for sole proprietors) and necessary legal documents. Then, gradually move your business transactions from your personal account to your new business account. A business accountant can provide guidance throughout this process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.