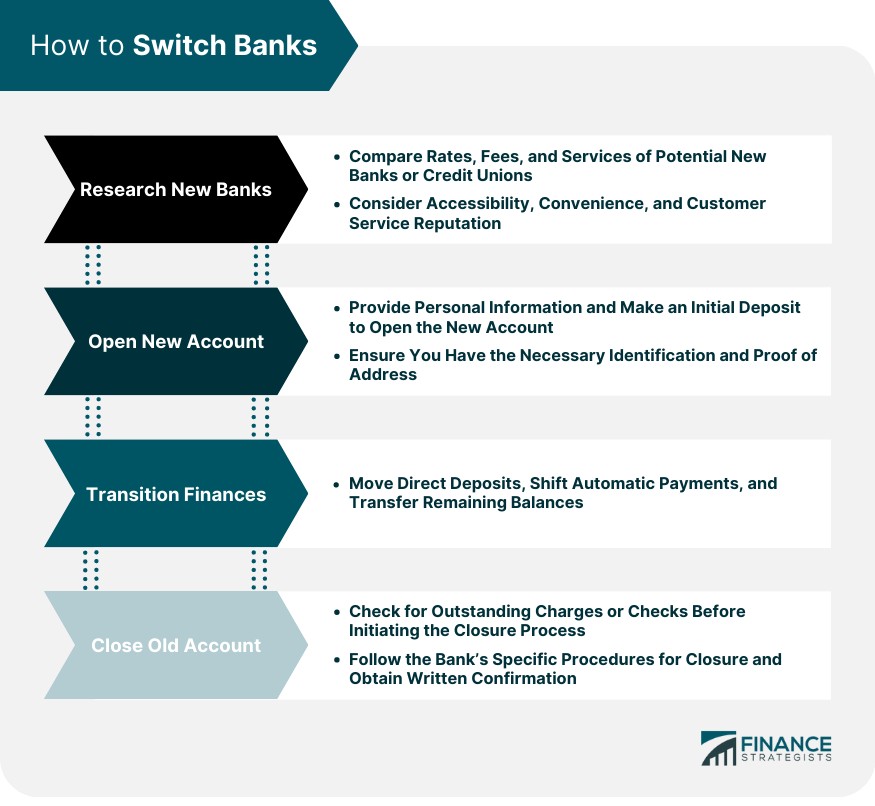

Switching banks, though may appear daunting, can be a strategic move for better services, lower fees, higher interest rates, or superior digital features. The process typically involves opening a new account at your chosen bank, transferring your funds, setting up direct deposits and automatic payments, and finally closing your old account. It's crucial to ensure all transactions have cleared and to double-check for any potential fees or penalties before closing. Managing the transition meticulously is key to avoid missed payments, overdrafts, or damaging your credit score. Some banks offer switch kits or dedicated services to ease this process. The right bank should align with your financial goals and lifestyle requirements, offering an appropriate balance of convenience, customer service, and competitive rates. Before you can open a new account, you need to find a new bank or credit union that fits your needs. Start by comparing bank rates and fees. Online platforms can help you compare different banks' offerings side by side, saving you a lot of time and effort. Remember, the right fit might be a major bank, a local credit union, or even an online-only bank. When comparing rates, look at both the interest rates for savings accounts and loan products, as well as fees for common services. You'll want a bank that offers competitive rates and low fees. This will ensure your money works harder for you. Don't underestimate the importance of convenience when choosing a bank. Consider factors like the number of branches and ATMs, the quality of the mobile and online banking platforms, the availability of customer service (such as 24/7 service or live online chat), and even the aesthetics and user-friendliness of the bank's website and app. Additionally, think about your lifestyle; if you travel frequently, global accessibility might be crucial. You want a bank that will be there for you when you need help. Research each bank's reputation for customer service. Reading reviews online or asking friends and family for their experiences can be very revealing. Consistent positive feedback can provide peace of mind in your choice. Once you've chosen your new bank, it's time to open your new account. While it might seem tedious, the effort you put into this initial step can lead to a smoother banking experience down the line. Opening a bank account is usually a straightforward process. You'll need to provide some personal information, such as your name, address, and social security number. You'll also likely need to make an initial deposit. Many banks now offer instant account setup online, making the process even more convenient. Be prepared to show identification when opening your new account. This could be a driver's license, passport, or another form of government-issued ID. You'll also need to know your social security number and may need proof of address, such as a utility bill. Ensuring you have all these documents ready can expedite the account opening process. Now that you've opened your new account, it's time to transition your finances. This is a critical phase, as any oversight can lead to missed payments or potential fees. Start by moving any direct deposits to your new account. This might include your salary, government benefits, or other regular income. Informing your employer or benefits provider early can ensure a seamless transition of funds. Next, shift any automatic payments to your new account. These might include utility bills, loan payments, or subscriptions. Maintaining a checklist of all auto-payments can be useful to ensure none are overlooked. Once you've moved all incoming and outgoing transactions to your new account, it's time to transfer any remaining balance from your old account. Using electronic transfers can speed up the process and might be cheaper than writing a check. Finally, you can close your old account. But before you do, check for any outstanding charges or checks that haven't cleared yet. Closing too early can result in unnecessary fees or complications. Before you close your old account, make sure all transactions have cleared. You don't want to be hit with overdraft charges or bounce checks. A quick review of your statement or online banking can provide clarity. To close your account, you'll likely need to contact your bank directly. Some banks allow you to do this online or over the phone, while others require a written request. Always be sure to follow the bank's specific procedures to ensure a smooth closure. Once your account is closed, get confirmation in writing. It's also a good idea to check your credit reports a few weeks later to ensure the account shows as closed. This documentation can be crucial if any disputes arise later on. Sometimes, the bank you've been with for years simply isn't the best fit for you anymore. Life changes may prompt you to reconsider your banking options. For instance, buying a home or starting a business might expose you to financial products your current bank doesn't excel in. Bank fees can eat away at your balance little by little. If your bank charges high fees for services like ATM withdrawals, check writing, balance inquiries, or has a high minimum balance requirement, it may be time to consider switching banks. Such fees, when accumulated, can significantly impact your financial health. Banks should provide excellent service. If you’re having trouble resolving issues, or you're not getting the help you need when you need it, that could be a red flag. In today’s competitive banking landscape, settling for subpar customer service isn’t necessary. Your banking needs will change over time. Perhaps your current bank isn't keeping up with these changes, offering the services or features that you require, like advanced mobile banking features, international services, or a wider range of loan products. Having a bank that evolves with your needs is essential for a long-term banking relationship. Often, switching banks can lead to better financial opportunities. These could come in the form of better interest rates for loans or savings accounts, cash bonuses for new accounts, or more rewarding credit card programs. Furthermore, many new banks or fintech firms offer innovative tools to help with budgeting, saving, and investing. One challenge you might face when switching banks is dealing with transactions that overlap the closure of your old account and the opening of your new one. It's best to keep enough money in both accounts to cover any potential overlaps. This buffer can give you peace of mind and prevent any sudden shortfalls. Be aware of any fees associated with closing your account or opening a new one. Some banks charge an account closure fee, especially if the account is being closed within a certain time frame after opening. Reading the fine print and asking questions can help you avoid unexpected charges. Maintaining continuity of services can be another challenge when switching banks. It may take time for automatic payments to be switched over to your new account, and you might need to manually pay bills in the interim to avoid late payments. Setting reminders or alarms can be an effective way to ensure you don't miss any payments during the transition. Switching banks might appear complex, but when conducted with attention to detail, it can offer numerous benefits such as better services, lower fees, or higher interest rates. The decision to switch should be influenced by various factors like product suitability, fees, customer service quality, available services, and opportunities offered by other institutions. Once a suitable alternative is identified, a step-by-step process of transitioning finances can ensure a smooth switch. Careful management of this transition can prevent missed payments, overdrafts, or damage to your credit score. Despite potential challenges such as overlapping transactions or fees, these can be managed with adequate planning. Overall, changing banks can be a strategic move to align your financial tools with your current lifestyle and future goals. If you're contemplating a bank switch, consider seeking professional advice from our expert financial advisors for personalized assistance.Overview of Switching Banks

How to Switch Banks: Step-By-Step Guide

Research Potential New Banks or Credit Unions

Compare Bank Rates and Fees

Consider Accessibility and Convenience

Evaluate Customer Service

Open New Account

Process of Opening a Bank Account

Important Documents Needed

Transition Finances

Move Direct Deposits

Shift Automatic Payments

Transfer Remaining Balances

Close Old Account

Check for Outstanding Charges or Checks

Process of Account Closure

Confirmation and Documentation

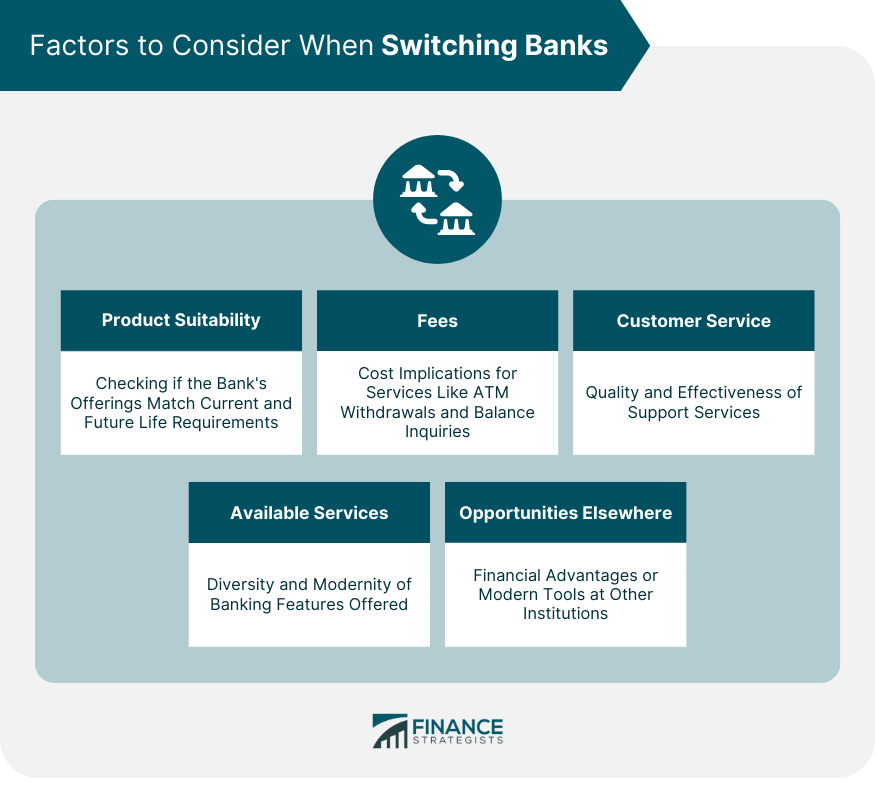

Factors to Consider When Switching Banks

Product Suitability

High Fees

Customer Service

Available Services

Opportunities Elsewhere

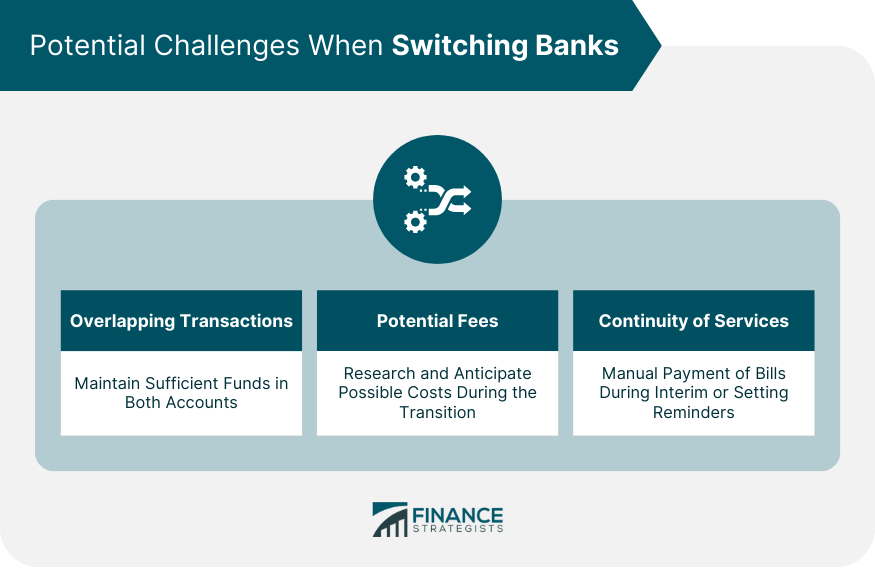

Potential Challenges When Switching Banks and How to Overcome Them

Overlapping Transactions

Potential Fees

Continuity of Services

Bottom Line

How to Switch Banks FAQs

People switch banks due to reasons like high fees, inadequate services, poor customer service, or seeking better financial opportunities elsewhere.

It's crucial to compare bank rates, fees, accessibility, convenience, and evaluate the bank's customer service reputation.

You'll need to provide personal details, possibly make an initial deposit, and present identification like a passport or driver’s license.

Transitioning requires moving direct deposits, shifting automatic payments, and transferring remaining balances from the old account.

Overlapping transactions, potential fees, and maintaining continuity of services can pose challenges during the transition.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.