A bank account beneficiary and a will beneficiary refer to individuals or entities designated to inherit assets upon the death of an account or will holder. The bank account beneficiary receives assets directly from the bank account, bypassing probate a legal process validating a will. On the contrary, a will beneficiary receives assets according to the terms of a will, but only after the will has passed through probate. Understanding the distinction between these two types of beneficiaries is crucial for effective financial and estate planning. It impacts how quickly assets are transferred after death, how they're taxed, and their legal standing. Furthermore, the context in which these terms are applied often involves personal finance, estate planning, legal proceedings, and sometimes even familial relations. A bank account beneficiary, sometimes referred to as a payable on death (POD) or transfer on death (TOD) beneficiary, is a person or entity who is designated to receive the contents of a bank account upon the account holder's passing. The purpose of designating a bank account beneficiary is to ensure the swift and efficient transfer of funds without having to go through the probate process. Essentially, naming a bank account beneficiary provides a straightforward path for your assets to reach your chosen recipients after your demise. Most banks offer the option to add a beneficiary to checking and savings accounts. This action turns the accounts into POD or TOD accounts. Retirement accounts like Individual Retirement Accounts (IRA) and 401(k)s typically require the account holder to name a beneficiary. Brokerage accounts can also have TOD provisions. Adding a beneficiary to a bank account generally requires contacting your bank and providing the beneficiary's personal details, such as their name, birth date, and Social Security number. Bank account beneficiaries have no rights to the funds in the account while the account holder is alive. Their rights commence upon the account holder's death, bypassing probate. A will beneficiary is an individual or entity explicitly named in a person's will to inherit assets or property. This person is chosen by the creator of the will, also known as the testator, to receive specific items, amounts, or percentages of the testator's total estate. The purpose of naming beneficiaries in a will is twofold: first, it ensures that the testator's possessions are allocated according to their specific wishes. Second, it helps prevent potential legal disputes that might arise in the absence of a clearly designated beneficiary. A will can include various types of assets, including real estate, personal property (like cars and furniture), bank accounts that do not have a designated beneficiary, and investments. Perhaps the most significant asset many people possess is real estate. This can range from your primary residence to vacation homes, rental properties, and undeveloped land. In your will, you can specify who inherits these properties upon your death. Personal property is a broad category encompassing anything that isn't real estate. This could include cars, furniture, jewelry, clothing, and personal collections like art, books, or vinyl records. Each of these items can be specifically mentioned in your will, ensuring they go to the intended recipients. While bank accounts can have a designated "payable on death" beneficiary, those without such a designation are included in your estate and can be covered by your will. This includes checking accounts, savings accounts, and Certificates of Deposit. Represent a significant part of many people's assets and can be included in a will. These might include stocks, bonds, mutual funds, exchange-traded funds (ETFs), and other investment accounts. However, retirement accounts like IRAs and 401(k)s typically have their own beneficiary designations and are not distributed through a will unless no beneficiary is named. If you own a portion of a business or are a sole proprietor, these business interests can be passed on through your will. This includes shares in a company, partnership interests, or sole proprietorships. If you hold patents, copyrights, or trademarks, these are also assets that can be covered in your will. These can continue to generate royalties or income after your death and can be an important part of your legacy. Naming a beneficiary in a will generally requires the assistance of an attorney to ensure that the will is legally sound. It involves identifying the assets to be included and specifying who should receive each asset. Will beneficiaries have no rights to the assets until after the testator's death and the completion of the probate process, which validates the will. A bank account beneficiary receives assets directly and almost immediately after the account holder's death. In contrast, a will beneficiary receives assets only after the will has passed through probate, which can take several months or even years. Assets left to a bank account beneficiary bypass the probate process, while assets left to a will beneficiary do not. A bank account beneficiary has no access or control over the funds until the account holder's death. However, a will beneficiary may potentially be involved in decisions concerning the assets, particularly if they are also the executor of the will. Changing a bank account beneficiary is typically a simple process of contacting the bank. Changing a will beneficiary often requires creating a codicil or a completely new will. Depending on the jurisdiction, tax implications may differ between bank accounts and will beneficiaries. In certain jurisdictions, the assets received by beneficiaries may be subject to estate or inheritance tax, which can significantly impact the net value of the inherited assets. Improper beneficiary designations can lead to legal disputes, often among family members. These disputes can result in court cases, which can delay the distribution of assets and incur significant legal costs. The designation of beneficiaries affects wealth management and estate planning strategies. Professionals in these fields can provide guidance tailored to individual situations. Life changes, such as marriage, divorce, or the birth of a child, often necessitate changes to beneficiary designations. Having multiple beneficiaries can provide a fallback if a primary beneficiary predeceases the account holder or declines the inheritance. Informing beneficiaries of their status helps avoid surprises and potential disputes after the account holder's death. Understanding the distinction between a bank account beneficiary and a will beneficiary is crucial for effective financial and estate planning. A bank account beneficiary receives assets directly from the bank account upon the account holder's death, bypassing probate. On the other hand, a will beneficiary receives assets according to the terms of a will, but only after the will has passed through probate. The key differences between these two types of beneficiaries include the distribution of assets, the probate process, rights and limitations, ease of changing beneficiaries, and tax implications. By carefully considering and designating beneficiaries, individuals can ensure their assets are distributed according to their wishes and potentially avoid lengthy legal proceedings or disputes among family members. Regularly reviewing and updating beneficiaries, choosing multiple beneficiaries as a backup, and communicating with beneficiaries are essential tips to follow.Bank Account Beneficiary vs Will Beneficiary: Overview

Understanding Bank Account Beneficiaries

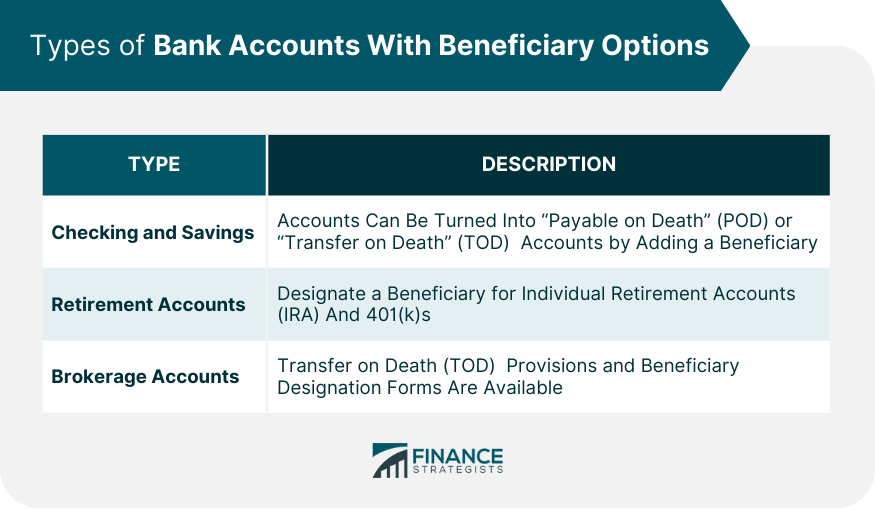

Types of Bank Accounts With Beneficiary Options

Checking and Savings Accounts

Retirement Accounts

Brokerage Accounts

How to Add a Beneficiary to a Bank Account

Rights and Limitations of Bank Account Beneficiaries

Understanding Will Beneficiaries

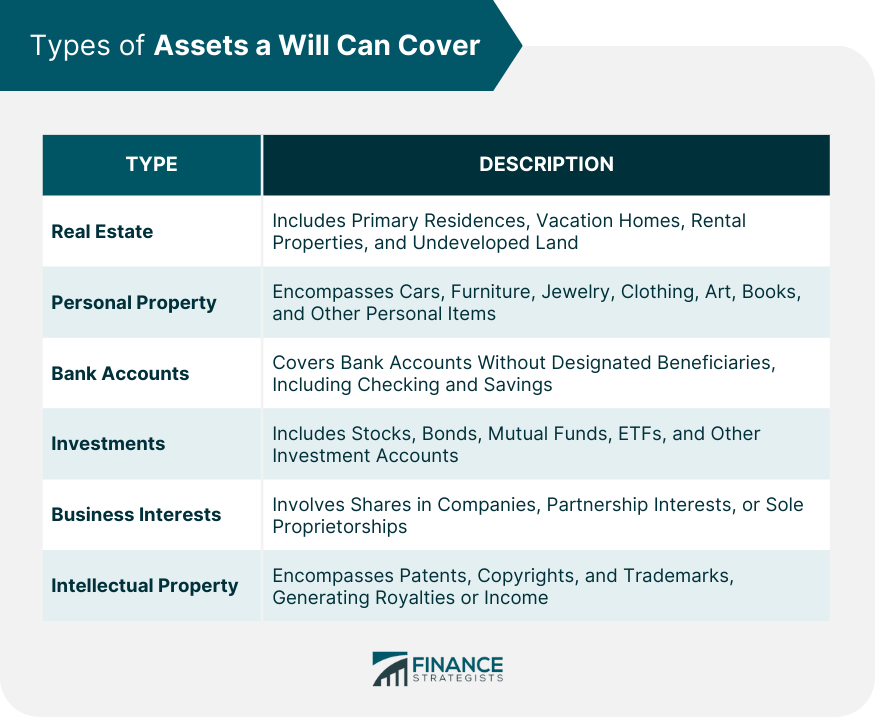

Types of Assets a Will Can Cover

Real Estate

Personal Property

Bank Accounts

Investments

Business Interests

Intellectual Property

How to Name a Beneficiary in a Will

Rights and Limitations of Will Beneficiaries

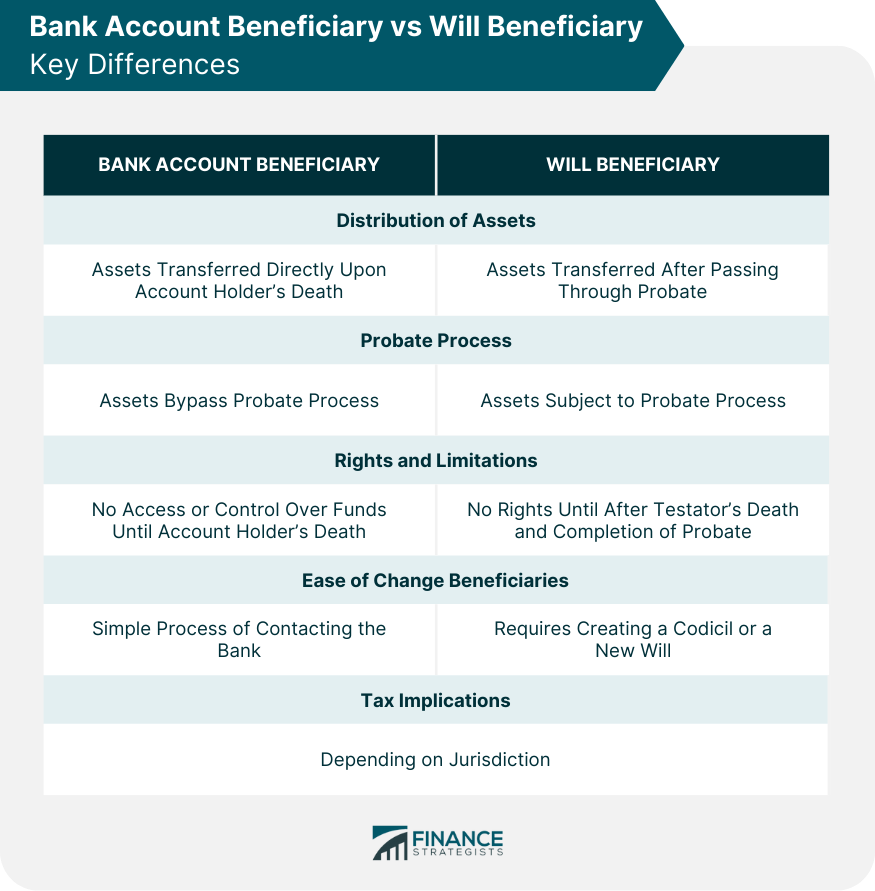

Bank Account Beneficiary vs Will Beneficiary: Key Differences

Distribution of Assets

Probate Process

Rights and Limitations

Ease of Change Beneficiaries

Tax Implications

Legal and Financial Implications of Beneficiary Designations

Estate and Inheritance Tax

Legal Disputes and Court Cases

Financial Planning and Wealth Management Considerations

Tips and Best Practices: Setting up Bank Accounts and Will Beneficiaries

Regularly Review and Update Beneficiaries

Choose Multiple Beneficiaries

Communicate With Beneficiaries

Conclusion

Bank Account Beneficiary vs Will Beneficiary FAQs

The main difference lies in how and when assets are distributed. A bank account beneficiary inherits the assets directly upon the account holder's death, bypassing probate. In contrast, a will beneficiary inherits the assets specified in a will, but only after the will has gone through probate, which can be a time-consuming process.

Yes, they can be different. However, in the case of a bank account, the beneficiary specified directly with the bank will generally supersede the will. This is why it's crucial to keep all beneficiary designations current and consistent across all platforms.

Assets left to a bank account beneficiary bypass the probate process entirely. This means the assets can be transferred almost immediately after the account holder's death. On the other hand, assets left to a will beneficiary have to go through probate, which can take months or even years to complete.

Changing a bank account beneficiary usually requires contacting your bank and updating the beneficiary's details. On the other hand, changing a will beneficiary often involves creating a new will or adding a codicil to an existing will. In both cases, it's advisable to consult with a legal or financial advisor.

There can be. Depending on the jurisdiction and the value of the inherited assets, there may be estate or inheritance taxes that apply. The tax situation can vary significantly, so beneficiaries should consult with a tax advisor or attorney to understand any potential tax liabilities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.