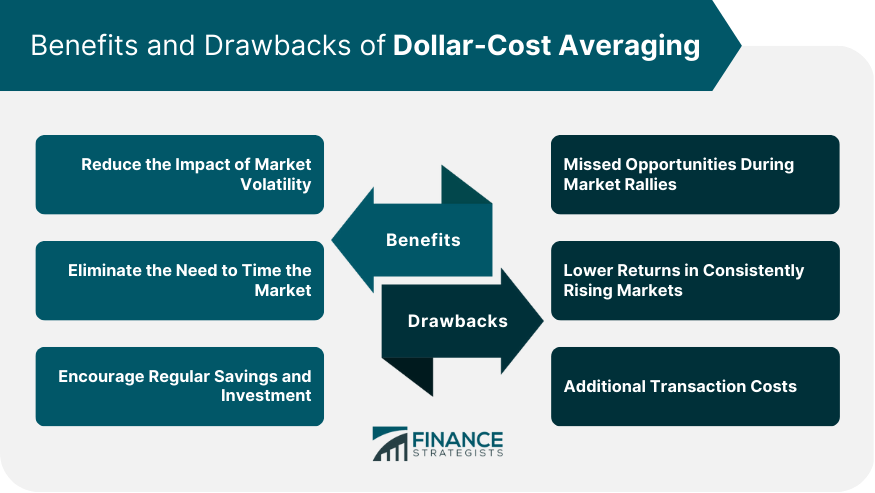

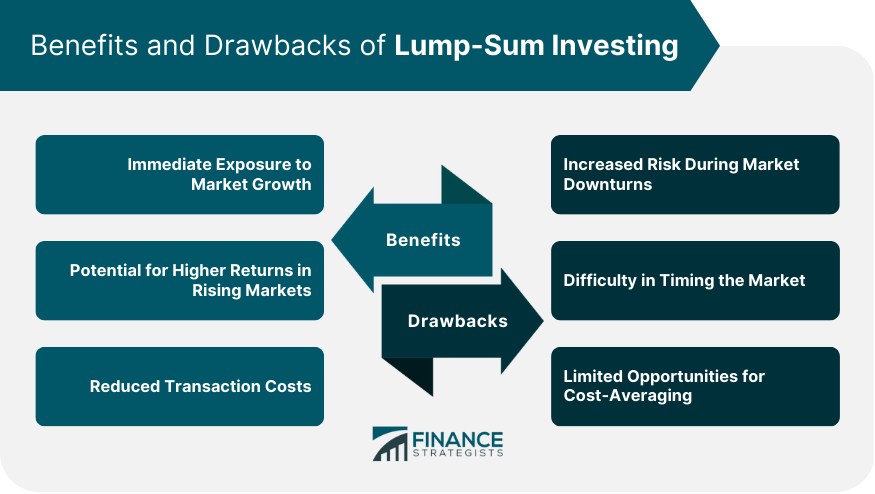

Dollar-cost averaging is an investment strategy where an investor allocates a fixed amount of money to invest in a particular asset at regular intervals, regardless of the asset's price. This approach helps reduce the impact of market fluctuations and eliminates the need to time the market. Lump-sum investing is an investment strategy where an investor invests a large sum of money in a particular asset or portfolio all at once. This approach seeks to take advantage of immediate exposure to market growth and the potential for higher returns in rising markets. Both dollar-cost averaging and lump-sum investing are viable investment strategies with distinct advantages and disadvantages. The choice between the two depends on factors such as an investor's risk tolerance, investment time horizon, market conditions, and available funds. Dollar-cost averaging is an investment strategy that involves investing a fixed amount of money into an asset at regular intervals, regardless of the market conditions. This means an investor would invest the same amount of money at fixed intervals, such as monthly or quarterly, regardless of whether the market is up or down. For example, if an investor decides to invest $500 in a particular stock every month for a year, they would invest $500 every month regardless of whether the stock price went up or down during that period. By doing this, the investor is able to buy more shares when the price is low and fewer shares when the price is high. Over time, this can help to reduce the impact of market fluctuations on the overall investment performance. Dollar-cost averaging is often used as a way to reduce the risk of investing in volatile markets. It can also help to reduce the emotional impact of investing, as investors are less likely to make impulsive decisions based on short-term market movements. However, it is important to note that dollar-cost averaging does not guarantee a profit or protect against losses, and investors should always do their own research and seek professional advice before investing. By spreading investments over time, dollar-cost averaging helps reduce the impact of market volatility on the investor's portfolio. This approach mitigates the risk of investing a large sum of money at an inopportune time when the market is at a peak. Dollar-cost averaging removes the pressure of timing the market, as investments are made consistently over time. This strategy allows investors to focus on their long-term investment goals rather than attempting to predict short-term market movements. Dollar-cost averaging promotes a disciplined approach to investing, as it requires regular contributions to the investment plan. This strategy helps investors build wealth over time by consistently adding to their investments, regardless of market conditions. One disadvantage of dollar-cost averaging is the potential to miss out on significant gains during market rallies. By investing gradually, investors may not be fully invested when the market experiences a sustained period of growth. In consistently rising markets, dollar-cost averaging may result in lower returns compared to lump-sum investing, as the investor is not fully exposed to market growth from the beginning. Dollar-cost averaging can lead to higher transaction costs due to increased trades. These costs can erode returns, particularly for small investors or those with high trading fees. Lump-sum investing is an investment strategy in which an investor invests a large sum of money all at once rather than investing smaller amounts of money over a period of time. Unlike dollar-cost averaging, which involves investing a fixed amount of money at regular intervals, lump-sum investing involves investing a significant amount of money in a single transaction. For example, if an investor has $50,000 to invest, they might choose to invest the entire amount in a single stock or mutual fund. This approach can be particularly beneficial if the investor expects the investment to generate significant returns in a short period of time. Additionally, lump-sum investing can help to reduce transaction costs, as the investor only needs to make a single investment rather than multiple investments over time. However, lump-sum investing can also be risky, particularly if the investor invests in a volatile asset or in a market that experiences significant fluctuations. If the investment performs poorly, the investor may lose a significant amount of money in a short period of time. For this reason, many investors prefer to use dollar-cost averaging to reduce their risk and take advantage of market fluctuations over time. Ultimately, the decision to use lump-sum investing or dollar-cost averaging will depend on an investor's risk tolerance, investment goals, and market conditions. Lump-sum investing allows investors to gain immediate exposure to market growth, potentially benefiting from any subsequent increases in asset prices. In a rising market, lump-sum investing has the potential to generate higher returns than dollar-cost averaging, as the investor is fully invested from the outset. By investing a large sum of money all at once, lump-sum investing can result in lower transaction costs compared to dollar-cost averaging. This approach may be more cost-effective for investors with limited funds or high trading fees. Lump-sum investing can expose investors to increased risk during market downturns, as the entire investment is subject to market fluctuations. If the investment is made just before a significant market decline, the investor may experience substantial losses. Investing a large sum of money all at once can be challenging, as it requires accurately predicting the best time to enter the market. Most investors find it difficult to time the market consistently, potentially leading to suboptimal investment decisions. Lump-sum investing does not provide cost-averaging benefits, as the investment is made all at once. This approach makes the investor more vulnerable to short-term market fluctuations and may result in a less diversified portfolio over time. Value averaging is a variation of dollar-cost averaging that adjusts the investment amount based on the performance of the asset. This approach seeks to maintain a predetermined growth rate for the investment, resulting in larger contributions during periods of underperformance and smaller contributions during periods of outperformance. Systematic withdrawal plans involve regularly withdrawing a fixed amount or percentage from an investment portfolio, providing a steady income stream for the investor. This strategy can be used in conjunction with either dollar-cost averaging or lump-sum investing to help manage cash flow needs during retirement. An investor's time horizon plays a crucial role in deciding between dollar-cost averaging and lump-sum investing. Long-term investors may be more inclined to use dollar-cost averaging, as it helps mitigate the impact of short-term market fluctuations. Short-term investors might prefer lump-sum investing to capitalize on immediate market opportunities. Risk tolerance should be considered when choosing between dollar-cost averaging and lump-sum investing. Investors with a lower risk tolerance may prefer dollar-cost averaging, as it spreads investment risk over time. Those with a higher risk tolerance might choose lump-sum investing to maximize potential returns during favorable market conditions. The current market conditions and outlook should influence an investor's decision between dollar-cost averaging and lump-sum investing. When markets are uncertain or volatile, dollar-cost averaging can provide a more conservative approach. In contrast, lump-sum investing may be more suitable during market stability and growth periods. The availability of funds is another factor to consider when choosing between dollar-cost averaging and lump-sum investing. Investors with limited funds may find dollar-cost averaging more accessible, as it allows for smaller, regular investments. Those with a significant sum available for investment might prefer lump-sum investing to capitalize on immediate market exposure. A hybrid investment approach combines elements of both dollar-cost averaging and lump-sum investing strategies. This approach can provide a balanced investment plan that adapts to varying market conditions and investor preferences. Combining dollar-cost averaging and lump-sum investing strategies can offer the benefits of both approaches. Investors can reduce market timing risks, enjoy immediate market exposure, and adapt to changing market conditions and personal financial goals. To implement a combined strategy, investors can allocate a portion of their investment to lump-sum investing, providing immediate market exposure. The remaining funds can be invested using a dollar-cost averaging approach, allowing regular investments over time and reducing market timing risks. Understanding the differences between dollar-cost averaging and lump-sum investing is crucial for informed decision-making. Each strategy has unique benefits and drawbacks, which should be considered based on individual investment goals and market conditions. When choosing an investment strategy, investors should consider factors such as investment time horizon, risk tolerance, market conditions, and availability of funds. These factors will help determine which strategy aligns best with an investor's goals and preferences. Both dollar-cost averaging and lump-sum investing offer potential benefits and drawbacks. Weighing these factors can help investors make informed decisions about which strategy to pursue based on their unique circumstances. A hybrid approach combining dollar-cost averaging and lump-sum investing elements may provide a balanced investment plan. This approach can help investors adapt to changing market conditions and personal financial goals while capitalizing on the benefits of each strategy. Understanding the differences between dollar-cost averaging and lump-sum investing is essential to make informed investment decisions. However, navigating the complexities of these strategies can be challenging for individual investors. Seeking the guidance of professional wealth management services can help you determine the most suitable investment approach based on your unique financial goals and risk tolerance. A wealth management professional can provide personalized advice, tailor investment strategies, and help you create a well-balanced portfolio to optimize returns and minimize risks. Reach out to a trusted wealth management advisor today to take control of your financial future.Dollar-Cost Averaging vs Lump-Sum Investing: Overview

What Is Dollar-Cost Averaging?

Benefits of Dollar-Cost Averaging

Reduce the Impact of Market Volatility

Eliminate the Need to Time the Market

Encourage Regular Savings and Investment

Drawbacks of Dollar-Cost Averaging

Missed Opportunities During Market Rallies

Lower Returns in Consistently Rising Markets

Additional Transaction Costs

What Is Lump-Sum Investing?

Benefits of Lump-Sum Investing

Immediate Exposure to Market Growth

Potential for Higher Returns in Rising Markets

Reduced Transaction Costs

Drawbacks of Lump-Sum Investing

Increased Risk During Market Downturns

Difficulty in Timing the Market

Limited Opportunities for Cost-Averaging

Variations of Dollar-Cost Averaging and Lump-Sum Investing

Value Averaging

Systematic Withdrawal Plans

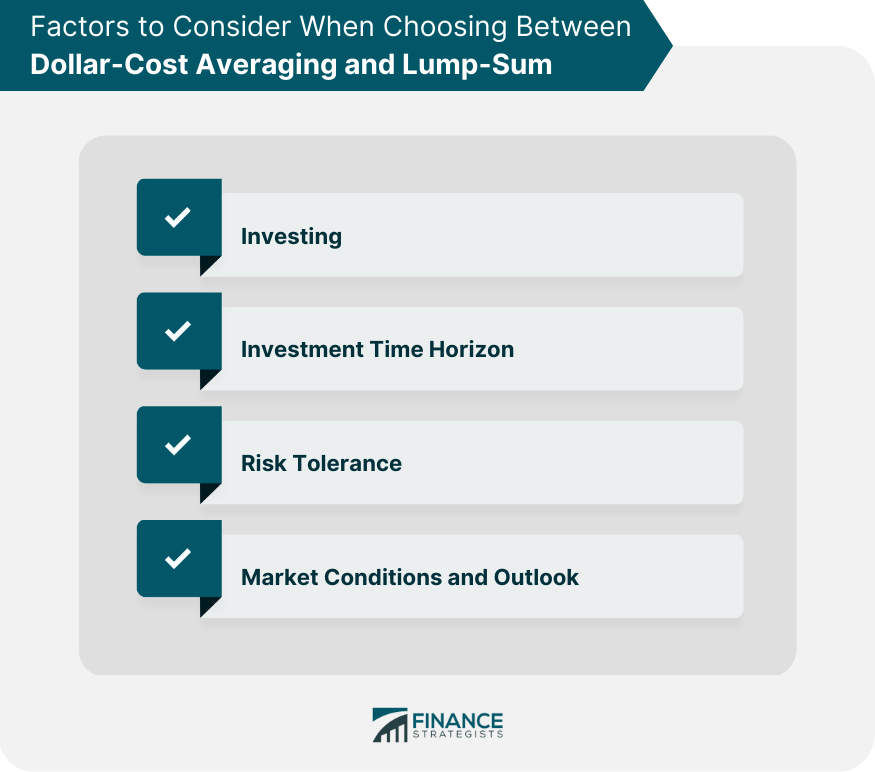

Factors to Consider When Choosing Between Dollar-Cost Averaging and Lump-Sum Investing

Investment Time Horizon

Risk Tolerance

Market Conditions and Outlook

Availability of Funds

Combining Dollar-Cost Averaging and Lump-Sum Investing Strategies

Hybrid Investment Approach

Benefits of Combining the Strategies

Implementing a Combined Strategy

Final Thoughts

Dollar-Cost Averaging vs Lump-Sum Investing FAQs

Dollar-cost averaging is an investment strategy that involves investing a fixed amount of money into an asset at regular intervals, regardless of the market conditions.

Lump-sum investing is an investment strategy in which an investor invests a large sum of money all at once rather than investing smaller amounts of money over a period of time.

Dollar-cost averaging can reduce the impact of market volatility, eliminate the need to time the market, and encourage regular savings and investment.

Lump-sum investing can expose investors to increased risk during market downturns, be challenging to time the market, and limited opportunities for cost-averaging.

Yes, a hybrid investment approach can combine elements of both strategies to provide a balanced investment plan that adapts to varying market conditions and investor preferences.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.