Perpetual bonds, also known as perpetual securities or perpetuities, are a type of long-term debt instrument that has no fixed maturity date. These bonds do not have a specific redemption date, and the issuer is not obligated to repay the principal amount to the bondholders. Instead, perpetual bonds pay periodic coupon or interest payments indefinitely. The interest payments are typically fixed and may have a reset provision to adjust the coupon rate periodically. While perpetual bonds provide a stable source of income for investors, they also carry risks such as interest rate changes and creditworthiness of the issuer. Issuers of perpetual bonds are often corporations, governments, or financial institutions seeking long-term financing options. The primary characteristic of perpetual bonds is the lack of a maturity date. This means that the issuer is not required to repay the principal amount, allowing the bond to generate interest payments indefinitely. Perpetual bonds can have either fixed or variable interest rates. Fixed-rate bonds pay a constant interest rate throughout their existence, while variable-rate bonds adjust their interest rates periodically based on market conditions or a reference rate. Issuers can offer perpetual bonds with a call option, giving them the right to redeem the bond at a specific date or after a predetermined period. This allows the issuer to refinance the bond at a lower interest rate if market conditions are favorable. Non-callable perpetual bonds, on the other hand, do not have this feature. Perpetual bonds can vary in their subordination and ranking in the issuer's capital structure. Some bonds are senior, meaning they have priority over other types of debt, while others are subordinated, ranking lower in the event of a default or bankruptcy. Perpetual bonds are considered hybrid securities because they possess characteristics of both debt and equity. While they pay regular interest, similar to traditional bonds, they have no maturity date, making them more similar to stocks in terms of their duration. Governments can issue perpetual bonds to finance long-term projects or manage public debt. Historically, these bonds have been used to fund wars, infrastructure projects, and other public initiatives. Corporations may issue perpetual bonds to raise capital for various purposes, such as expanding operations or refinancing existing debt. These bonds are typically riskier than government-issued perpetual bonds due to the potential for default. Perpetual preferred stock is a type of equity security that pays dividends indefinitely, similar to perpetual bonds. Holders of preferred stock have priority over common shareholders in the event of bankruptcy or liquidation. Perpetual subordinated debt is a type of bond that ranks lower in priority compared to other debt securities issued by the same entity. This means that, in the event of default, holders of perpetual subordinated debt will be paid after holders of senior debt. Investing in perpetual bonds provides investors with a consistent and potentially lifelong income stream. This makes them an attractive option for those seeking regular cash flow, such as retirees or income-focused investors. Perpetual bonds often offer higher yields compared to other fixed-income securities with similar credit ratings. This is because the lack of a maturity date and the hybrid nature of these bonds increase their risk profile. Including perpetual bonds in an investment portfolio can help to diversify holdings, reducing overall risk. These bonds can provide exposure to different sectors, credit qualities, and interest rate environments, helping to balance the portfolio. In some countries, interest payments from perpetual bonds may be taxed more favorably than other forms of investment income, offering additional incentives for investors. Perpetual bonds with variable interest rates can provide an effective hedge against inflation. As interest rates rise, the bond's coupon payments increase, helping to maintain the investor's purchasing power. Like all fixed-income securities, perpetual bonds are subject to interest rate risk. As interest rates rise, the price of existing bonds tends to fall, leading to capital losses for investors who sell their bonds before the issuer redeems them. Investors in perpetual bonds are exposed to credit risk, as the issuer may default on interest payments or principal repayment in the case of callable bonds. This risk is particularly relevant for corporate perpetual bonds, which generally carry a higher risk of default compared to government-issued bonds. Perpetual bonds may be less liquid than other fixed-income securities, making it more challenging for investors to buy or sell them in the secondary market. This can result in wider bid-ask spreads and increased price volatility. Callable perpetual bonds carry the risk that the issuer will redeem the bond when interest rates fall, forcing investors to reinvest their capital at lower rates. This can lead to a reduction in income and potential capital losses. Due to their indefinite duration, perpetual bonds offer limited potential for capital appreciation compared to other fixed-income securities with set maturity dates. Investors should carefully consider the credit rating of the issuer when evaluating perpetual bonds. A higher credit rating generally indicates a lower risk of default, which is essential for maintaining a stable income stream. Comparing the yield of perpetual bonds to other fixed-income securities with similar credit ratings can help investors determine if the potential return is worth the increased risk associated with the bond's indefinite duration. The coupon rate and payment frequency of perpetual bonds can impact their overall attractiveness. Investors should consider how these factors align with their income needs and investment objectives. For callable perpetual bonds, it is crucial to understand the call features, including the call date and any restrictions on the issuer's ability to redeem the bond. This information can help investors gauge the potential call risk associated with the investment. Investors should consider the current interest rate environment when evaluating perpetual bonds. In a rising interest rate environment, the value of existing perpetual bonds may decline, while falling interest rates may increase the likelihood of callable bonds being redeemed. Including perpetual bonds in an investment portfolio can help achieve diversification across asset classes, sectors, and credit qualities. This can contribute to a more balanced risk profile and potentially improve overall portfolio performance. Perpetual bonds can provide a consistent income stream, making them suitable for investors who rely on regular cash flow, such as retirees. By allocating a portion of their portfolio to perpetual bonds, investors can help meet their income needs without sacrificing diversification. Investors with a long-term investment horizon may find perpetual bonds particularly attractive due to their indefinite duration and potential for higher yields compared to other fixed-income securities. Understanding and actively managing the various risks associated with perpetual bonds is critical for incorporating them into a wealth management strategy. Investors should closely monitor interest rate movements, credit quality, and liquidity to manage their exposure to these risks. Investors should consider the potential tax benefits associated with perpetual bonds in their jurisdiction. In some cases, interest payments may be taxed more favorably than other forms of investment income, offering additional incentives for investors to include perpetual bonds in their wealth management strategies. Perpetual bonds offer unique features and considerations for investors. They lack a maturity date but provide a steady income stream through periodic coupon payments. Investors should assess the credit rating of the issuer, comparing it to similar securities, to evaluate default risk and potential returns. The coupon rate and payment frequency should align with investors' income needs and objectives. Call features, such as call dates and redemption restrictions, should be understood to gauge call risk. The current interest rate environment impacts the value of perpetual bonds, with rising rates potentially decreasing their value and falling rates increasing call risk. When incorporating perpetual bonds into wealth management strategies, diversification, income generation, long-term investment horizons, risk management, and tax planning should be considered.Definition of Perpetual Bonds

Features of Perpetual Bonds

No Maturity Date

Fixed or Variable Interest Rates

Callable and Non-callable Options

Subordination and Ranking

Hybrid Nature

Types of Perpetual Bonds

Government-Issued Perpetual Bonds

Corporate Perpetual Bonds

Perpetual Preferred Stock

Perpetual Subordinated Debt

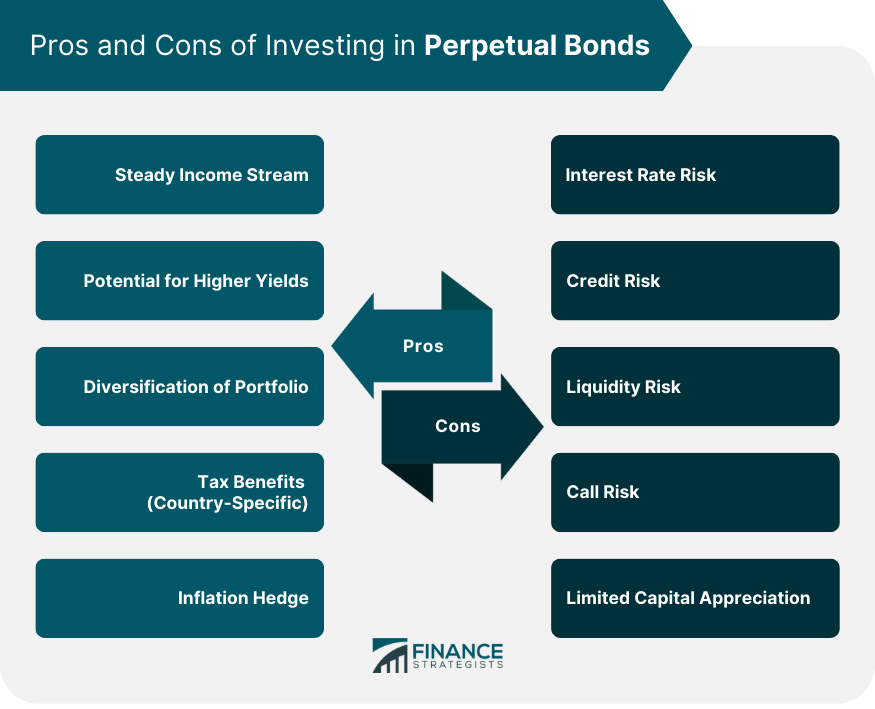

Pros Investing in Perpetual Bonds

Steady Income Stream

Potential for Higher Yields

Diversification of Portfolio

Tax Benefits (Country-Specific)

Inflation Hedge

Cons of Perpetual Bonds

Interest Rate Risk

Credit Risk

Liquidity Risk

Call Risk

Limited Capital Appreciation

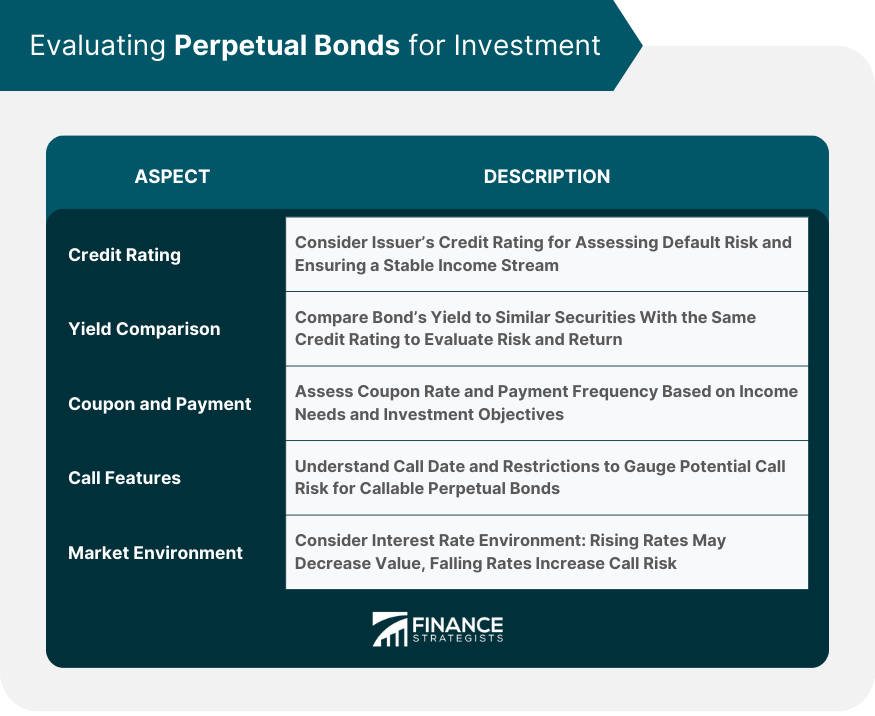

Evaluating Perpetual Bonds for Investment

Credit Rating Assessment

Yield Comparison

Coupon and Payment Frequency

Call Features

Market Environment

Incorporating Perpetual Bonds in Wealth Management Strategies

Portfolio Diversification

Income Generation

Long-Term Investment Horizon

Risk Management

Tax Planning

Conclusion

Perpetual Bonds FAQs

A Perpetual Bond is a type of fixed-income security with no set maturity date, which pays interest to the bondholder indefinitely. Unlike traditional bonds, which have a defined maturity date when the principal is repaid, perpetual bonds continue to generate interest payments for the bondholder without an obligation for the issuer to repay the principal.

Investing in Perpetual Bonds can contribute to wealth management by providing a steady income stream, the potential for higher yields, and diversification benefits. These bonds can help balance an investment portfolio, reduce overall risk, and generate consistent cash flow, making them attractive for income-focused investors and those seeking long-term investments.

The main risks associated with investing in Perpetual Bonds include interest rate risk, credit risk, liquidity risk, call risk, and limited capital appreciation. These risks stem from the bond's indefinite duration, the credit quality of the issuer, market conditions, and call features in the case of callable bonds.

Investors can evaluate Perpetual Bonds by assessing the credit rating of the issuer, comparing the bond's yield to other fixed-income securities with similar credit ratings, understanding the coupon rate and payment frequency, analyzing the call features of callable bonds, and considering the current interest rate environment.

Future trends and developments, such as changes in the interest rate environment, potential market growth, regulatory changes, and innovations in perpetual bond structures, can significantly impact the Perpetual Bond market. These factors can influence the attractiveness, demand, and pricing of perpetual bonds, making it crucial for investors to stay informed and adapt their investment strategies accordingly.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.