Participant-Level Fee Disclosures are regulatory requirements aimed at promoting transparency in the fees and expenses charged to participants in employer-sponsored retirement plans such as 401(k), 403(b), and similar defined contribution plans. These disclosures are governed by the Employee Retirement Income Security Act (ERISA) and the U.S. Department of Labor (DOL) regulations, primarily Section 404(a)(5) of ERISA. The purpose of these disclosures is to help plan participants make informed decisions about their investment options and better understand the costs associated with their retirement savings. Expense ratios represent the percentage of a mutual fund's or exchange-traded fund's (ETF) assets used for operational expenses. These fees are automatically deducted from the fund's returns, affecting the overall investment performance. Sales charges, also known as loads, are fees paid by investors when purchasing or selling shares of mutual funds. These fees compensate brokers, financial advisors, or other intermediaries for their services. Management fees are charged by the investment management company to cover the costs of managing the fund, including investment research, portfolio management, and trading expenses. Recordkeeping fees cover the cost of maintaining participant account records, processing transactions, and providing customer service. Custodial fees are charged by the financial institution holding the plan's assets to cover the costs of safeguarding the investments and executing transactions. Third-party administration (TPA) fees are paid to service providers who help manage the plan's day-to-day operations, such as compliance testing and government reporting. Loan processing fees are charged when participants take loans from their retirement plan accounts. These fees cover the administrative costs associated with processing and maintaining the loan. Distribution fees are charged when participants withdraw money from their retirement plan accounts, either as a lump sum or through periodic payments. Qualified Domestic Relations Order (QDRO) processing fees are incurred when retirement plan assets are divided as part of a divorce settlement. The ERISA Section 404(a)(5) establishes the requirement for plan fiduciaries to provide participant-level fee disclosures to help participants make informed decisions about their investments. This regulation sets forth the specific requirements for participant-level fee disclosures, including the type and format of information that must be provided to participants. Investment advisers must provide clients with a Form ADV, which includes information about the adviser's fees, services, and potential conflicts of interest. Reg BI requires broker-dealers to act in the best interest of their clients when recommending investment products or strategies, including disclosing material fees and costs. Plan fiduciaries must act solely in the interest of plan participants, including providing transparent fee information. Plan fiduciaries must exercise care and diligence when selecting and monitoring plan investments, as well as ensuring that fees are reasonable. Fees should be clearly presented in a manner that is easily understood by plan participants, avoiding jargon or complex terminology. All fees, including those that may not be readily apparent, should be disclosed to plan participants to ensure full transparency. Regular updates on fee disclosures should be provided to participants, ideally on an annual basis or whenever significant changes occur. Fee disclosures should be made available in various formats, such as print, online, and through mobile apps, to cater to the diverse preferences of plan participants. Plan sponsors and service providers should offer resources and educational materials to help participants better understand fee structures and their impact on investment outcomes. Tools and resources should be made available to assist participants in comparing fees across different investment options and providers. Transparent fee disclosures enable participants to make well-informed decisions about their investments and retirement planning strategies. Greater fee transparency can lead to increased fee awareness among participants, encouraging them to take a more active role in managing their retirement plan accounts. Transparent fee disclosures can result in increased competition among service providers, potentially driving down fees and improving overall investment performance for participants. Fee structures can be complex and difficult to understand, posing challenges for participants when evaluating their investment options. Fee disclosures can vary significantly across different providers and investment products, making it difficult for participants to make accurate comparisons. Ensuring transparency in fee disclosures while avoiding information overload is an ongoing challenge, as excessive detail can overwhelm participants and hinder effective decision-making. Participant-Level Fee Disclosures play a vital role in fostering transparency and informed decision-making within the retirement plan industry. These disclosures encompass various types of fees, including investment-related fees, plan administration fees, and individual service fees. The regulatory framework, governed by the DOL and the SEC, sets the standards for fee disclosures and fiduciary responsibilities. Implementing best practices in fee disclosure communication, such as ensuring transparency, using multiple formats, and providing educational resources, can enhance participant outcomes. Challenges like complex fee structures, inconsistencies across providers, and information overload persist; continuous improvement and standardization in fee disclosure practices remain crucial for promoting transparency and supporting better retirement planning decisions for participants.Definition of Participant-Level Fee Disclosures

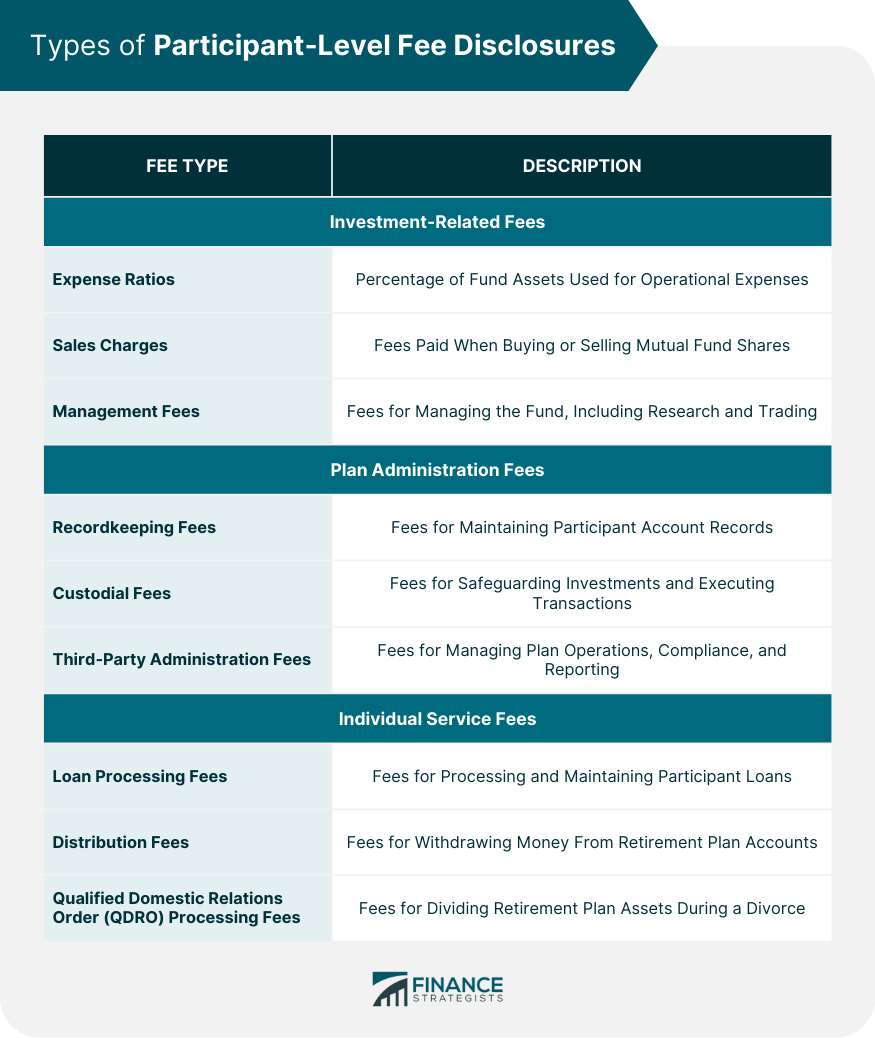

Types of Participant-Level Fee Disclosures

Investment-Related Fees

Expense Ratios

Sales Charges

Management Fees

Plan Administration Fees

Recordkeeping Fees

Custodial Fees

Third-Party Administration Fees

Individual Service Fees

Loan Processing Fees

Distribution Fees

QDRO Processing Fees

Regulatory Framework

Department of Labor (DOL) Regulations

ERISA Section 404(a)(5)

29 CFR 2550.404a-5

Securities and Exchange Commission (SEC) Regulations

Form ADV Requirements

Regulation Best Interest (Reg BI)

Fiduciary Responsibilities

Duty of Loyalty

Duty of Prudence

Fee Disclosure Best Practices

Transparency

Clear Presentation of Fees

Avoiding Hidden Fees

Communication

Frequency of Fee Disclosure Updates

Use of Multiple Formats

Education

Helping Participants Understand Fee Structures

Providing Resources for Fee Comparison

Impact of Fee Disclosures on Participant Outcomes

Informed Decision-Making

Increased Fee Awareness

Potential for Lower Fees and Improved Investment Performance

Challenges and Controversies

Complexity of Fee Structures

Inconsistencies in Fee Disclosures Across Providers

Balancing the Need for Transparency With Information Overload

Conclusion

Participant-Level Fee Disclosures FAQs

Participant-Level Fee Disclosures are documents that provide essential information about the fees and expenses associated with retirement plans. They are crucial for ensuring transparency, enabling plan participants to make informed decisions about their investments, and promoting a competitive environment that can lead to lower fees and better investment performance.

Participant-Level Fee Disclosures generally include investment-related fees (such as expense ratios, sales charges, and management fees), plan administration fees (such as recordkeeping, custodial, and third-party administration fees), and individual service fees (such as loan processing, distribution, and QDRO processing fees).

The Department of Labor (DOL) and the Securities and Exchange Commission (SEC) have established regulations that govern Participant-Level Fee Disclosures. Key regulations include ERISA Section 404(a)(5) and 29 CFR 2550.404a-5 from the DOL, as well as Form ADV requirements and Regulation Best Interest (Reg BI) from the SEC.

Best practices for communicating Participant-Level Fee Disclosures include ensuring transparency through a clear presentation of fees and avoiding hidden fees, providing regular updates on fee disclosures, using multiple formats (e.g., print, online) to cater to diverse preferences, and offering educational resources to help participants understand fee structures and compare fees across different investment options and providers.

Participant-Level Fee Disclosures can positively impact participant outcomes by enabling informed decision-making, increasing fee awareness, and fostering a competitive environment that may result in lower fees and improved investment performance. However, challenges such as complex fee structures, inconsistencies in disclosures across providers, and information overload can hinder the effectiveness of these disclosures.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.