Seller financing, also known as owner financing or vendor financing, is a transaction in which the seller of a property acts as the lender by providing a loan to the buyer, who then repays the loan through regular installment payments. The buyer takes possession of the property and assumes ownership, while the seller retains a security interest in the property until the loan is fully repaid. The seller should clearly understand the property's current market value. This can be achieved through a professional appraisal, a comparative market analysis, or by consulting with a real estate agent. Before agreeing to seller financing, the seller should assess the buyer's creditworthiness by reviewing their credit history, employment status, and financial stability. The loan amount is the total amount the seller is financing for the buyer. It is typically determined by subtracting the buyer's down payment from the purchase price. The interest rate is the percentage of the loan amount the buyer will pay as interest on an annual basis. The rate should be competitive with current market rates. The loan term is the length of time the buyer has to repay the loan. Typical terms range from 15 to 30 years, but can be negotiated between the parties. The down payment is the amount the buyer will pay upfront toward the purchase price. A higher down payment reduces the loan amount and provides the seller with additional security. The payment schedule outlines the frequency and amount of the buyer's loan payments, including principal and interest. The promissory note is a legal document that outlines the terms of the loan and the buyer's promise to repay the debt. It includes the principal amount, interest rate, payment schedule, and any other relevant terms. A mortgage or deed of trust is a legal document that secures the promissory note by granting the seller a security interest in the property. This document provides the seller with the right to foreclose on the property if the buyer defaults on the loan. The purchase agreement is a legally binding contract between the buyer and seller that outlines the terms and conditions of the property sale, including the purchase price, closing date, and any contingencies. Depending on the jurisdiction and specific circumstances, additional documents, such as property disclosures, inspection reports, and title insurance, may be necessary. Both parties must sign the promissory note, mortgage or deed of trust, purchase agreement, and any other necessary documents to finalize the transaction. The seller must record the mortgage or deed of trust with the appropriate local government office to establish their security interest in the property. Once all documents are executed and recorded, the property ownership is transferred to the buyer, and the transaction is considered closed. Faster Sale: Seller financing may attract more potential buyers, leading to a quicker sale. Higher Sales Price: Sellers may be able to negotiate a higher sales price in exchange for providing financing. Interest Income: The seller earns interest on the loan, providing an additional source of income. Tax Benefits: Spreading out the capital gains from the sale over multiple years can result in favorable tax treatment. Easier Financing: Buyers who may have difficulty obtaining traditional financing can benefit from seller financing. Faster Closing: The process is often quicker than obtaining a traditional mortgage. Flexible Terms: The buyer and seller can negotiate loan terms tailored to their specific needs. The primary risk for the seller is the possibility of the buyer defaulting on the loan, which may require the seller to foreclose on the property and potentially incur additional expenses. If the property's value declines or the buyer damages the property, the seller may lose part or all of their collateral. Seller financing may result in complex legal and tax issues. Sellers should consult with legal and financial professionals to ensure compliance with all applicable laws and regulations. Sellers acting as lenders must be prepared for the ongoing responsibilities and time commitment associated with managing the loan. Buyers may face higher interest rates in seller financing arrangements compared to traditional mortgages, increasing their overall cost of borrowing. Sellers may require a larger down payment as a form of security, which can be challenging for some buyers. Some seller financing agreements include balloon payments, where the buyer must make a large lump-sum payment at the end of the loan term, potentially creating financial strain. Buyers must ensure that the seller has the financial capacity to provide financing and that the seller's existing mortgage, if any, allows for seller financing. Both buyers and sellers should seek professional advice from attorneys, financial advisors, and real estate professionals to ensure a smooth and legally compliant transaction. It is important for both parties to carefully review all financial documents, including credit reports, tax returns, and bank statements. Both parties should arrange for a thorough property inspection and appraisal to confirm the property's condition and value. A title search should be conducted to ensure the property is free of liens or encumbrances, and title insurance should be obtained to protect against potential title defects. In a tight credit market, it can be difficult for potential buyers to obtain financing through traditional banks, making seller financing an attractive alternative. Unique or unconventional properties may not meet traditional lenders' requirements, making seller financing a more viable option. Buyers with limited or poor credit history may need help to secure a mortgage, but may still be able to obtain financing through a seller-financed arrangement. Buyers with strong credit and financial stability may be able to obtain a mortgage from a traditional bank or credit union. Federally backed loan programs, such as FHA, VA, and USDA loans, can provide more flexible lending requirements and lower down payment options for eligible borrowers. A lease-option agreement allows the buyer to lease the property with the option to purchase it at a predetermined price within a specified time frame. A lease-purchase agreement is similar to a lease-option agreement, but the buyer is obligated to purchase the property at the end of the lease term. Individual investors or private lending companies provide private money loans and can offer more flexible lending terms compared to traditional banks. Hard money loans are short-term, asset-based loans provided by private lenders that can be a viable option for buyers who need quick financing or have difficulty obtaining traditional loans. Seller financing can be a valuable tool for facilitating homeownership and property sales in situations where traditional financing may not be available. By understanding the process, risks, and considerations involved and exploring alternative financing options, buyers and sellers can make informed decisions and potentially benefit from a successful seller financing arrangement.What Is Seller Financing?

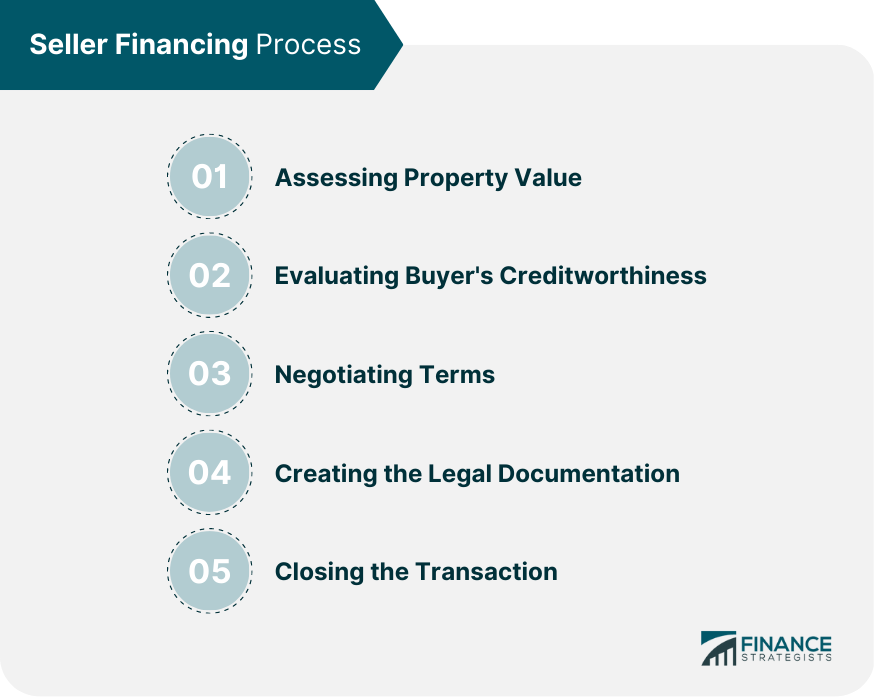

Seller Financing Process

Assessing Property Value

Evaluating Buyer's Creditworthiness

Negotiating Terms

Loan Amount

Interest Rate

Loan Term

Down Payment

Payment Schedule

Creating the Legal Documentation

Promissory Note

Mortgage or Deed of Trust

Purchase Agreement

Other Relevant Documents

Closing the Transaction

Execution of Legal Documents

Recording the Mortgage or Deed of Trust

Transfer of Property Ownership

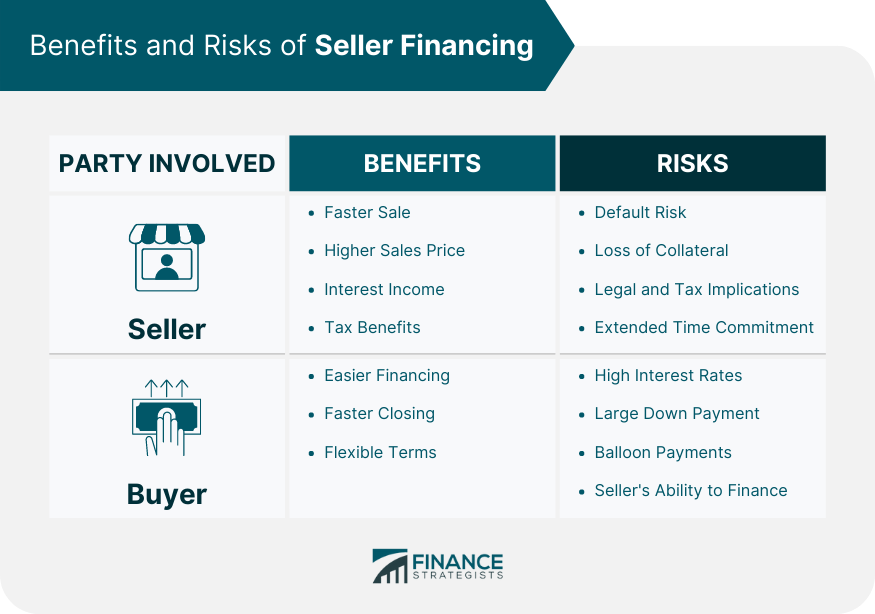

Benefits of Seller Financing

Benefits to the Seller

Benefits to the Buyer

Risks and Considerations of Seller Financing

Risks for the Seller

Default Risk

Loss of Collateral

Legal and Tax Implications

Extended Time Commitment

Risks for the Buyer

High Interest Rates

Large Down Payment

Balloon Payments

Seller's Ability to Finance

Due Diligence for Both Parties

Professional Advice

Reviewing Financial Documents

Property Inspection and Appraisal

Title Search and Insurance

Situations Where Seller Financing is Advantageous

Tight Credit Market

Unique Property

Buyer With Limited Credit History

Alternatives to Seller Financing

Traditional Bank Loans

FHA, VA, and USDA Loans

Lease-Option Agreements

Lease-Purchase Agreements

Private Money Loans

Hard Money Loans

Conclusion

Seller Financing FAQs

Seller financing, also known as owner financing, is a transaction in which the seller of a property provides financing to the buyer instead of the buyer obtaining a mortgage loan from a third-party lender.

In seller financing, the buyer makes a down payment to the seller and signs a promissory note to repay the remaining balance, with interest, over a specified period. The seller retains a lien on the property until the buyer fully repays the loan.

Seller financing can benefit both the buyer and the seller. Buyers who may not qualify for traditional financing can purchase a property with flexible terms. At the same time, sellers can sell their property quickly and earn a steady stream of income from the interest on the loan.

Yes, there are risks involved in seller financing. The buyer may default on the loan, which could result in a lengthy and costly legal process to regain ownership of the property. Additionally, the seller may have to foreclose on the property if the buyer fails to make payments, which can be complicated.

Seller financing is not as common as traditional financing methods but is becoming more popular in certain situations. It is often used in real estate transactions when the buyer is unable to obtain financing through a bank or other lender.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.