Mortgage planning is the process of evaluating and choosing the best mortgage options based on an individual's financial situation and goals. It plays a crucial role in personal finance, as buying a home is often the largest investment most people make. By understanding the different types of mortgages and their implications, homeowners can make informed decisions that lead to long-term financial stability. A fixed-rate mortgage has an interest rate that remains constant throughout the loan term. This type of mortgage provides stability in monthly payments, making it easier for homeowners to budget and plan. An adjustable-rate mortgage (ARM) has an interest rate that changes periodically based on market conditions. This type of mortgage often has lower initial interest rates, but may increase over time, affecting monthly payments. In an interest-only mortgage, borrowers pay only the interest on the loan for a specified period, usually 5-10 years. After the interest-only period ends, the monthly payments increase significantly to cover both principal and interest. A balloon mortgage requires borrowers to make small monthly payments for a set period, followed by a large lump sum payment to pay off the remaining loan balance. This type of mortgage may be suitable for those who expect to receive a large sum of money or plan to sell the property before the balloon payment is due. Federal Housing Administration (FHA) loans are government-backed mortgages designed to help low-to-moderate-income borrowers qualify for a mortgage. They typically require a smaller down payment and have more lenient credit requirements compared to conventional loans. Veterans Affairs (VA) loans are government-backed mortgages available to eligible veterans, active-duty service members, and some surviving spouses. VA loans often require no down payment and have competitive interest rates. United States Department of Agriculture (USDA) loans are government-backed mortgages designed for rural homebuyers with low-to-moderate incomes. These loans often require no down payment and have competitive interest rates. Jumbo loans are mortgages that exceed the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These loans typically have stricter credit requirements and may require a larger down payment. A borrower's credit score is a key factor in determining eligibility for a mortgage, as well as the interest rate offered. A higher credit score often leads to better mortgage terms. Lenders consider a borrower's income stability to ensure they can consistently make mortgage payments. Stable employment history and sufficient income are essential for mortgage approval. The debt-to-income (DTI) ratio compares a borrower's monthly debt payments to their gross monthly income. Lenders use this ratio to assess a borrower's ability to manage monthly mortgage payments. Identify the preferred location for the property, taking into consideration factors such as proximity to work, schools, and amenities. Determines the type of property desired, such as a single-family home, condominium, or townhouse. Establish a timeline for buying the property, considering factors such as job stability, family planning, and financial readiness. Obtain a mortgage pre-approval to determine the maximum loan amount and interest rate a lender is willing to offer. This provides a realistic estimate of affordability and strengthens the homebuying position. Evaluate the required down payment for the desired mortgage, as this can significantly affect the overall affordability of the property. Consider available savings and potential sources of down payment assistance. Calculate estimated monthly mortgage payments based on the loan amount, interest rate, and loan term. Ensure these payments align with your budget and financial goals. Mortgage rates are influenced by various factors, including credit score, loan-to-value ratio, loan term, and market conditions. Understanding these factors can help borrowers secure the best possible rate. Compare mortgage rates and terms from multiple lenders to find the most suitable option. Remember that interest rates are not the only consideration; also, take into account fees and other loan features. Mortgage terms are typically 30 years. Shorter loan terms generally have lower interest rates but higher monthly payments, while longer terms have higher interest rates and lower monthly payments. An amortization schedule outlines the allocation of each monthly payment towards the principal and interest over the loan term. Understanding the schedule can help borrowers plan for principal reduction and potential tax deductions. Some mortgages offer prepayment options, allowing borrowers to make additional payments towards the principal without incurring penalties. This can help save on interest and pay off the loan faster. The loan origination fee covers the lender's costs for processing the mortgage application. This fee can vary depending on the lender and loan type. An appraisal fee is charged to determine the fair market value of the property. This ensures the property's value aligns with the loan amount. Title insurance protects the lender and homeowner from any potential disputes or claims against the property's ownership. Property taxes are levied by local governments and are based on the assessed value of the property. These taxes are usually paid on a semi-annual or annual basis. Homeowners insurance protects the property from potential damages and liabilities. Lenders typically require borrowers to maintain adequate insurance coverage. Mortgage insurance is required for loans with a down payment of less than 20% of the property's value. This insurance protects the lender in case the borrower defaults on the loan. If the property is part of a homeowners association, monthly or annual fees may apply. These fees cover the maintenance and management of shared community amenities and facilities. An accelerated payment plan involves making additional or higher payments to reduce the loan principal faster, ultimately saving on interest and shortening the loan term. Making extra payments towards the principal can help reduce the loan balance and save on interest over the life of the loan. Loan recasting involves making a large lump sum payment towards the principal and requesting the lender to re-amortize the remaining loan balance, resulting in lower monthly payments. Refinancing involves replacing the current mortgage with a new one, often at a lower interest rate or with different loan terms. This strategy can help save on interest or reduce monthly payments. Homeowners can deduct the mortgage interest paid on their primary residence from their taxable income, subject to certain limitations. Points, or prepaid interest, paid at closing may also be tax-deductible, depending on the borrower's eligibility and circumstances. Property taxes paid on a primary residence can also be deducted from taxable income, subject to certain limitations and eligibility requirements. Maintaining an emergency savings fund can help cover unexpected expenses, such as home repairs or temporary income loss, without jeopardizing mortgage payments. Mortgage protection insurance covers mortgage payments in the event of job loss, disability, or death. This insurance provides financial security for borrowers and their families during difficult times. Home warranty plans offer coverage for the repair or replacement of major home systems and appliances. These plans can help homeowners manage unexpected repair costs and protect their investment. Mortgage planning is a vital component of homeownership, as it equips borrowers with the knowledge and tools necessary to make well-informed decisions about their most significant investment. By comprehending the various types of mortgages, evaluating personal financial situations, and considering both additional costs and potential repayment strategies, prospective homeowners can develop a mortgage plan tailored to their unique financial goals and long-term stability. Furthermore, mortgage planning assists in selecting the right mortgage rate and term, preparing for unexpected expenses, and understanding the tax implications of mortgages. Ultimately, effective mortgage planning leads to sound financial decisions and a more secure future for homeowners.Mortgage Planning Overview

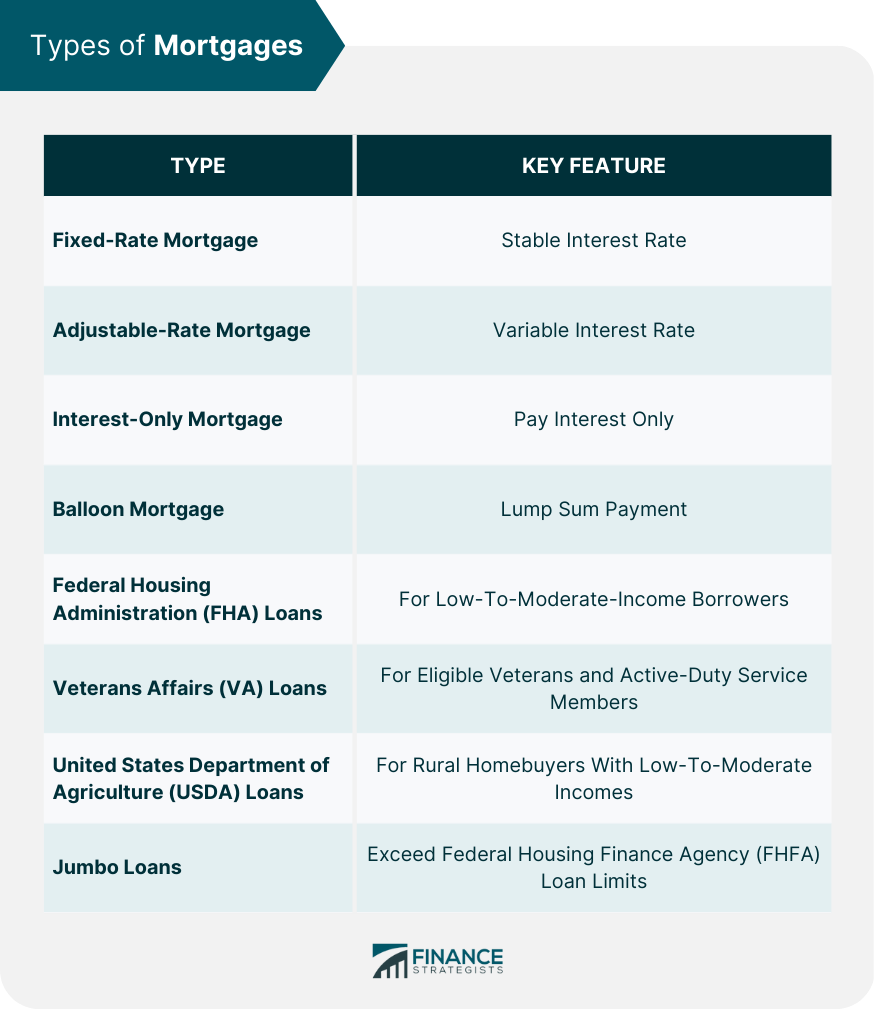

Types of Mortgages

Fixed-Rate Mortgage

Adjustable-Rate Mortgage

Interest-Only Mortgage

Balloon Mortgage

FHA Loans

VA Loans

USDA Loans

Jumbo Loans

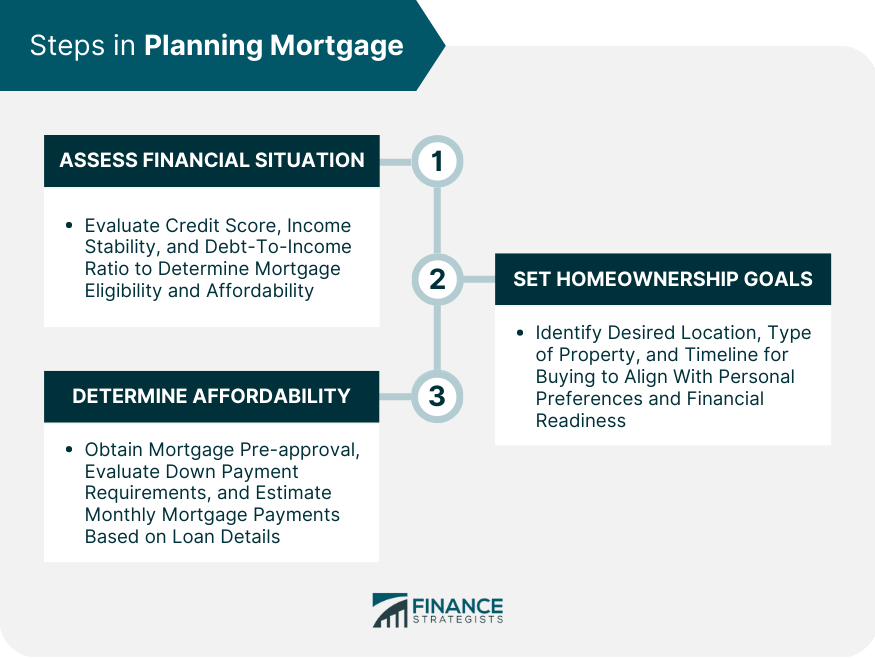

Mortgage Planning Process

Assessing Financial Situation

Credit Score

Income Stability

Debt-to-Income Ratio

Setting Homeownership Goals

Desired Location

Type of Property

Timeline for Buying

Determining Affordability

Mortgage Pre-Approval

Down Payment Requirements

Monthly Mortgage Payment Estimates

Mortgage Rates and Terms

Understanding Mortgage Rates

Factors Affecting Rates

Comparison Shopping

Mortgage Terms

Loan Term Length

Amortization Schedule

Prepayment Options

Additional Costs and Fees

Closing Costs

Loan Origination Fee

Appraisal Fee

Title Insurance

Ongoing Costs

Property Taxes

Homeowners Insurance

Mortgage Insurance

Homeowners Association (HOA) Fees

Mortgage Repayment Strategies

Accelerated Payment Plans

Extra Payments Towards Principal

Loan Recasting

Refinancing

Tax Implications of Mortgages

Mortgage Interest Deduction

Points Deduction

Property Tax Deduction

Preparing for the Unexpected

Emergency Savings

Mortgage Protection Insurance

Home Warranty Plans

Conclusion

Mortgage Planning FAQs

Mortgage planning plays a crucial role in personal finance, as it helps borrowers evaluate and choose the best mortgage options based on their financial situation and goals. By understanding different types of mortgages and their implications, homeowners can make informed decisions that lead to long-term financial stability.

Mortgage planning involves obtaining a mortgage pre-approval, which determines the maximum loan amount and interest rate a lender is willing to offer. This provides a realistic estimate of affordability and strengthens the homebuying position. Additionally, mortgage planning helps borrowers evaluate down payment requirements and estimate monthly mortgage payments based on the loan amount, interest rate, and loan term.

Mortgage planning involves understanding the factors that affect mortgage rates, such as credit score, loan-to-value ratio, and market conditions. By comparing mortgage rates and terms from multiple lenders, borrowers can find the most suitable option for their needs. Mortgage planning also helps borrowers choose the appropriate loan term length, considering the trade-offs between interest rates and monthly payments.

Mortgage planning should account for closing costs, such as loan origination fees, appraisal fees, and title insurance, as well as ongoing costs like property taxes, homeowners insurance, mortgage insurance, and homeowners association (HOA) fees. These costs can significantly impact the overall affordability of the property and should be factored into the mortgage planning process.

Yes, mortgage planning can help borrowers explore various mortgage repayment strategies, such as accelerated payment plans, making extra payments towards the principal, loan recasting, and refinancing. By implementing these strategies, homeowners can potentially save on interest, reduce monthly payments, or shorten the loan term.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.