Paying off a mortgage is often one of the most significant financial achievements for many homeowners. Mortgage payoff strategies are various methods employed to accelerate mortgage repayment, reduce interest costs, and ultimately achieve financial freedom. The importance of paying off a mortgage early cannot be overstated, as it can provide increased financial security, flexibility, and peace of mind. Refinancing is a popular mortgage payoff strategy that involves replacing the existing mortgage with a new one, often with more favorable terms or lower interest rates. This strategy can help homeowners save on interest payments and shorten the loan term. There are two main types of refinancing: rate-and-term refinancing and cash-out refinancing. Rate-and-term refinancing aims to secure a lower interest rate or change the loan term, while cash-out refinancing allows homeowners to access their home equity in the form of cash. Before refinancing, homeowners should weigh the costs and benefits, including closing costs, the new interest rate, and the time it takes to break even. Additionally, credit scores and current market conditions can impact the success of refinancing. Making extra payments towards the mortgage principal is another effective way to pay off a mortgage faster. Homeowners may choose to apply for lump-sum payments from an inheritance, windfalls, or tax refunds toward their mortgage principal. This strategy can significantly reduce the outstanding balance and interest paid over the loan term. By making bi-weekly payments instead of monthly payments, homeowners can make an extra payment each year, accelerating the mortgage payoff process. Bi-weekly payments can help homeowners save on interest costs and reduce the loan term by several years. To implement bi-weekly payments, homeowners can either work with their lender or set up a separate account to ensure timely payment. Homeowners can make additional principal payments either monthly, quarterly, or annually. These payments reduce the principal balance and overall interest paid, accelerating mortgage payoff. Recasting involves making a large lump-sum payment towards the mortgage principal and having the lender re-amortize the loan with the new balance, resulting in lower monthly payments. Recasting can provide lower monthly payments and increased cash flow, but it does not shorten the loan term or reduce the interest rate. Lenders often have specific eligibility requirements for recasting, including minimum payment amounts and restrictions on government-backed loans. The debt snowball method focuses on paying off debts with the smallest balances first while making minimum payments on all other debts. This method can provide quick wins and motivate individuals to continue their debt payoff journey. However, it may not be the most cost-effective strategy, as it does not prioritize high-interest debts. The debt avalanche method involves paying off debts with the highest interest rates first while making minimum payments on all other debts. This method saves more money on interest payments but may require more time before achieving noticeable results. Individuals should consider their financial goals, motivation levels, and debt balances when selecting between these methods. Understanding one's financial situation is crucial when choosing a mortgage payoff strategy. Homeowners should evaluate their income, expenses, and savings to determine the most suitable approach. Homeowners should consider their mortgage interest rates and remaining loan terms when selecting a payoff strategy. For instance, a low-interest rate may justify investing extra funds elsewhere, while a high-interest rate may warrant prioritizing mortgage payoff. Before focusing on mortgage payoff, homeowners should consider other financial goals and obligations. Maintaining an emergency fund is essential for financial stability. Homeowners should ensure they have sufficient savings to cover unexpected expenses before aggressively paying off their mortgage. Contributing to retirement savings is crucial for long-term financial security. Homeowners should evaluate their retirement goals and ensure they are on track before allocating additional funds towards mortgage payoff. For parents, saving for their children's college tuition may be a priority. Balancing mortgage payoff with college savings requires careful planning and consideration of various factors, such as tuition costs, financial aid, and investment returns. Homeowners should consider the potential returns on investment opportunities before directing additional funds towards mortgage payoff. In some cases, investing in the stock market or other investment vehicles may yield higher returns than paying off a low-interest mortgage. A well-crafted budget can help homeowners track their income, expenses, and progress toward mortgage payoff. Regularly reviewing and adjusting the budget is crucial for financial success. Homeowners should set realistic goals for mortgage payoff, taking into account their current financial situation and other financial priorities. Automating extra mortgage payments can help homeowners stay on track and ensure consistent progress towards their mortgage payoff goal. Regularly reviewing the mortgage balance and overall progress can help homeowners stay motivated and make adjustments as needed. Homeowners should be prepared to adjust their mortgage payoff strategy based on changes in their financial situation, interest rates, or other factors. Paying off a mortgage early may come with an opportunity cost, as homeowners could potentially earn higher returns by investing in other opportunities, such as stocks or real estate. Mortgage interest is tax-deductible in some countries, and paying off a mortgage early may reduce this benefit. Homeowners should consult a tax professional to understand the implications of their mortgage payoff strategy. Directing significant funds toward mortgage payoff can reduce an individual's liquid assets, making it harder to cover unexpected expenses or take advantage of investment opportunities. Some mortgage lenders impose penalties for early mortgage payoff, which can offset the benefits of paying off a mortgage ahead of schedule. Homeowners should review their mortgage terms and consult their lenders before adopting an aggressive payoff strategy. Understanding various mortgage payoff strategies and their implications is crucial for homeowners seeking to reduce their loan term and achieve financial freedom. Key strategies include refinancing, extra payments, and recasting, while debt snowball and debt avalanche methods can also play a role in paying off mortgages along with other debts. It is essential to evaluate one's financial situation, considering factors such as mortgage rates, financial goals, and potential risks and drawbacks before selecting a strategy. By creating a budget, setting realistic goals, automating payments, monitoring progress, and adjusting strategies as needed, homeowners can effectively work towards mortgage freedom and enjoy the benefits of early mortgage payoff.Mortgage Payoff Strategies Overview

Mortgage Payoff Strategies

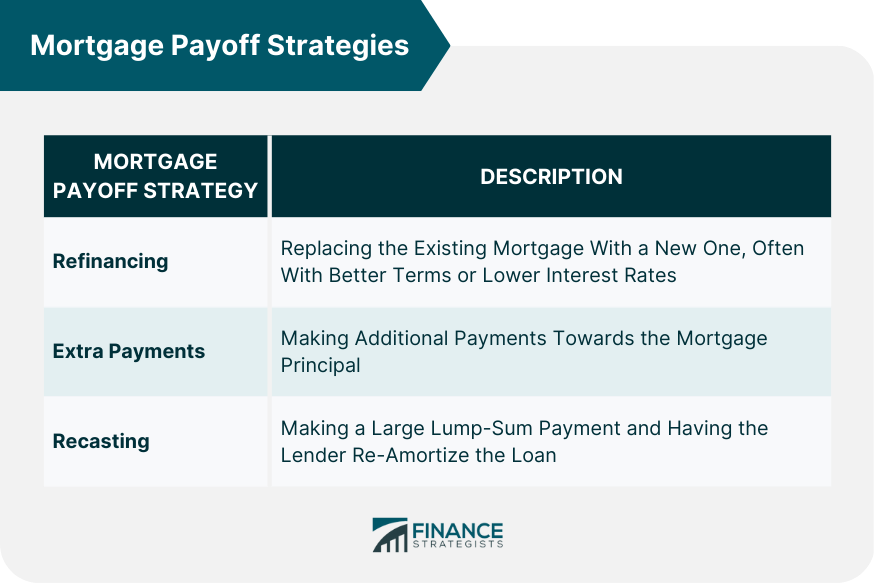

Refinancing

Types of Refinancing

Factors to Consider Before Refinancing

Extra Payments

Lump-Sum Payments

Bi-Weekly Payments

Benefits

Implementation

Additional Principal Payments

Recasting

Advantages and Disadvantages

Eligibility Requirements

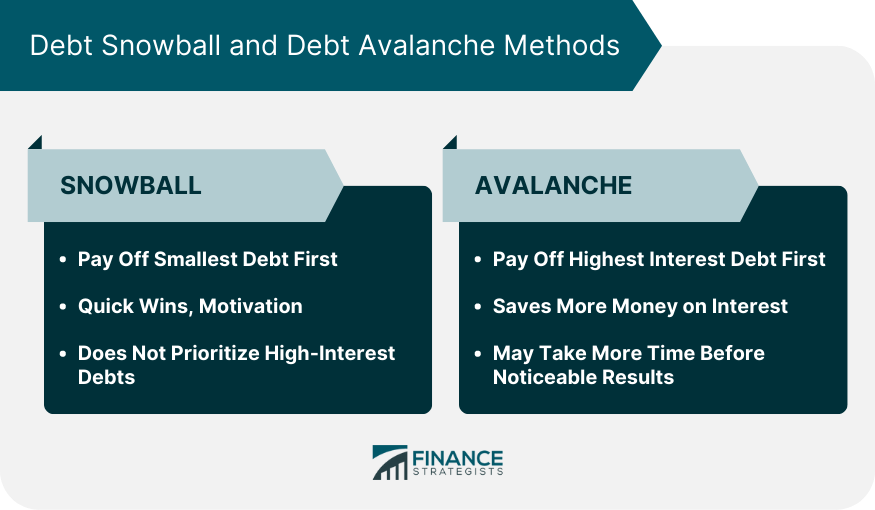

Debt Snowball and Debt Avalanche Methods

Debt Snowball Method

Benefits and Drawbacks

Debt Avalanche Method

Benefits and Drawbacks

Choosing Between Debt Snowball and Debt Avalanche

Evaluating Your Financial Situation

Assessing Income, Expenses, and Savings

Considering Mortgage Rates and Terms

Balancing Other Financial Goals

Emergency Fund

Retirement Savings

College Tuition

Investments

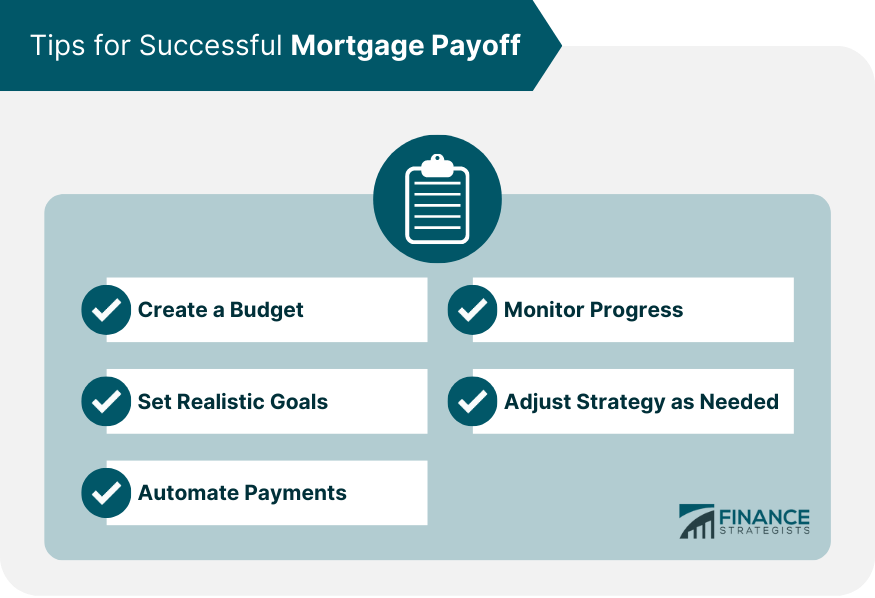

Tips for Successful Mortgage Payoff

Creating a Budget

Setting Realistic Goals

Automating Payments

Monitoring Progress

Adjusting Strategy as Needed

Potential Risks and Drawbacks

Opportunity Cost

Tax Implications

Reduced Liquidity

Early Payoff Penalties

Bottom Line

Mortgage Payoff Strategies FAQs

Some of the most common mortgage payoff strategies include refinancing, making extra payments (such as lump-sum payments, bi-weekly payments, or additional principal payments), and recasting. Each of these strategies has its own benefits and drawbacks, so it's essential for homeowners to carefully consider their personal financial situation before choosing a strategy.

The debt snowball and debt avalanche methods are primarily used for paying off multiple debts, including mortgages. These methods can be incorporated into mortgage payoff strategies to help homeowners prioritize their debts and systematically pay them off. The debt snowball method focuses on paying off smaller debts first, while the debt avalanche method targets debts with the highest interest rates.

To evaluate the best mortgage payoff strategies for your financial situation, start by assessing your income, expenses, and savings. Consider your mortgage interest rate, remaining loan term, and other financial goals like emergency funds, retirement savings, college tuition, and investment opportunities. Additionally, consult a financial advisor to help you make informed decisions based on your unique circumstances.

Yes, there are potential risks and drawbacks to using mortgage payoff strategies to pay off your loan early. These may include opportunity costs, tax implications, reduced liquidity, and early payoff penalties. It's crucial to weigh these factors against the benefits of early mortgage payoff before deciding on a strategy.

To stay on track with your chosen mortgage payoff strategies, create a budget, set realistic goals, automate extra payments, monitor your progress, and adjust your strategy as needed. Keeping a close eye on your financial situation and making necessary adjustments will help ensure you achieve mortgage freedom and reap the benefits of an early mortgage payoff.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.