Level-premium insurance is a type of life insurance policy in which the premium payments remain constant throughout the entire term of the policy. This means that the policyholder pays the same amount each year, regardless of changes in their age, health, or other factors that might otherwise affect their premium. This form of insurance offers a predictable and stable method of providing financial security for the policyholder's beneficiaries. In contrast to level-premium insurance, other types of insurance premiums may fluctuate over time. For example, annually renewable term life insurance policies have premiums that increase each year as the policyholder ages, while universal life insurance policies may have flexible premiums that can be adjusted based on the policyholder's financial needs and goals. The primary purpose of level-premium insurance is to provide financial protection to the policyholder's dependents or beneficiaries in the event of their death. This form of insurance offers several benefits, including: 1. Predictable premium payments remain the same throughout the term of the policy, making it easier for policyholders to budget for their insurance expenses. 2. Long-term cost savings as compared to other forms of insurance premiums, may increase over time. 3. Protection against inflation, as the constant premium payments are locked in at the time of policy purchase. 4. Encouraging policyholders to purchase insurance earlier in life, which can result in more affordable premiums. Level-term life insurance is a type of life insurance policy that provides coverage for a specific period, usually 10, 20, or 30 years. The key features of level-term life insurance include: 1. Fixed premium payments that remain the same throughout the term of the policy. 2. Death benefits that are paid to beneficiaries if the policyholder dies during the term of the policy. 3. No cash value component, meaning that the policy does not accumulate any cash value over time. Level-term life insurance offers several benefits for policyholders, including: 1. Affordable coverage for a specified period, making it ideal for individuals who require financial protection for a limited time, such as during their working years or while raising a family. 2. Predictable premium payments, which can provide peace of mind for policyholders who want to ensure their beneficiaries are protected without the worry of increasing premiums. Whole life insurance is a type of permanent life insurance policy that provides coverage for the policyholder's entire life, as long as premium payments are maintained. The key features of whole life insurance include: 1. Level premium payments remain the same for the life of the policy. 2. Guaranteed death benefits are paid to beneficiaries upon the policyholder's death. 3. Cash value component that accumulates over time and can be accessed through policy loans or withdrawals. Whole life insurance offers several benefits for policyholders, including: 1. Lifetime coverage, which ensures that beneficiaries will receive a death benefit regardless of when the policyholder dies. 2. Forced savings component through the cash value accumulation, which can provide policyholders with an additional source of funds for emergencies, retirement, or other financial goals. 3. The potential for dividends, which some whole life insurance policies may pay to policyholders based on the insurer's financial performance. Universal life insurance is a type of permanent life insurance policy that combines the flexibility of adjustable premium payments with the security of a guaranteed death benefit. The key features of universal life insurance include: 1. Level premium payments, which can be adjusted by the policyholder based on their financial needs and goals. 2. Guaranteed death benefits are paid to beneficiaries upon the policyholder's death. 3. Cash value component that accumulates over time and can be accessed through policy loans or withdrawals. 4. Flexible premiums and adjustable death benefits allowing policyholders to customize their coverage based on their changing needs. 1. Universal life insurance offers several benefits for policyholders, including: 2. Lifetime coverage with the added flexibility of adjustable premium payments and death benefits, allowing policyholders to adapt their coverage as their financial needs change. 3. The potential for tax-deferred growth of the cash value component, which can be an attractive feature for long-term financial planning. 4. The ability to borrow against or withdraw from the cash value, providing policyholders with additional financial resources when needed. The age of the policyholder is a significant factor in determining the cost of level-premium insurance policies. Generally, the younger the policyholder, the lower the premium rate. This is because younger individuals typically have a longer life expectancy, which means that the insurance company is likely to collect more premium payments before needing to pay out a death benefit. A policyholder's health and medical history also play a critical role in determining the cost of level-premium insurance. Individuals with pre-existing medical conditions or a history of chronic illnesses may be considered higher risk by insurance companies, resulting in higher premium rates. Some insurers may require applicants to undergo a medical exam to assess their risk level accurately. The policyholder's occupation and lifestyle can also impact the cost of level-premium insurance policies. Occupations that are considered high-risk, such as construction workers, firefighters, or pilots, may result in higher premium rates due to the increased likelihood of injury or death. Additionally, individuals who engage in high-risk activities, such as skydiving or extreme sports, may also face higher premiums. The term of the policy and the amount of coverage purchased also influence the cost of level-premium insurance. Generally, policies with longer terms and higher coverage amounts will have higher premium rates, as the insurance company is taking on a greater risk by providing coverage for an extended period and larger death benefits. Gender and smoking status can also impact level-premium insurance rates. Generally, women tend to have lower premium rates than men, as they typically have a longer life expectancy. Additionally, non-smokers are likely to receive lower premium rates than smokers, as smoking is associated with a higher risk of death due to health complications. One of the primary advantages of level-premium insurance is the predictability of premium payments. Policyholders can confidently budget for their insurance expenses, knowing that their premiums will remain the same throughout the term of the policy. This consistency can alleviate financial stress and help policyholders manage their finances more effectively. Level-premium insurance policies can offer long-term cost savings compared to other types of insurance premiums that may increase over time. As policyholders age, the cost of obtaining new coverage typically rises. However, with level-premium insurance, the premiums are locked in at the time of policy purchase, providing a more affordable option in the long run. Inflation can erode the purchasing power of money over time, potentially impacting a policyholder's ability to afford insurance premiums in the future. Level-premium insurance provides protection against inflation by locking in premium rates at the time of policy purchase, ensuring that policyholders will not face increased costs due to rising inflation rates. Level-premium insurance encourages individuals to purchase policies earlier in life when premiums are typically more affordable. Purchasing a policy at a younger age can result in lower premium rates, providing an incentive for individuals to secure financial protection for their beneficiaries sooner rather than later. One of the main disadvantages of level-premium insurance is the higher initial premium costs compared to other types of insurance premiums. Because the premium rates are locked in and remain constant throughout the policy term, insurers often charge higher initial premiums to account for the increased risk associated with providing coverage for an extended period. Level-premium insurance policies may offer limited flexibility in terms of adjusting coverage amounts or premium payments throughout the policy term. This lack of flexibility can be a disadvantage for policyholders whose financial needs and goals change over time, as they may not be able to adjust their coverage accordingly. In some cases, policyholders may end up overpaying for coverage with level-premium insurance policies. If a policyholder's financial needs decrease over time, they may be paying for more coverage than necessary, resulting in an inefficient use of their insurance budget. Level-premium insurance policies can be complex, with numerous terms and conditions that policyholders must understand to make informed decisions. The complexity of these policies can be a disadvantage for individuals who may struggle to comprehend the nuances of their coverage and the long-term implications of their choices. Before purchasing a level-premium insurance policy, it's essential for individuals to assess their financial needs and goals. This process can help them determine the appropriate coverage amount and policy term to ensure that their beneficiaries will be adequately protected in the event of their death. Policyholders should compare multiple level-premium insurance policy options and providers to ensure they are getting the best coverage at the most competitive rates. By researching and comparing different policies, individuals can make informed decisions about which policy is best suited to their specific needs and budget. Some level-premium insurance policies offer optional riders or additional features that can provide added benefits and protection. 1. Accelerated Death Benefit Rider: This rider allows the policyholder to receive a portion of the death benefit in advance if they are diagnosed with a terminal illness or critical illness. 2. Waiver of Premium Rider: With this rider, if the policyholder becomes disabled and is unable to pay the premiums, the insurance company waives the premium payments while keeping the coverage in force. 3. Guaranteed Insurability Rider: This rider enables the policyholder to purchase additional coverage in the future without undergoing a medical exam or providing evidence of insurability. 4. Accidental Death Benefit Rider: This rider provides an additional death benefit if the policyholder dies as a result of an accident on top of the base death benefit. 5. Child Term Rider: This rider provides coverage for the policyholder's children, usually at a lower cost, for a specified term. 6. Return of Premium Rider: This rider refunds a portion or all of the premiums paid if the policyholder survives the policy term. Policyholders should carefully evaluate these options to determine if they are worth the additional cost and if they align with their overall financial goals and objectives. Consulting with a financial advisor or insurance agent can provide valuable guidance and insight when choosing a level-premium insurance policy. These professionals can help individuals assess their financial needs, compare policy options, and navigate the complexities of insurance policies and terms. By leveraging their expertise, policyholders can make more informed decisions and ensure they select the most appropriate level-premium insurance policy for their unique situation. Level-premium insurance offers a predictable and stable method of providing financial security for the policyholder's beneficiaries. It provides several benefits, including predictable premium payments, long-term cost savings, protection against inflation, and encouragement of early purchase. Different types of level-premium insurance, such as level-term life insurance, whole life insurance, and universal life insurance, cater to various coverage needs. The cost of level-premium insurance is influenced by factors such as age, health, occupation, and policy term. While there are advantages to level-premium insurance, such as budget predictability and long-term cost savings, there are also drawbacks, including higher initial premium costs and limited flexibility in coverage. Individuals should carefully assess their financial needs, compare policy options, and consider consulting with professionals when choosing the right level-premium insurance policy.What Is Level-Premium Insurance?

Purpose and Benefits of Level-Premium Insurance

Types of Level-Premium Insurance

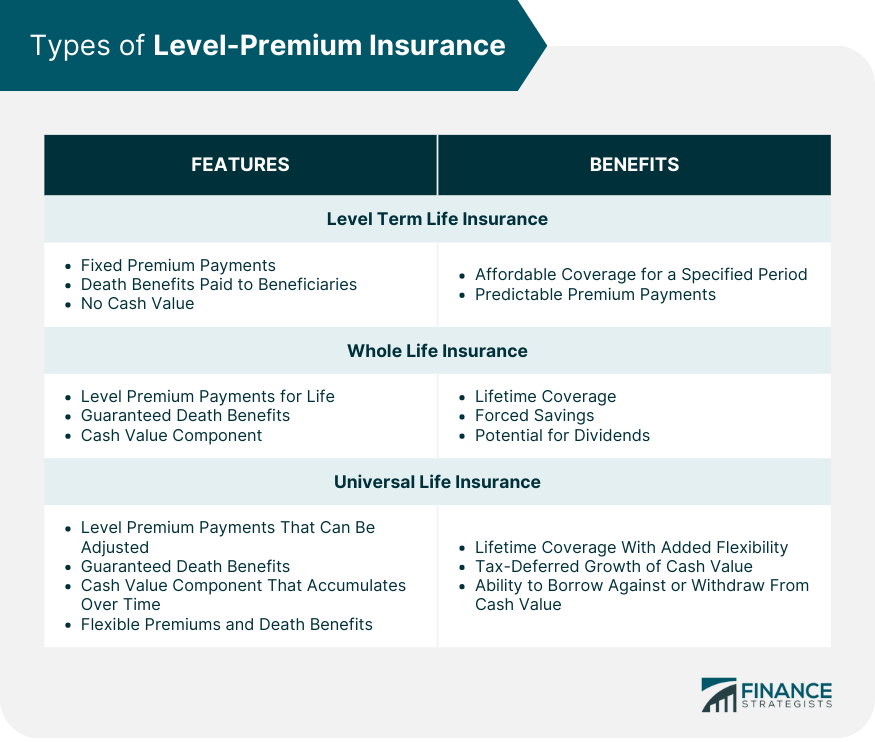

Level Term Life Insurance

Features

Benefits

Whole Life Insurance

Features

Benefits

Universal Life Insurance

Features

Benefits

Determining Factors for Level-Premium Insurance Rates

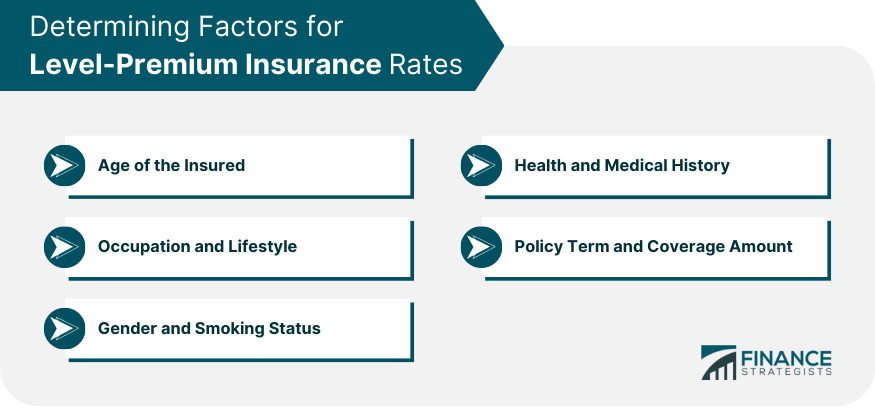

Age of the Insured

Health and Medical History

Occupation and Lifestyle

Policy Term and Coverage Amount

Gender and Smoking Status

Advantages of Level-Premium Insurance

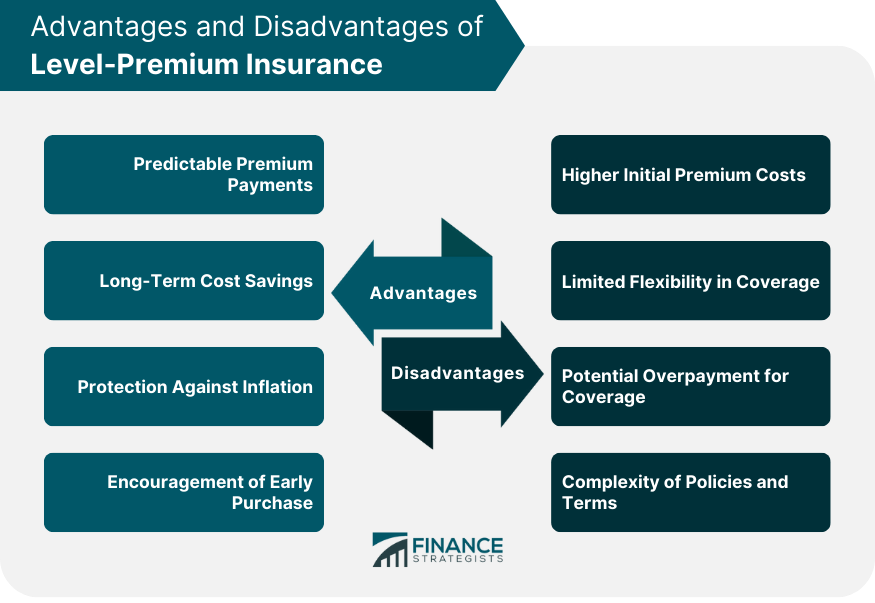

Budget Predictability

Long-Term Cost Savings

Protection Against Inflation

Encouragement of Early Purchase

Disadvantages of Level-Premium Insurance

Higher Initial Premium Costs

Limited Flexibility in Coverage

Potential Overpayment for Coverage

Complexity of Policies and Terms

Tips for Choosing the Right Level-Premium Insurance Policy

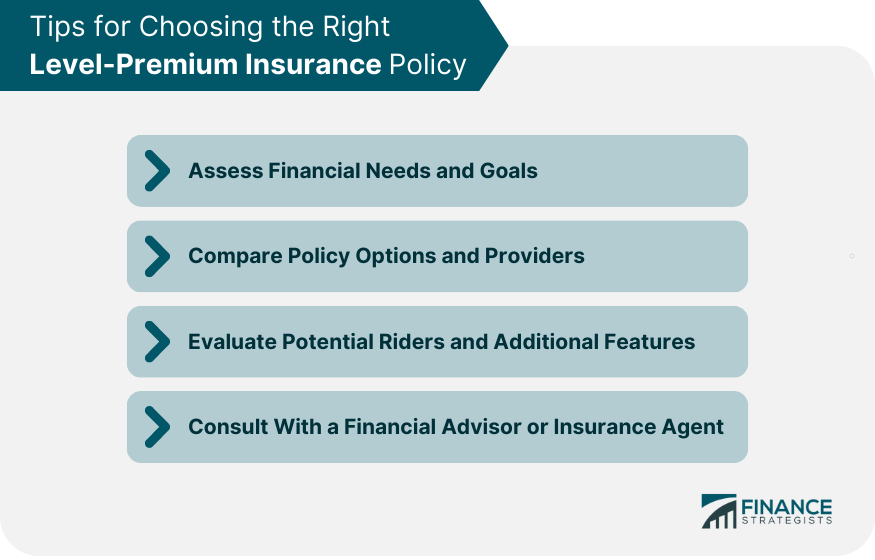

Assess Financial Needs and Goals

Compare Policy Options and Providers

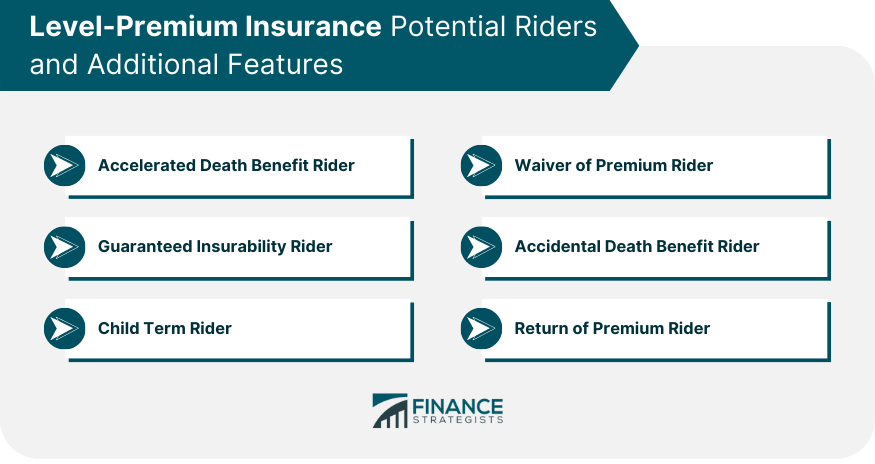

Evaluate Potential Riders and Additional Features

Consult With a Financial Advisor or Insurance Agent

Final Thoughts

Level-Premium Insurance FAQs

The main difference between level-premium insurance and other types of insurance premiums is that level-premium insurance offers predictable and stable premium payments that remain constant throughout the term of the policy, while other types of insurance premiums may fluctuate over time.

Age is a significant factor in determining the cost of level-premium insurance policies. Generally, younger individuals have lower premium rates as they have a longer life expectancy, meaning that the insurance company is likely to collect more premium payments before needing to pay out a death benefit.

Some common disadvantages of level-premium insurance policies include higher initial premium costs, limited flexibility in coverage, potential overpayment for coverage, and the complexity of policies and terms. Policyholders should weigh these potential drawbacks against the benefits of level-premium insurance when choosing a policy.

To choose the best level-premium insurance policy, policyholders should assess their financial needs and goals, compare policy options and providers, evaluate potential riders and additional features, and consult with financial advisors or insurance agents to ensure they make an informed decision that aligns with their unique situation.

Yes, some level-premium insurance policies offer additional features or riders to enhance coverage, such as accelerated death benefits, accidental death benefits, and long-term care riders. Policyholders should carefully evaluate these options to determine if they align with their overall financial goals and objectives.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.