Medicare Supplement Insurance, also known as Medigap, is a type of insurance policy designed to help cover the gaps in Original Medicare coverage. These gaps include expenses such as deductibles, coinsurance, and copayments. Medigap policies are sold by private insurance companies and are meant to help seniors manage their healthcare costs more effectively. As healthcare costs continue to rise, having adequate insurance coverage is increasingly important for seniors. Medicare Supplement Insurance can provide financial security and peace of mind by reducing out-of-pocket expenses and ensuring that seniors have access to the care they need. There are ten standardized Medicare Supplement Insurance plans, labeled Plan A through Plan N. Each plan offers a different combination of benefits and coverage, allowing individuals to choose a plan that best suits their needs. Medicare Supplement Insurance plans vary in the benefits they provide, such as covering Part A and Part B deductibles, excess charges, and foreign travel emergency coverage. It's crucial to compare each plan's coverage options to find the best fit based on individual healthcare needs and budget. When selecting a Medicare Supplement Insurance plan, consider factors such as current health status, anticipated future healthcare needs, and budget constraints. Consulting with a licensed insurance agent or financial advisor can provide valuable guidance in making this decision. To be eligible for a Medicare Supplement Insurance plan, an individual must be enrolled in both Medicare Part A and Part B. Typically, people become eligible for Medicare at age 65, but some individuals may qualify earlier due to certain disabilities or medical conditions. The best time to purchase a Medicare Supplement Insurance policy is during the open enrollment period, which begins on the first day of the month an individual turns 65 and lasts for six months. During this period, insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. There may be special enrollment periods and exceptions for those who did not enroll in a Medigap plan during their open enrollment period. These situations can include losing employer-sponsored coverage or experiencing other qualifying life events. If an individual does not enroll in a Medicare Supplement Insurance plan during their open enrollment period, they may face late enrollment penalties, including higher premiums or denial of coverage based on pre-existing conditions. Premium rates for Medicare Supplement Insurance plans can vary depending on factors such as the plan type, the insurance company, and the individual's age, location, and tobacco use. There are three primary pricing methods for Medigap policies: community-rated, issue-age-rated, and attained-age-rated. Community-rated policies charge the same premium for all policyholders, regardless of age. Issue-age-rated policies base the premium on the age at which the policy is purchased, while attained-age-rated policies adjust the premium as the policyholder ages. Some Medicare Supplement Insurance plans include a deductible, which is the amount an individual must pay for healthcare services before the insurance begins to cover costs. and copayments are out-of-pocket costs that policyholders are responsible for when receiving healthcare services. These costs can vary depending on the specific Medicare Supplement Insurance plan. Out-of-pocket limits are caps on the amount a policyholder must pay for covered healthcare services in a given year. Once the limit is reached, the insurance plan covers 100% of the remaining costs for the rest of the year. Not all Medicare Supplement Insurance plans have out-of-pocket limits, so it's essential to consider this factor when selecting a plan. Various insurance companies offer Medicare Supplement Insurance plans, including well-known providers such as AARP, Mutual of Omaha, and Blue Cross Blue Shield. Each company may have different pricing structures, plan offerings, and customer service standards. When selecting a Medicare Supplement Insurance provider, it's essential to compare companies based on factors such as customer service, reputation, and financial stability. Reading online reviews, seeking recommendations from friends or family members, and researching the company's financial ratings can help ensure that you choose a reliable provider. In addition to comparing providers based on the factors mentioned above, consider the company's network of healthcare providers, the availability of electronic claims processing, and the ease of communication with customer service representatives. Taking the time to research and compare providers can lead to a better overall experience with your Medicare Supplement Insurance plan. If a policyholder has multiple insurance policies, the coordination of benefits process ensures that the different insurance companies work together to cover healthcare costs without overlapping or overpaying. This process is essential for avoiding unnecessary expenses and ensuring that all insurance policies function effectively. Medicare Supplement Insurance and Medicare Advantage are two distinct types of insurance options for seniors. Medicare Supplement Insurance works alongside Original Medicare to fill in coverage gaps, while Medicare Advantage is an alternative to Original Medicare that offers additional benefits and services. Individuals must choose between enrolling in a Medicare Supplement Insurance plan or a Medicare Advantage plan, as they cannot have both simultaneously. If an individual has employer or union-sponsored coverage, it's crucial to understand how that coverage interacts with Medicare Supplement Insurance. In some cases, employer-sponsored coverage may provide sufficient benefits, making it unnecessary to purchase a Medigap policy. However, if the employer-sponsored coverage leaves gaps in coverage, a Medicare Supplement Insurance plan may be beneficial. Some low-income seniors may qualify for both Medicare and Medicaid, a state and federal program that provides healthcare coverage to those in need. In these cases, Medicaid may cover some of the out-of-pocket costs not covered by Medicare, reducing the need for Medicare Supplement Insurance. However, each individual's situation is unique, and it's essential to evaluate the specific benefits provided by each program. As healthcare needs and circumstances change over time, it's essential to regularly review your Medicare Supplement Insurance coverage and plan options. This process can help ensure that you continue to have the most suitable coverage for your needs and budget. Having a clear understanding of your healthcare expenses, including premiums, deductibles, and out-of-pocket costs, is crucial for effectively managing your Medicare Supplement Insurance. Keeping track of medical bills, maintaining a healthcare budget, and discussing costs with healthcare providers can help you stay on top of your healthcare expenses. Open communication with healthcare providers and insurance companies is essential for getting the most out of your Medicare Supplement Insurance plan. Make sure to ask questions, clarify any confusion, and stay informed about changes to your coverage or plan options. Medicare Supplement Insurance plays a vital role in providing financial security and peace of mind for seniors by helping to cover the gaps in Original Medicare coverage. By reducing out-of-pocket expenses and ensuring access to necessary healthcare services, Medigap policies can significantly improve the quality of life for seniors. Selecting the right Medicare Supplement Insurance plan involves carefully considering factors such as healthcare needs, budget constraints, and the specific benefits offered by each plan. By staying informed about changes in the healthcare and insurance industries, regularly reviewing coverage options, and working closely with healthcare providers and insurance companies, seniors can make informed decisions about their coverage and enjoy greater financial security.What Is Medicare Supplement Insurance?

Types of Medicare Supplement Insurance Plans

Overview of Standardized Plans (A-N)

Comparison of Plan Benefits and Coverage

Selecting the Right Plan Based on Individual Needs

Enrollment and Eligibility

Medicare Eligibility Requirements

Open Enrollment Period and Guaranteed Issue Rights

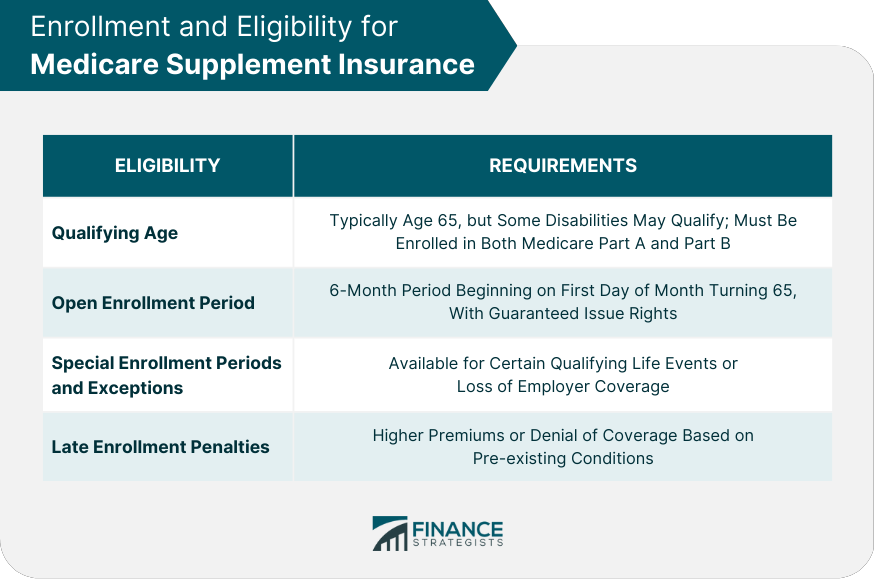

Special Enrollment Periods and Exceptions

Late Enrollment Penalties

Costs and Pricing

Premiums

Factors Affecting Premium Rates

Community-Rated, Issue-Age-Rated, and Attained-Age-Rated Pricing Methods

Deductibles

Coinsurance and Copayments

Out-Of-Pocket Limits

Medicare Supplement Insurance Providers

Overview of Insurance Companies Offering Plans

Comparison of Providers Based on Service, Reputation, and Financial Stability

Tips for Selecting the Right Provider

How Medicare Supplement Insurance Works With Other Insurance

Coordination of Benefits

Medicare Supplement Insurance vs Medicare Advantage

Working With Employer or Union-Sponsored Coverage

Interactions With Medicaid and Other Public Assistance Programs

Tips for Managing Medicare Supplement Insurance

Regularly Reviewing Coverage and Plan Options

Understanding and Managing Healthcare Expenses

Communicating With Healthcare Providers and Insurance Companies

Conclusion

Medicare Supplement Insurance FAQs

Medicare Supplement Insurance, also known as Medigap, is private health insurance that helps pay for some of the out-of-pocket costs that Original Medicare (Part A and Part B) does not cover, such as deductibles, coinsurance, and copayments.

To be eligible for Medicare Supplement Insurance, individuals must be enrolled in Original Medicare (Part A and Part B). In most states, beneficiaries must be at least 65 years old or have a qualifying disability to be eligible for Medigap.

Medicare Supplement Insurance policies work alongside Original Medicare to cover some of the costs that Medicare does not cover. Beneficiaries pay a monthly premium for their Medigap policy, in addition to their Medicare Part B premium, and the policy pays for some or all of their out-of-pocket costs.

Medicare Supplement Insurance plans are standardized and are identified by letters (such as Plan A, Plan B, etc.) in most states. Each plan offers a different combination of benefits, and all plans must cover certain basic benefits, such as Medicare Part A and Part B coinsurance and copayments. Some plans also cover additional benefits, such as foreign travel emergency coverage.

To enroll in Medicare Supplement Insurance, beneficiaries must first be enrolled in Original Medicare (Part A and Part B). Beneficiaries can then purchase a Medigap policy from a private insurance company. It is important to compare plans and costs carefully, as Medigap policies can vary significantly in price and benefits. In most states, beneficiaries have a six-month open enrollment period when they first become eligible for Medicare, during which they have guaranteed issue rights to purchase any Medigap policy they choose, regardless of their health status.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.