An annuity is a financial product designed to pay a stream of income in the future. Insurance companies usually offer it to individuals eager to secure a steady cash flow after retirement. Annuities are just one of the many financial products designed to offer income for retirees. Other options include Individual Retirement Accounts (IRAs), 401(k)s, pensions, and social security. When individuals purchase an annuity, their initial payment is referred to as the premium. Insurance companies collect the premium in the form of a lump sum or through periodic payments. During the accumulation phase, these institutions use the premium to invest in various vehicles, such as the stock market or bonds. During the pay-out phase, the annuity begins to provide a stream of income that combines a portion of the premium with any investment gains. The duration of these pay-outs can last for either a short period or for the remainder of the annuitant’s life. Annuitants or policy owners receive income payments in one of two ways: through an immediate annuity or a deferred annuity. In an immediate annuity, the annuitant starts receiving regular income relatively quickly. After investing a lump sum, annuitants may start receiving pay-outs within a year from the policy’s start date, depending on their chosen frequency. Immediate annuities are best suited for individuals nearing retirement and needing an instant and steady source of income. In a deferred annuity, the policy owner begins to receive regular income or annuity at a specified time in the future, known as the maturity date, usually after the age of 59 ½. This set-up is more suitable for younger individuals or those who do not need retirement income immediately. Pay-outs may be higher in a deferred annuity because the premium can be invested for a longer time. Despite the differences in the two options, they share one thing: the money invested in either will grow tax-free until the annuitant starts receiving payments. There are several types of annuities that offer different advantages and disadvantages. These are: Fixed annuities pay out a fixed amount. It also has a set interest rate that updates regularly after a predetermined number of years. The changes are made to adjust to the current rates in the market. Compared to other investment types, the fixed annuity is more stable because it has limits on both gains and losses. Indexed annuities fall somewhere in the middle in terms of risk and reward. They offer a guaranteed minimum payment. However, pay-out is also tied to the performance of an index, such as the Nasdaq Composite. While the income payments in this type of annuity may fluctuate, it mainly protects you from losing any of your investments if the index declines. Variable annuities offer the highest potential return of all three types. However, this type also carries the greatest risk since it is based on the performance of the annuity’s underlying investment portfolio. Payment amounts may be higher if the investment’s value increases. On the other hand, if the investments’ value dips, income payments may also be lower. It is essential to know the additional costs associated with an annuity before choosing to purchase one. Several of these fees are discussed below. Some financial advisors get an annual commission for securing the sale of the annuity. These commissions are typically not highlighted in the contract, and their total value will depend on the type of annuity. This charge protects the insurer from any losses that might occur if the policy owner unexpectedly dies. The fee is usually based on the annuitant’s age and amounts to an average of 1.25% of the account’s value each year. This charge may also be used to pay a commission to the person who sold the annuity. The issuer may charge you a flat annual fee or a percentage of your account value for administrative expenses, such as record-keeping. The investment options chosen within the annuity will have their associated fees and expenses. For example, if a fixed annuity is backed by bonds, the issuer may charge an annual fee to manage the underlying bond portfolio costs. The annuitant may need to pay a 10% penalty to the Internal Revenue Service (IRS) if the money in the account is withdrawn before age 59 ½. This early withdrawal refers to any amount withdrawn before the policy’s maturity date. Aside from the penalty levied by the IRS, insurance companies may also charge for early withdrawals through surrender charges. Depending on the investment’s values, the total penalty fees can be a significant sum, so it is crucial for policy owners to weigh their options before withdrawing funds from their annuity. Fees for special features, such as long-term care insurance or guaranteed minimum income benefit, may be charged. Understanding all the possible fees associated with an annuity is vital before getting one. There are a few advantages to getting annuities, including: Annuities can provide policy owners with a guaranteed stream of income for life. They can be used to supplement other sources of retirement income, such as a pension or Social Security. However, individuals are encouraged to invest in insurance companies with high financial strength ratings from independent rating agencies. This criterion increases the possibility that the insurer will consistently be able to pay-out the guaranteed income. The amount contributed to an annuity grows tax-deferred, which means that taxes are only due once policy owners start receiving income from the annuity. The tax break helps the invested premiums grow faster because taxes are not deducted from the earnings each year. Annuity contracts can be customized to meet policy owners’ specific needs and goals. For example, annuitants can choose a death benefit provision to ensure their loved ones will continue receiving the income after they die. Other special benefits include long-term care insurance, which can be added to the annuity after paying extra fees. There are also some disadvantages to getting annuities, including: Annuities can be expensive because of the annual fees charged by insurance companies. These fees include maintenance charges and charges for any special features added to the contract. The commission rates on annuities are usually high, which can eat into its investment returns. Depending on the type of annuity, the commission could range from around 1% to 8%. Annuities are subject to surrender charges if you withdraw your money before the start of the pay-out phase. For instance, if an annuitant has a 25-year annuity but withdraws the money after six years, they may be required to pay a surrender fee to their insurer. An additional 10% penalty fee is also due to the IRS if the money is withdrawn before the age of 59 ½. An annuity can be a good investment for people who want a consistent income stream during retirement. It can also be the right option for those who have maxed out other retirement accounts and are looking for tax-deferred growth on their investments. When extra charges are factored in, annuities can be expensive and may not be the best option for everyone. The annuity also rests on the financial strength of the chosen insurance provider. Thus, it is crucial to select a company with good ratings. Individuals may consult with a financial advisor to review different options before deciding to buy an annuity. Once an individual decides to get an annuity, there are a few things they need to do to get started. The first step is for individuals to assess their financial situation and needs. They need to know how much income they will need during retirement and how long they expect to live. Individuals must ensure that the type of annuity they choose aligns with their goals, risk tolerance, and age. Not all annuities are created equal. Individuals must compare different providers and choose those with strong financial ratings and good reputations. They can compare companies based on fees, commissions, and over-all plan features. Once the individual has selected an annuity provider, they can begin processing their application. They need to provide all the required information and review their application carefully. They must also choose how frequently they want to receive monthly, quarterly, or annual income payments. The individual also needs to decide how they will pay for the required premium. They can select between a one-time, lump-sum payment or a series of payments. They must also choose how frequently they want to receive monthly, quarterly, or annual income payments. Once an individual has applied for the annuity and paid the required premiums, most insurance companies will give a free-look period. This is a period of time when the policy owner can review the annuity contract and decide whether they want to keep it or not. If an individual decides that an annuity is not the right investment for them within this period, they get their money back without incurring a penalty. However, if the individual decides to close their annuity after the free look period, they may be asked to pay the corresponding surrender charges. An annuity is a contract between an individual and an insurance company. The individual makes a lump sum payment or series of payments. In exchange for these payments, the insurer agrees to provide the individual with regular income payments, starting immediately or in the future. There are three types of annuities–fixed, variable, and indexed–which provide different benefits depending on an individual’s needs. Annuities have a number of advantages, such as providing tax-deferred growth. However, there are also some disadvantages to consider, such as high extra fees. Whether or not an annuity is a good investment depends on an individual’s financial needs and goals. An annuity may be a good option for those seeking a way to guarantee income during retirement. However, there are other options for those who prefer more flexibility. If an individual decides to get an annuity, they must compare different providers before selecting one. They may also want to review the contract carefully and understand all the terms and conditions. Finally, they can take advantage of the free look period. If the policy owner changes their mind about an annuity, they can cancel the contract during this period without paying any charges.Annuity Definition

How Does an Annuity Work?

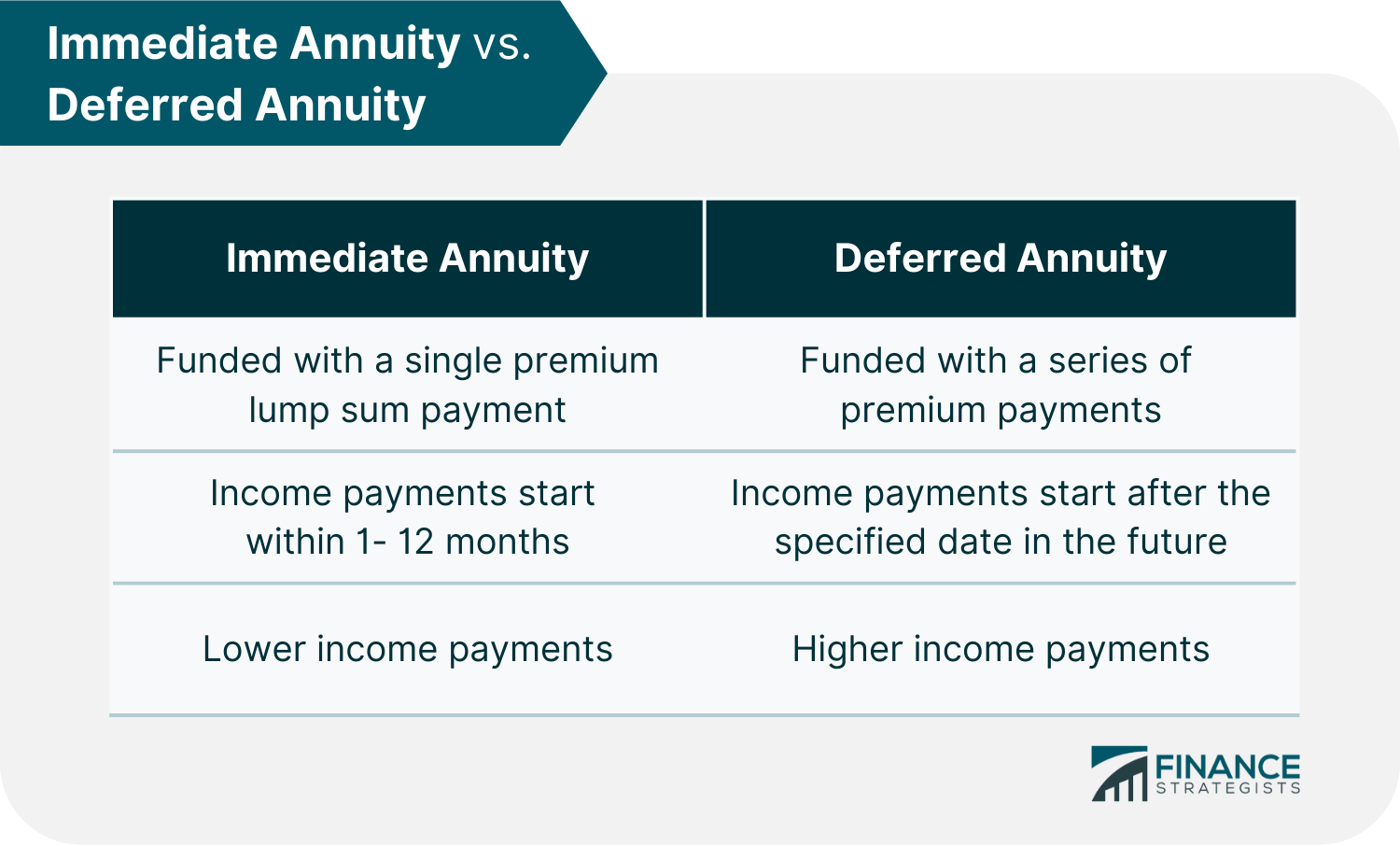

Immediate Annuity

Deferred Annuity

Types of Annuities

Fixed Annuities

Indexed Annuities

Variable Annuities

Cost of Annuities

Commissions

Mortality and Expense Risk Charges

Administrative Fees

Underlying Fund Expenses

Penalties

Fees for Extra Features

Pros of Getting Annuities

Guaranteed Regular Income

Contributions Grow Tax-Deferred

Personalized Features

Cons of Getting Annuities

Expensive Annual Fees

High Commission Rates

Subject to Penalty Fees

Are Annuities a Good Investment?

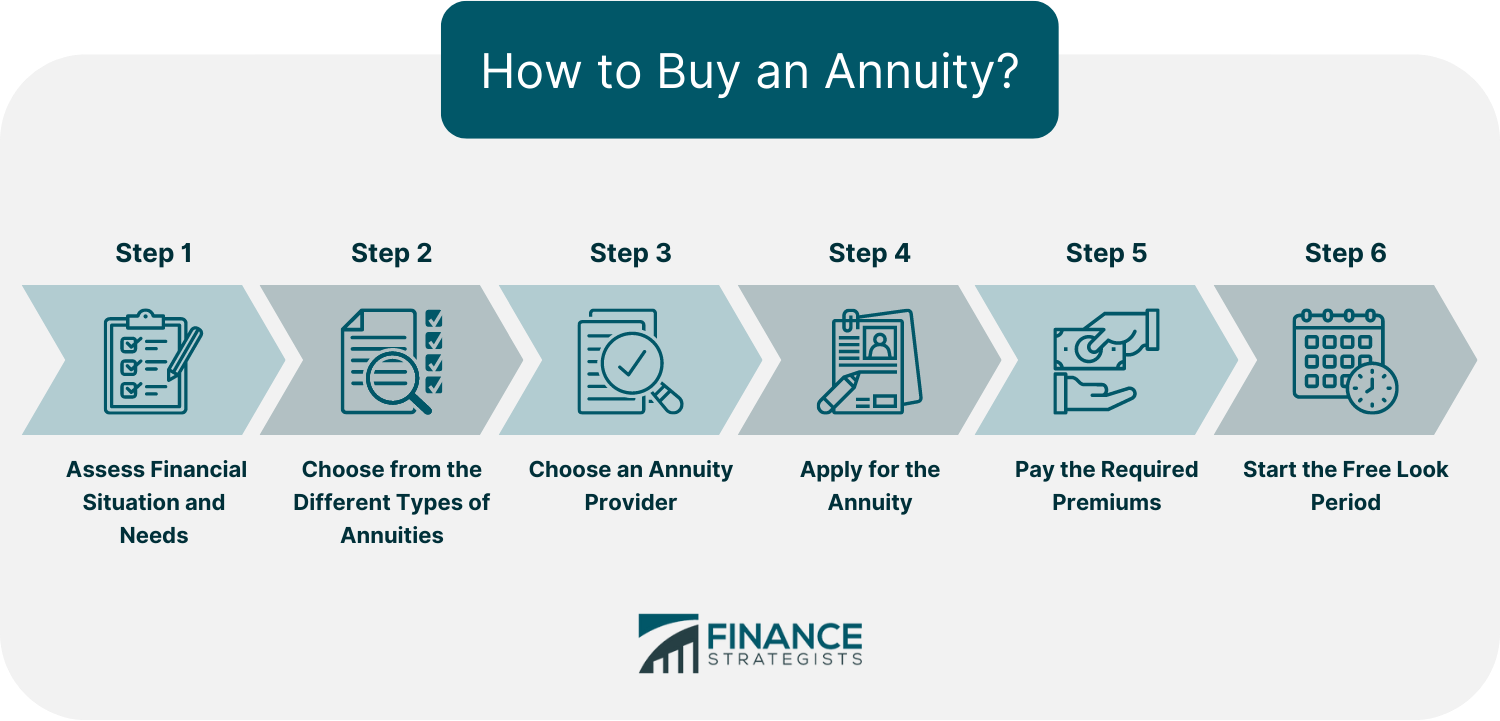

How to Buy an Annuity?

Step 1: Assess Financial Situation and Needs

Step 2: Choose from the Different Types of Annuities

Step 3: Choose an Annuity Provider

Step 4: Apply for the Annuity

Step 5: Pay the Required Premiums

Step 6: Start the Free Look Period

The Bottom Line

Annuity FAQs

An annuity is a contract between an individual and an insurance company in which the individual makes a lump sum payment or series of payments. In exchange for the payments, the insurer agrees to provide the individual with regular income, starting immediately or in the future.

Annuities provide regular income payments in exchange for your lump sum or a series of payments. Immediate annuity payments begin right away, while deferred annuities allow money to grow tax-deferred before payments start.

Annuities offer advantages such as guaranteed regular income, tax-deferred growth, and personalized features.

Annuities have a few disadvantages, including expensive annual fees, high commission rates, and early withdrawal penalty fees.

The three types of annuities are fixed, variable, and indexed. Fixed annuities pay out a fixed amount, while variable annuities offer a variable return on investment based on the performance of the annuity's underlying portfolio. Indexed annuities fall somewhere in the middle because they provide a guaranteed minimum payment, but part of the pay-out is also tied to the performance of an index.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.