An annuity ladder is a retirement income strategy that involves purchasing multiple annuities with staggered maturity dates to generate a steady, diversified stream of income. This approach helps mitigate risks associated with interest rate fluctuations and longevity while providing retirees with a reliable source of income throughout their retirement years. In today's uncertain economic environment, annuity ladders play a crucial role in helping individuals secure their financial future during retirement. This strategy can provide a consistent income stream that complements other sources of retirement income, such as Social Security benefits and pensions. An annuity ladder works by spreading out annuity purchases over time, which allows the investor to take advantage of changing interest rates and other economic factors. By creating a diversified income stream, annuity ladders can help minimize the impact of market volatility and reduce the risk of outliving one's retirement savings. Annuity ladders provide a diversified income stream by combining different types of annuities and staggering their start dates. This helps to reduce reliance on any single income source and mitigates risks associated with market fluctuations. Purchasing annuities at different times allows investors to take advantage of varying interest rates, reducing the impact of unfavorable rates on their overall retirement income. By staggering the start dates of annuity payments, annuity ladders help ensure a continuous flow of income throughout the retiree's lifetime, reducing the risk of outliving one's retirement savings. Annuity ladders can be tailored to individual needs and preferences, allowing investors to create a retirement income plan that aligns with their specific financial goals and risk tolerance. By incorporating variable and indexed annuities into the ladder, investors have the opportunity to potentially earn higher returns based on market performance, which can help combat inflation and grow retirement income over time. Inflation can erode the purchasing power of your annuity payments over time. Incorporating variable or indexed annuities into your ladder can help counteract this risk. The financial stability of the insurance company issuing the annuity is crucial, as their solvency impacts the security of your annuity payments. Research the credit ratings of potential issuers before making a purchase. Annuities are generally illiquid investments, meaning they cannot be easily converted to cash. Consider this factor when building your annuity ladder, as it may impact your ability to access funds in the event of an emergency. Annuities can come with various fees and expenses, such as surrender charges, administrative fees, and investment management fees. Evaluate the costs associated with each annuity product before making a purchase. Annuity payments are generally subject to income tax, and withdrawals made before age 59½ may incur a 10% tax penalty. Consult with a tax professional to understand the tax implications of your annuity ladder strategy. Assess your anticipated expenses during retirement, including housing, healthcare, travel, and day-to-day living costs. This will help you determine how much income you'll need to maintain your desired lifestyle. Take stock of your current retirement income sources, such as Social Security benefits, pensions, and investment accounts. This will help you identify any gaps in your retirement income that an annuity ladder can help fill. Subtract your existing sources of retirement income from your anticipated retirement expenses to identify any income gaps that need to be addressed. Determine the appropriate mix of annuity types based on your risk tolerance, financial goals, and investment horizon. This may include fixed, variable, indexed, immediate, or deferred annuities. Start building your annuity ladder by purchasing annuities with staggered start dates. This will help spread out your income sources and reduce the impact of interest rate fluctuations. Regularly review your annuity ladder to ensure it continues to meet your retirement income needs. Adjustments may be necessary as your financial situation or the economic landscape changes. Decide whether to incorporate immediate or deferred annuities into your ladder based on your current income needs and investment horizon. Immediate annuities provide income sooner, while deferred annuities allow for tax-deferred growth and future income. Consider combining different annuity types to diversify your income sources further and minimize risks. For example, a ladder might include a mix of fixed, variable, and indexed annuities. An annuity ladder can be an integral part of a broader retirement income plan, which may also include investments in stocks, bonds, and other assets. Diversifying your portfolio can further mitigate risks and enhance your financial security. Annuity ladders offer several benefits, including diversification of income sources, mitigation of risks, flexibility, and potential for higher returns. When implemented correctly, an annuity ladder can help provide a secure, reliable income stream throughout retirement. Retirement income planning is a highly personalized process that requires careful consideration of an individual's unique financial circumstances and goals. When building an annuity ladder, it is essential to work with a financial professional who can help you assess your needs and tailor a plan that aligns with your objectives. As retirement planning continues to evolve, new products and strategies will emerge that can help retirees meet their income needs. Keep an eye on trends in the industry, such as the growth of hybrid annuities or the use of technology to enhance retirement planning tools. You can make informed decisions that position you for a financially secure retirement by staying informed. Retirement planning is a complex and challenging process that requires expert knowledge and guidance. Working with an insurance broker can provide the support and expertise necessary to build an effective retirement income plan, including an annuity ladder.What Are Annuity Ladders?

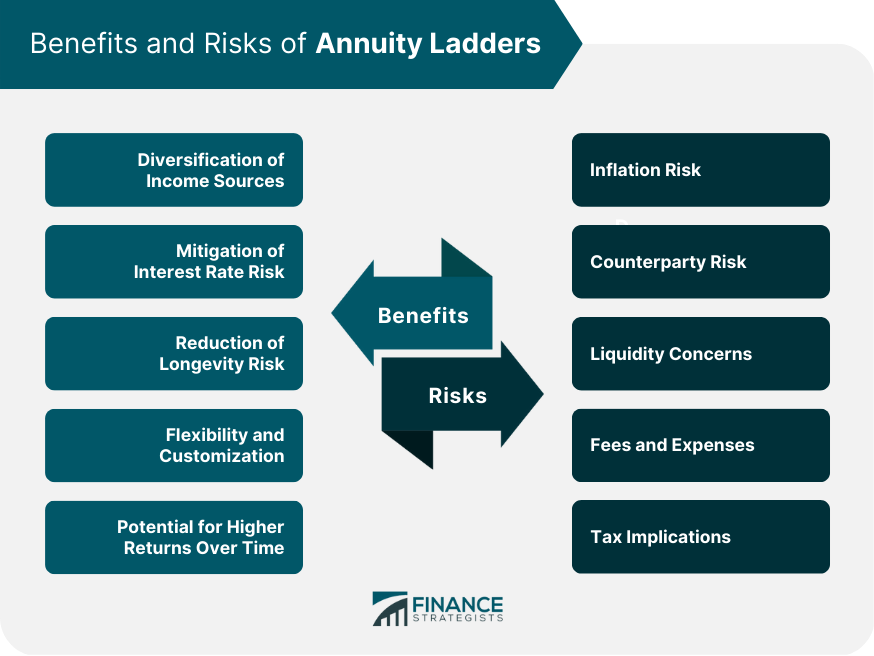

Benefits of Annuity Ladders

Diversification of Income Sources

Mitigation of Interest Rate Risk

Reduction of Longevity Risk

Flexibility and Customization

Potential for Higher Returns Over Time

Risks and Considerations

Inflation Risk

Counterparty Risk

Liquidity Concerns

Fees and Expenses

Tax Implications

Steps to Building an Annuity Ladder

Determine Retirement Income Needs

Assess Existing Sources of Retirement Income

Calculate the Annuity Income Gap

Allocate Funds to Different Annuity Types

Purchase Annuities in Stages

Monitor and Adjust the Ladder as Needed

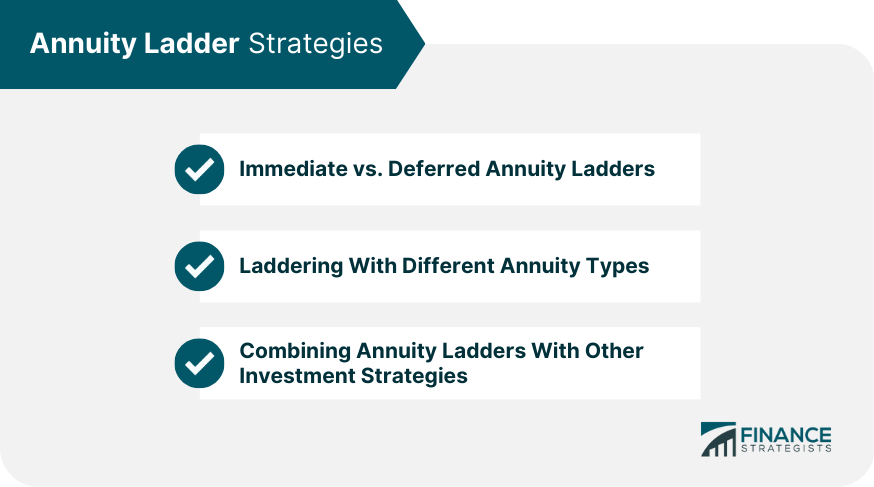

Annuity Ladder Strategies

Immediate vs. Deferred Annuity Ladders

Laddering With Different Annuity Types

Combining Annuity Ladders With Other Investment Strategies

Final Thoughts

Annuity Ladder FAQs

An annuity ladder is a retirement income strategy that involves purchasing multiple annuities with staggered maturity dates to generate a steady, diversified stream of income.

Various types of annuities can be used in an annuity ladder, including fixed, variable, indexed, immediate, and deferred annuities.

Annuity ladders offer several benefits, including diversification of income sources, mitigation of risks, flexibility, and potential for higher returns.

Investors should be aware of risks such as inflation, counterparty risk, liquidity concerns, fees, and tax implications when using an annuity ladder.

Retirement planning is complex, and working with an insurance broker can provide the support and expertise necessary to build an effective retirement income plan, including an annuity ladder.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.