Suing a financial advisor is a legal option available to clients who believe their advisor has engaged in misconduct or negligence, resulting in financial harm. To sue a financial advisor, clients must first understand their legal responsibility and liability to clients. Financial advisors are responsible for providing accurate and complete information to clients, disclosing any conflicts of interest, and avoiding engaging in fraudulent or misleading practices. Before suing a financial advisor, clients should attempt to resolve the issue through alternative dispute resolution methods, gather evidence and documentation to support their case and consult with a legal professional to assess the viability of their case. Clients who decide to sue their financial advisor must follow specific legal procedures, including filing a complaint, engaging in the discovery process, and potentially going to trial. The first step in suing a financial advisor is understanding their legal responsibility and liability to clients. Financial advisors owe a duty of care to their clients and must act in the best interests of their clients. They must also provide accurate and complete information to clients, disclose any conflicts of interest, and avoid engaging in fraudulent or misleading practices. Failure to fulfill these responsibilities may lead to legal liability for the financial advisor. Financial advisors, including Registered Investment Advisors (RIAs), Broker-Dealers (BDs), and insurance agents, can come in various forms. Each type of financial advisor has different responsibilities to their clients, as outlined below: RIAs are fiduciaries and must act in the best interest of their clients at all times. This means they are legally obligated to put their client's interests ahead of their own and provide advice that aligns with their client's goals and risk tolerance. RIAs must fully and fairly disclose all material facts related to investments and potential conflicts of interest. They must also provide ongoing monitoring of their client's investments and make changes as needed to keep their clients' portfolios aligned with their goals and objectives. BDs are held to a lower standard of care and must only recommend suitable investments for their clients. Unlike RIAs, BDs are not required to act in the best interest of their clients at all times. Instead, they must ensure that their investment recommendations suit their clients based on their financial situation, investment goals, and risk tolerance. BDs must also provide their clients with full and fair disclosure of any material facts related to investments and potential conflicts of interest. Insurance agents are responsible for providing insurance policies that meet their client's needs and objectives. They must recommend policies that are suitable for their clients based on their financial situation and insurance needs. Insurance agents must also provide full and fair disclosure of any material facts related to the policies they recommend and any potential conflicts of interest. Additionally, insurance agents must ensure that their clients understand the terms and conditions of the policies they purchase, including any fees and charges. Financial advisor misconduct or negligence can take many forms, including but not limited to the following: Making Unsuitable Investment Recommendations. This occurs when a financial advisor recommends investments that are not appropriate for a client's investment objectives, risk tolerance, or financial situation. Failing to Disclose Conflicts of Interest. A financial advisor may be incentivized to recommend an investment, not in their client's best interest, such as receiving a commission or other compensation for selling the investment. Engaging in Insider Trading. This occurs when a financial advisor uses non-public information to make trades for their benefit or to benefit their clients. Making Misrepresentations or Omissions of Material Facts. A financial advisor may make false or misleading statements about an investment or fail to disclose important information that could impact a client's decision to invest. Breach of Fiduciary Duty. Financial advisors owe their clients a fiduciary duty and must always act in their client's best interests. A breach of fiduciary duty may occur when a financial advisor puts their interests ahead of their client's interests. For example, suppose a financial advisor recommends a risky investment unsuitable for their client's investment objectives. In that case, they may be held liable for any losses incurred by the client. Additionally, if a financial advisor fails to disclose a conflict of interest or engages in insider trading, they may be subject to disciplinary action by regulatory agencies and legal liability. Clients must understand their rights and the legal options available if they believe their financial advisor has engaged in misconduct or negligence. To prove financial advisor liability in court, the client must show that the advisor breached their duty of care and that the breach caused the client's financial losses. The client must also demonstrate that the advisor had a duty to provide accurate and complete information and failed to do so and that the client relied on the advisor's advice in making the investment decision. To establish a breach of fiduciary duty claim, the client must show that the advisor breached their fiduciary duty and that the breach caused the client's financial losses. Before suing a financial advisor, there are several steps that clients can take to try to resolve the issue outside of court. Alternative dispute resolution methods, such as mediation or arbitration, may be less expensive and time-consuming than going to court. Mediation involves a neutral third party who helps the parties come to a mutually acceptable resolution. Arbitration involves a neutral third party who hears both sides of the case and makes a binding decision. Before engaging in either of these methods, clients should consult with a legal professional to ensure they are making the best decision for their case. Clients should gather as much evidence and documentation as possible to support their case. This may include investment account statements, emails, and other correspondence between the client and the advisor and any other relevant documents. Record any conversations with the advisor, including dates, times, and the discussion content is also essential. Clients should consult with a legal professional to assess the viability of their case. An experienced securities attorney can evaluate the evidence and determine whether the client has a strong case. They can also advise the client on the best course of action, whether that is to pursue legal action or attempt to resolve the issue through alternative dispute resolution methods. Clients must follow specific legal procedures if they decide to sue their financial advisor. The following steps outline the process of suing a financial advisor. The first step in suing a financial advisor is filing a court lawsuit. The client must file a complaint outlining their claim against the financial advisor. The financial advisor will be able to respond to the complaint, after which the court will schedule the case. During the discovery process, both parties exchange information and evidence that will be used in the trial. This includes depositions, sworn statements under oath and document requests. Clients must be prepared to provide evidence that supports their claim against the financial advisor. Before the case goes to trial, there may be opportunities for settlement negotiations between the client and the financial advisor. If a settlement cannot be reached, the case will proceed to trial, where the evidence will be presented, and a judge or jury will determine the outcome. Clients who sue their financial advisor may be entitled to recover damages for the financial harm caused by the advisor's actions. However, other potential outcomes of suing a financial advisor include disciplinary action against the advisor by regulatory agencies and the impact on the advisor's professional reputation and future business prospects. If the client is successful in their lawsuit, they may be entitled to recover damages for the financial harm caused by the advisor's actions. This may include reimbursement of losses, punitive damages, and attorneys' fees and costs. Regulatory agencies such as the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Authority (FINRA) may also take disciplinary action against the financial advisor if they find that the advisor violated securities laws or regulations. Disciplinary action may include fines, suspension, or revocation of the advisor's license to practice. Suing a financial advisor may also impact the advisor's professional reputation and future business prospects. A lawsuit can damage the advisor's reputation and make it more difficult to attract new clients. Suing a financial advisor is a serious decision that should not be taken lightly. Clients who believe their financial advisor harmed them should consult a legal professional to assess their options and determine the best course of action. Understanding financial advisor liability, taking steps to resolve the issue outside of court, and following legal procedures can help clients hold their financial advisors accountable and recover damages for the financial harm caused.Overview of Suing a Financial Advisor

Understanding Financial Advisor Liability

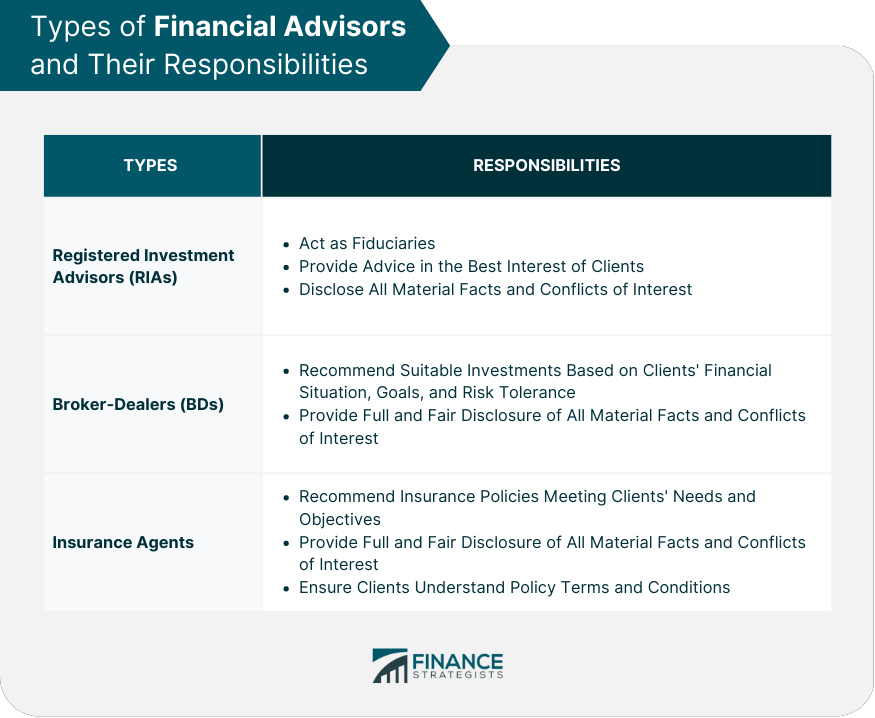

Types of Financial Advisors and Their Responsibilities to Clients

Registered Investment Advisors (RIAs)

Broker-Dealers (BDs)

Insurance Agents

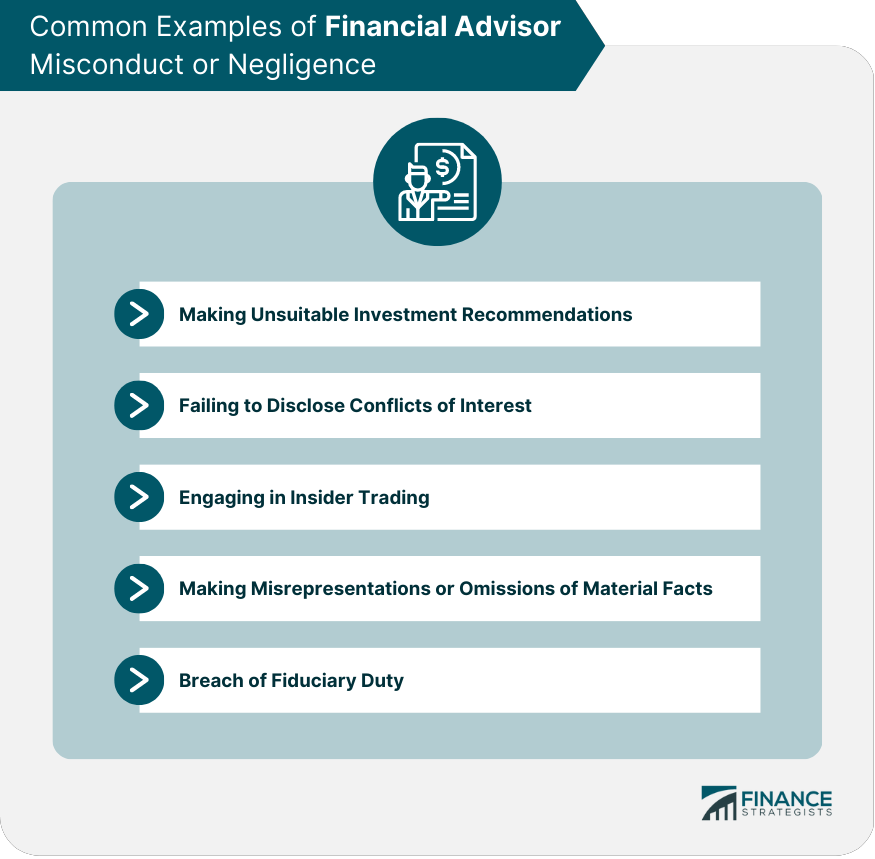

Common Examples of Financial Advisor Misconduct or Negligence

Legal Standards for Proving Financial Advisor Liability in Court

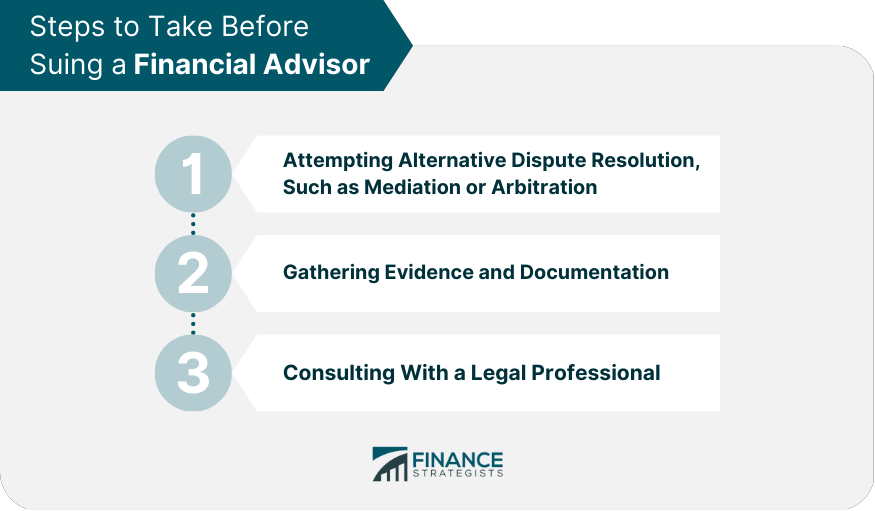

Steps to Take Before Suing a Financial Advisor

Attempting to Resolve the Issue Through Alternative Dispute Resolution Methods

Gathering Evidence and Documentation to Support the Case

Consulting With a Legal Professional to Assess the Viability of the Case

How to Sue a Financial Advisor

File a Lawsuit and Initiate Legal Proceedings

Gather Evidence to Support the Case

Negotiate Settlements or Prepare for the Potential Trial

Potential Outcomes of Suing a Financial Advisor

Recovering Damages for Financial Losses or Harm

Possible Disciplinary Action Against the Advisor

Impact on the Advisor's Reputation and Future Business Prospects

The Bottom Line

Suing a Financial Advisor FAQs

Suing a financial advisor typically involves filing a lawsuit, engaging in the discovery process to gather evidence, and potentially going to trial. Clients should consult with a legal professional to assess the viability of their case and determine the best course of action.

Financial advisor misconduct or negligence may take many forms, including making unsuitable investment recommendations, failing to disclose conflicts of interest, engaging in insider trading, misrepresentations or omissions of material facts, and breaching fiduciary duty.

If a financial advisor breaches their duty of care and causes a client's financial losses, they may be liable for damages. Clients must prove that the financial advisor's actions or advice directly caused their financial harm.

Clients who sue their financial advisor may recover damages for financial losses or harm caused by the advisor's actions, disciplinary action against the advisor by regulatory agencies, and an impact on the advisor's professional reputation and future business prospects.

Before suing a financial advisor, clients should attempt to resolve the issue through alternative dispute resolution methods, gather evidence and documentation to support their case and consult with a legal professional to assess the viability of their case. Understanding financial advisors' legal responsibility and liability to clients is also essential.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.