Passive income is generally not subject to self-employment tax, which primarily covers Social Security and Medicare taxes for individuals who work for themselves. Self-employment tax is applicable to earnings from a business or trade in which one is actively involved. Passive income, in contrast, is typically earned from endeavors where the individual does not actively participate on a regular basis. Common forms of passive income include earnings from rental properties, dividends, interest, and profits from businesses in which the individual is not materially involved. However, there are exceptions where certain types of passive income could be subject to self-employment tax, particularly if the activities are deemed to be conducted in a business-like manner. It's essential to accurately determine the nature of income and consult with a tax professional to understand specific tax obligations. The critical question of whether passive income is subject to self-employment tax hinges on how the IRS defines and categorizes this type of income. Generally, passive income is not subject to self-employment tax. However, there are exceptions based on the nature of the income and the individual’s involvement in the activity generating the income. Understanding the distinction between passive and active income is key to determining tax liabilities. Active income, or earned income, typically comes from salaries, wages, tips, and other forms of active business income. Rental income is a common form of passive income and is generally not subject to self-employment tax unless the rental activity is classified as a business. This classification can depend on several factors, such as the level of services provided with the rentals or the frequency of rental activities. Dividends, interest, and capital gains are typically considered passive income. They are often derived from investments in stocks, bonds, or mutual funds. These types of income are not subject to self-employment tax. Instead, they are taxed differently, often at lower rates than active income, making them attractive options for income generation. Income from limited partnerships or businesses in which an individual is not actively involved is also considered passive. The key factor here is the level of the individual’s direct involvement in the business operations. Such earnings are usually exempt from self-employment tax, falling under different tax rules. The calculation of taxable amounts for different types of passive income can be complex. For income streams not subject to self-employment tax, like rental income or investment earnings, the focus is on determining the net income after expenses. This calculation typically involves subtracting allowable expenses from the gross income. Once the taxable amount is determined, applying the correct tax rates and contributions is the next step. For passive income not subject to self-employment tax, this typically means adhering to capital gains tax rates or specific rental income tax rules. Complying with legal obligations for reporting passive income is critical. The IRS requires different forms for different income types, such as Schedule E for rental income or Schedule D for capital gains and losses. Proper documentation and adherence to filing procedures are key to effective tax compliance. This involves keeping detailed records of income and expenses, understanding which tax forms to use, and meeting filing deadlines. One effective tax planning strategy for passive income is to utilize tax deferral options. This can include investing in retirement accounts or other investment vehicles that offer tax-deferred growth. By deferring taxes, individuals can potentially lower their current tax liability and benefit from compound growth over time. Given the complexities of tax law, seeking professional tax advice is often a wise strategy. Tax professionals can provide guidance on tax planning, help identify applicable deductions and credits, and offer advice on structuring investments to maximize tax efficiency. There are several common myths regarding passive income and self-employment tax. One such myth is that all forms of passive income are automatically exempt from self-employment tax. Clarifying these misconceptions is important for proper tax planning and compliance. Another important aspect is ensuring accurate interpretation of tax regulations regarding passive income. Tax laws can be complex and often subject to changes and interpretations. Staying informed about the latest tax laws and seeking clarification when needed helps ensure that individuals are correctly categorizing and reporting their income, thereby avoiding potential legal complications. The taxation of passive income, particularly its subjection to self-employment tax, is a nuanced area that requires careful consideration. Passive income, typically derived from activities where the individual is not actively involved, like rental properties, dividends, interest, and business partnerships, generally does not incur self-employment tax. However, exceptions exist, particularly when passive activities are conducted in a business-like manner. Distinguishing between passive and active income is crucial for accurate tax liability determination. Various types of passive income have distinct tax implications, with considerations like the frequency of rental activities or the level of involvement in business operations affecting their classification. Calculating taxable amounts for different passive income streams, understanding legal reporting requirements, and leveraging tax planning strategies, including deferral options and professional advice, are essential for compliance and optimization. Accurately interpreting and applying tax regulations to passive income is vital to avoid misconceptions and ensure financial and legal security.Is Passive Income Subject to Self-Employment Tax?

Taxation of Passive Income

Applicability of Self-Employment Tax to Passive Income

Distinction Between Passive and Active Income for Tax Purposes

Different Types of Passive Income and Their Tax Implications

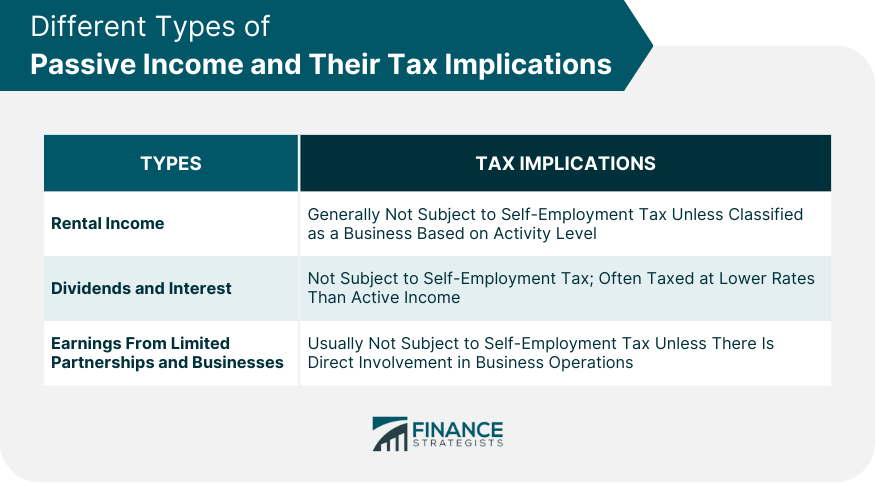

Rental Income and Self-Employment Tax

Dividends, Interest, and Capital Gains

Earnings From Limited Partnerships and Businesses

Calculating Self-Employment Tax for Different Income Streams

Methods to Calculate Taxable Amounts for Various Passive Incomes

Applying the Correct Tax Rates and Contributions

Compliance and Reporting Requirements for Passive Income and Self-Employment Tax

Legal Obligations in Reporting Passive Income

Documentation and Filing Procedures for Different Types of Income

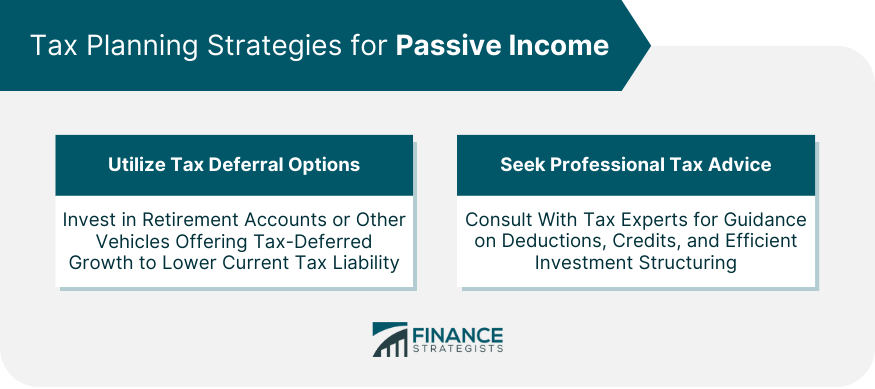

Tax Planning Strategies for Passive Income

Utilize Tax Deferral Options

Seek Professional Tax Advice

Common Misconceptions and Clarifications About Passive Income and Self-Employment Tax

Debunking Myths About Passive Income and Self-Employment Tax

Accurate Interpretation of Tax Regulations Regarding Passive Income

Conclusion

Is Passive Income Subject to Self Employment Tax? FAQs

Typically, passive income from rental properties is not subject to self-employment tax unless the rental activity is classified as a business based on the level of services provided.

No, dividends and interest are considered passive income and are usually not subject to self-employment tax. They are taxed differently, often at lower capital gains rates.

Generally, passive income from limited partnerships, where an individual is not actively involved, is not subject to self-employment tax.

Passive income from digital products, like e-books or courses, is typically not subject to self-employment tax, provided the individual is not actively involved in the business.

Passive income becomes subject to self-employment tax if the activities generating it are conducted in a business-like manner, indicating active involvement or if the IRS categorizes it as non-passive.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.