When a homeowner passes away, their property typically goes into probate. This legal process identifies and distributes the deceased's assets, but also brings up questions regarding home insurance. Importantly, the insurance should remain active during probate to protect the estate against potential risks like damage or theft. However, it's key to inform the insurance company about the owner's death, as failure to do so may render the policy invalid. It might be necessary to change the policy to a vacant home insurance if the property remains unoccupied. Additionally, the executor of the estate should ensure that all insurance premiums continue to be paid during probate. If the property is bequeathed to an heir, they should take steps to secure their own insurance policy before the end of the probate period to ensure uninterrupted coverage. Home insurance, also known as homeowners' insurance, safeguards an individual's house and its contents against losses and damages, while also providing liability coverage for accidents occurring on the property. It offers protection against potential losses, ensuring peace of mind that one's most valuable asset is secure. Probate is a legal process that ensues after a person's death. It involves validating the deceased's will, if any, managing their estate, identifying and cataloging their property, settling debts and taxes, and distributing the remaining assets to the beneficiaries. This court-supervised process ensures the estate is settled according to law and the deceased's wishes. The relationship between home insurance and probate is multifaceted. Throughout the probate process, the estate, including the home, is administered. If the deceased had home insurance, understanding its implications during probate is critical. The executor or administrator of the estate must maintain the home insurance to preserve the estate's value. During probate, it is essential to continue the home insurance coverage. The home represents a significant portion of the deceased's estate and, as such, needs protection from potential risks like fire, theft, or natural disasters. If the home is damaged without insurance coverage, the estate's value could substantially decrease, which may not fulfill the deceased's last wishes regarding asset distribution. The executor of the estate has a critical role in maintaining home insurance coverage. As the individual responsible for managing the estate during probate, the executor must ensure the insurance policy remains in effect. This responsibility involves making timely payments for the insurance premiums and updating the insurance company about the homeowner's death. After the homeowner's death, the executor should promptly contact the insurance provider to notify them of the changed circumstances. The insurance company can guide the executor on how to maintain coverage during the probate process. It is also crucial for the executor to understand any conditions or exclusions in the policy that may apply during this time. If the home becomes vacant during the probate process, the insurance policy may need to change. Many insurance providers consider a home to be vacant if it is unoccupied for 30 to 60 days, and standard homeowners' insurance may not provide coverage beyond this period. Thus, transitioning to vacant home insurance, which provides specific coverage for unoccupied properties, may be necessary. The length of the probate process can also impact home insurance. The longer the probate process takes, the longer the home may sit unoccupied, increasing the risk of damage. Insurance companies may adjust the policy conditions or premiums to reflect this increased risk. During probate, the insurance policy premiums may require adjustment. If the home is vacant and the insurance switches to a vacant home policy, the premiums could increase due to the higher risks associated with unoccupied properties. The executor must ensure these adjusted premiums are paid promptly to maintain continuous coverage. As an executor, you have what's called a fiduciary duty to the deceased person's estate. This duty requires you to act in the best interest of the estate, including maintaining necessary insurance coverage on estate properties. Neglecting this duty may result in personal legal and financial liability. Failure to maintain adequate insurance coverage can lead to serious legal consequences. If a home suffers damage or loss during probate due to insufficient insurance, beneficiaries could potentially sue the executor for breach of fiduciary duty. The executor might be personally liable to cover the loss, which can have significant financial implications. If the deceased's home insurance policy lapses during probate, the executor must act quickly to secure coverage. They may choose to reactivate the original policy if possible, or they may need to secure a new policy, possibly a vacant home insurance policy, depending on the circumstances. In some situations, the probate court may need to intervene if the deceased's insurance lapses and the executor does not promptly secure new coverage. The court could compel the executor to purchase coverage or even replace the executor if they are not adequately fulfilling their duties. If a claim must be filed during probate, the executor will typically need to handle it. This involves contacting the insurance company, providing necessary documentation, and coordinating any repairs or replacements. Insurance proceeds, if a claim is approved during probate, are typically added to the deceased's estate. These proceeds are then distributed in accordance with the deceased's will or state law, just like any other assets in the estate. Taking prompt action is critical when dealing with home insurance during probate. The sooner the insurance company is contacted and informed about the homeowner's death, the less likely the coverage will lapse. Effective communication with the insurance company can also help ensure a smooth process. Seeking legal advice can be very beneficial when handling home insurance during probate. A lawyer with experience in probate and estate law can provide guidance and help avoid potential legal pitfalls, such as a breach of fiduciary duty. Having essential documentation readily available can streamline the process. This includes the deceased's home insurance policy, death certificate, and any correspondence with the insurance company. Additionally, documentation of the home's condition, such as recent photos or appraisal reports, may be helpful if insurance claims need to be filed. Managing home insurance during probate is crucial to protecting the deceased's estate and fulfilling their wishes. The executor plays a pivotal role in this process, bearing the responsibility of maintaining coverage, making timely premium payments, and liaising with the insurance company. It's essential to anticipate changes, such as a transition to vacant home insurance or policy premium adjustments. Furthermore, fulfilling these responsibilities has legal ramifications as an executor holds a fiduciary duty. Failing to maintain insurance may lead to legal consequences and personal liability. If a policy lapses, securing new coverage promptly is important, and court intervention may occur in some cases. Claims during probate are handled by the executor, with proceeds added to the estate. Seeking legal advice can be beneficial, as can having essential documentation ready. Ultimately, prompt action, effective communication, and thoughtful handling of insurance matters can ensure a smooth probate process.What Happens to Home Insurance During Probate?

Relationship Between Home Insurance and Probate

Continuing Home Insurance During Probate

Necessity of Insurance Coverage

Executor's Role in Maintaining Coverage

Procedure for Contacting Insurance Provider After the Homeowner’s Death

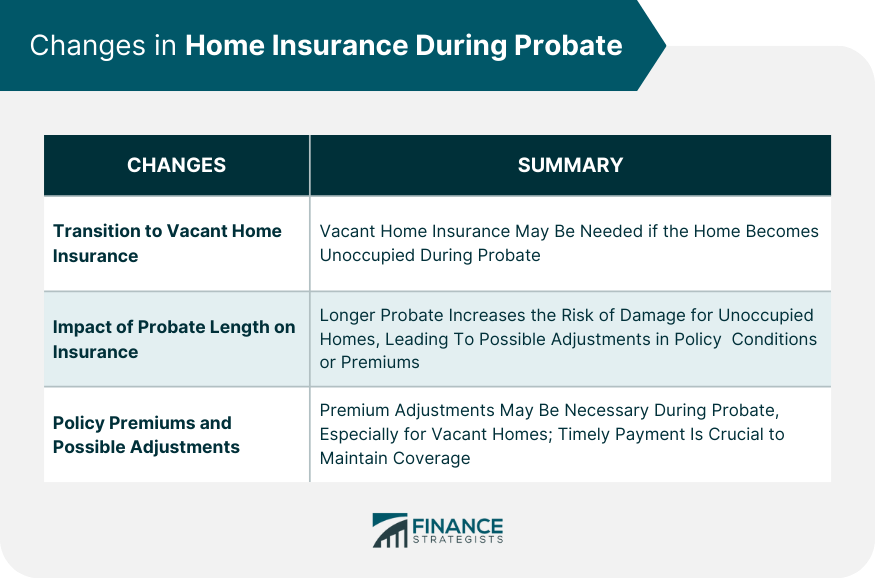

Changes in Home Insurance During Probate

Transition to Vacant Home Insurance

Impact of Probate Length on Insurance

Policy Premiums and Their Possible Adjustments

Complications and Legal Aspects of Home Insurance During Probate

Legal Responsibilities of the Executor Regarding Home Insurance

Fiduciary Duty

Possible Legal Consequences of Failing to Maintain Adequate Insurance

Challenges and Solutions When the Deceased's Insurance Lapses During Probate

Options for Obtaining Insurance Coverage

Probate Court Interventions

Handling Insurance Claims Made During the Probate Process

Procedure for Filing a Claim

Allocation of Insurance Proceeds

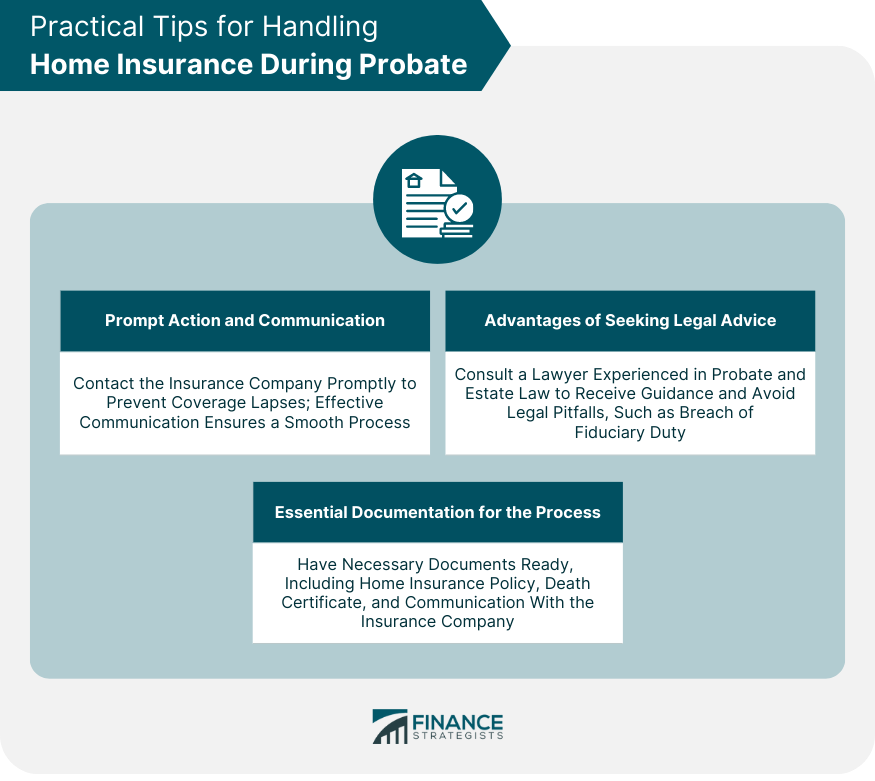

Practical Tips for Handling Home Insurance During Probate

Importance of Prompt Action and Communication

Advantages of Seeking Legal Advice

Essential Documentation for the Process

The Bottom Line

What Happens to Home Insurance During Probate? FAQs

Yes, it is crucial to maintain home insurance during probate to protect the estate from potential risks and fulfill the deceased's wishes regarding asset distribution.

The executor is responsible for ensuring that home insurance premiums are paid on time and for notifying the insurance company about the homeowner's death to keep the policy in effect.

Yes, it is important to promptly notify the insurance company about the homeowner's death to update them about the changed circumstances and to receive guidance on maintaining coverage during the probate process.

If the home becomes vacant during probate, it may be necessary to transition to vacant home insurance, as standard homeowners' insurance may not provide coverage for unoccupied properties beyond a certain period.

Yes, if the executor fails to maintain adequate insurance coverage and the home suffers damage or loss, beneficiaries could potentially sue the executor for breach of fiduciary duty. The executor might be personally liable to cover the loss, leading to significant legal and financial consequences.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.