UGMA accounts are custodial accounts established under the Uniform Gifts to Minors Act, allowing adults to transfer assets to minors without the need for a formal trust. UGMA accounts provide a simple and tax-efficient way to transfer assets to minors. The benefits of UGMA accounts include reduced gift tax implications, the ability to invest in various assets, and flexibility in using the funds for the minor's benefit. The UGMA is a set of laws that provide a legal framework for transferring assets to minors. Each state in the United States has adopted its version of the UGMA, with slight variations in the rules and regulations. UGMA accounts are governed by state law, and each state has its version of the UGMA. It is essential to familiarize yourself with the UGMA rules in your state to ensure compliance with the regulations governing these accounts. To establish an UGMA account, an adult (typically a parent or grandparent) opens the account as the custodian on behalf of the minor, known as the beneficiary. The custodian is responsible for managing the account until the minor reaches the age of majority, which varies by state. UGMA accounts can hold various assets, including cash, stocks, bonds, and mutual funds. Some states also allow other types of assets, such as real estate and collectibles, but this varies depending on the state's version of the UGMA. Contributions to UGMA accounts are irrevocable gifts to the minor and may be subject to federal gift tax if they exceed the annual exclusion limit. However, the donor can take advantage of the gift tax exclusion by contributing up to the limit each year. The custodian is responsible for managing the UGMA account on behalf of the minor. This includes making investment decisions, tracking account performance, and filing taxes for the account. The custodian has a fiduciary duty to act in the best interest of the minor. UGMA accounts offer a wide range of investment options, including stocks, bonds, and mutual funds. The custodian should choose investments that align with the minor's financial goals, time horizon, and risk tolerance. UGMA accounts are subject to taxation at the minor's tax rate. Investment income, such as interest, dividends, and capital gains, are taxed to the minor. However, a portion of the investment income may be tax-exempt or taxed at a lower rate, depending on the child's age and income level. Funds in an UGMA account can be used for any purpose that benefits the minor, such as education expenses, housing costs, or medical expenses. The custodian must ensure that withdrawals from the account are used for the minor's benefit. The custodian cannot withdraw funds from the UGMA account for their own use or benefit. Additionally, once the minor reaches the age of majority, they gain full control over the account, and the custodian can no longer make decisions or withdrawals on their behalf. When funds are withdrawn from an UGMA account, the minor may be subject to taxes on the investment income generated by the account. The tax consequences depend on the type of income, the minor's age, and their overall income level. UGMA accounts can affect a minor's eligibility for need-based financial aid, as they are considered an asset of the student when calculating the Expected Family Contribution (EFC). A higher EFC may result in reduced financial aid awards. To minimize the impact of UGMA accounts on financial aid eligibility, some families may choose to spend down the account on educational expenses before applying for financial aid or transfer the assets to a different savings vehicle, such as a 529 college savings plan. Uniform Transfers to Minors Act accounts are similar to UGMA accounts but allow for a broader range of assets to be held, including real estate and collectibles. UTMA accounts may be a suitable alternative for those looking to transfer non-financial assets to a minor. 529 college savings plans are tax-advantaged investment accounts specifically designed for education savings. Unlike UGMA accounts, 529 plans have no impact on financial aid eligibility and offer more significant tax benefits, making them an attractive alternative for college savings. Coverdell ESAs are another tax-advantaged savings vehicle for education expenses. While they have lower contribution limits than UGMA accounts and 529 plans, they can be used for both K-12 and college expenses, offering additional flexibility for families. UGMA accounts are custodial accounts that allow adults to transfer assets to minors for their benefit. They offer tax advantages, flexibility in investment options, and can be used for various purposes. However, UGMA accounts can impact financial aid eligibility, and there are alternative savings vehicles to consider based on the specific financial goals of the minor. Understanding UGMA accounts is essential for those looking to transfer assets to minors, as they offer a simple and tax-efficient way to save for a minor's future. Familiarizing yourself with the legal framework, management, and taxation of UGMA accounts can help ensure compliance and effective account management. Selecting the appropriate savings vehicle for a minor depends on the family's financial goals, risk tolerance, and preferences. By considering the various options, such as UGMA accounts, UTMA accounts, 529 plans, and Coverdell ESAs, families can make an informed decision about the best way to invest in a minor's financial future.What Are Uniform Gifts to Minors Act (UGMA) Accounts?

These accounts are used primarily for funding a minor's education, but the funds can also be used for any purpose that benefits the minor.Legal Framework of UGMA Accounts

Uniform Gifts to Minors Act

State Adoption and Variations

Establishing and Funding UGMA Accounts

Account Registration and Setup

Types of Assets Allowed

Contributions and Gift Tax Implications

UGMA Account Management

Role of the Custodian

Investment Options and Strategies

Taxation of UGMA Accounts

Withdrawals and Distributions From UGMA Accounts

Permissible Uses of Funds

Restrictions on Withdrawals

Tax Consequences of Distributions

UGMA Accounts and Financial Aid

Impact on Financial Aid Eligibility

Strategies to Minimize the Impact on Financial Aid

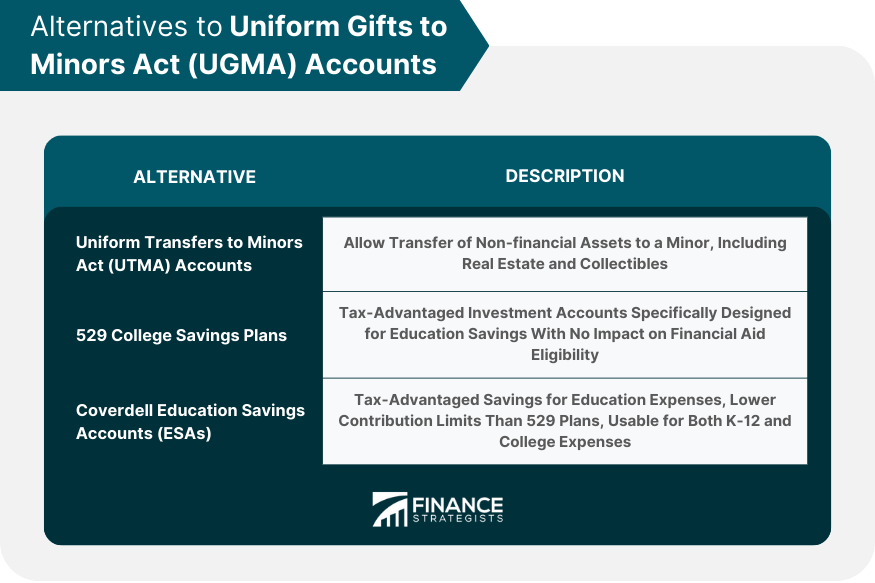

Alternatives to UGMA Accounts

Uniform Transfers to Minors Act (UTMA) Accounts

529 College Savings Plans

Coverdell Education Savings Accounts (ESAs)

Conclusion

Uniform Gifts to Minors Act (UGMA) Accounts FAQs

A UGMA account is a type of custodial account established under the Uniform Gifts to Minors Act, which allows a donor to make a gift of money or property to a minor. The account is managed by a custodian, who has legal control over the assets until the minor reaches the age of majority.

A UGMA account can hold a variety of assets, including cash, stocks, bonds, mutual funds, and other types of securities. The donor can make contributions to the account in any amount, up to the annual gift tax exclusion limit.

The income generated by a UGMA account is generally taxable to the minor, at their own tax rate. However, if the minor's income is below a certain threshold, they may be able to avoid paying taxes on their UGMA account income. In addition, the donor may be able to reduce their taxable estate by making gifts to a UGMA account.

When the minor reaches the age of majority, which is typically 18 or 21 depending on the state, they gain legal control over the UGMA account and its assets. The custodian is no longer involved in managing the account, and the minor can use the assets for any purpose.

Yes, a UGMA account can be used for college savings, but it may not be the most tax-efficient option. If the assets in the account are used for qualified education expenses, such as tuition, fees, and books, they can be withdrawn tax-free. However, any earnings on the account may be subject to taxes and penalties if they are not used for qualified education expenses. For this reason, a 529 college savings plan may be a better choice for college savings.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.