The Gordon Growth Model (GGM) is a financial valuation model used to estimate the intrinsic value of a stock. It is based on the premise that a company's value can be calculated by discounting its future dividends to the present value. The model is particularly useful for evaluating companies with stable dividend growth rates and is named after economist Myron J. Gordon, who developed the model in the 1960s. The Gordon Growth Model is an important tool in the field of finance because it provides a simple and straightforward way to estimate the value of a stock. By focusing on dividends and their growth, the model helps investors assess the company's ability to generate future cash flows. This information is crucial for long-term investors, as it allows them to identify stocks that may provide a stable and growing stream of income over time. Moreover, the GGM is widely used by analysts, portfolio managers, and other finance professionals to estimate the cost of equity capital. This is an essential input for the calculation of a firm's weighted average cost of capital (WACC), which is a crucial metric in determining the company's required rate of return on investments and evaluating potential projects. The Gordon Growth Model formula is relatively simple and can be calculated using the following equation: Value of Stock = D1 / (k - g) Where: D1 represents the expected annual dividend per share for the next year k is the required rate of return (discount rate) for the stock g is the constant growth rate of dividends By dividing the expected dividend per share by the difference between the required rate of return and the dividend growth rate, the GGM calculates the intrinsic value of a stock. The expected annual dividend (D1) represents the company's future cash flows to shareholders and is the primary source of value in the model. The required rate of return (k) reflects the investor's desired return on investment, taking into account the risk associated with the stock. A higher discount rate implies a higher required return, which will result in a lower stock value. The constant growth rate of dividends (g) is a critical assumption in the model. It represents the expected annual growth rate of the company's dividends and directly impacts the value of the stock. A higher growth rate implies greater future cash flows and will result in a higher stock value. Conversely, a lower growth rate will lead to a lower stock value. One key assumption of the Gordon Growth Model is that dividends will grow at a constant rate indefinitely. This means that the company is expected to maintain a consistent growth rate in its dividend payments, which may not always be realistic. Companies often experience fluctuations in their growth rates due to changes in market conditions, competition, and other factors. However, the constant growth rate assumption simplifies the valuation process and allows for easier comparisons between different companies. For the GGM to provide accurate estimates, it is best applied to companies with stable and predictable dividend growth rates, such as mature companies operating in non-cyclical industries. The Gordon Growth Model also assumes a constant discount rate, which represents the investor's required rate of return on the stock. This rate incorporates the time value of money and the perceived risk associated with the investment. The assumption of a constant discount rate simplifies the valuation process, but it may not accurately reflect changes in market conditions or investor risk preferences over time. In practice, the discount rate can be influenced by factors such as interest rate fluctuations, changes in the company's risk profile, and overall market volatility. When using the GGM, it is important for investors to consider the potential impact of these factors on their required rate of return and adjust the discount rate accordingly. Another assumption of the Gordon Growth Model is that the dividend payout ratio remains constant over time. The dividend payout ratio is the proportion of a company's earnings that is distributed to shareholders as dividends. This assumption implies that the company maintains a consistent dividend policy, which may not always be the case. Companies can change their dividend policies in response to changing business conditions or strategic priorities. For example, a company might choose to retain more earnings for reinvestment in growth opportunities or to reduce debt. As a result, the GGM may not accurately capture changes in a company's dividend payout ratio, which can impact the estimated stock value. One of the primary advantages of the Gordon Growth Model is its simplicity. With just three variables - expected dividend, required rate of return, and dividend growth rate - the GGM provides a straightforward method for estimating the intrinsic value of a stock. This simplicity makes the model accessible to a wide range of investors and finance professionals, even those with limited financial analysis experience. The Gordon Growth Model, when applied to appropriate companies, can provide a reasonable estimate of a stock's intrinsic value. By focusing on dividends and their growth, the model emphasizes the importance of a company's ability to generate future cash flows, which is a critical factor in determining its value. For companies with stable dividend growth rates, the GGM can be a useful tool in identifying potentially undervalued or overvalued stocks. The GGM is particularly well-suited for valuing companies with stable dividend growth rates. Mature companies operating in non-cyclical industries often exhibit consistent dividend growth and are more likely to meet the model's assumptions. In such cases, the GGM can provide a useful valuation estimate that helps investors make informed investment decisions. The accuracy of the Gordon Growth Model is highly dependent on the accuracy of its assumptions, particularly the dividend growth rate and the discount rate. Small changes in these assumptions can result in significant variations in the estimated stock value. As a result, investors must carefully consider the inputs used in the model and be aware of the potential impact of changes in these assumptions on their valuation estimates. The GGM does not account for external factors that can affect a company's growth rates, such as changes in market conditions, technological advancements, or regulatory shifts. These factors can have a significant impact on a company's ability to maintain stable dividend growth rates, and their omission from the model can lead to inaccurate valuation estimates. The Gordon Growth Model is a financial valuation tool that focuses on dividends and their growth rates to estimate the intrinsic value of a stock. By making key assumptions about constant dividend growth rates, discount rates, and dividend payout ratios, the model provides a straightforward method for evaluating stocks, particularly those of mature companies with stable growth rates. However, it is essential for investors to be aware of the model's limitations, such as its reliance on constant growth rates and its sensitivity to the assumptions made. The GGM may not be applicable to all companies, especially those with inconsistent or unpredictable dividend growth rates. Despite these limitations, the Gordon Growth Model remains a valuable tool in the field of finance, offering investors and finance professionals a simple and accessible method for estimating stock values. By carefully considering the model's assumptions and their potential impact on valuation estimates, investors can use the GGM to make more informed investment decisions and identify potential opportunities in the market.What Is the Gordon Growth Model?

The Formula of the Gordon Growth Model

Calculation of the Gordon Growth Model

Explanation of Each Variable in the Formula

Assumptions of the Gordon Growth Model

Constant Growth Rate Assumption

Discount Rate Assumption

Dividend Payout Ratio Assumption

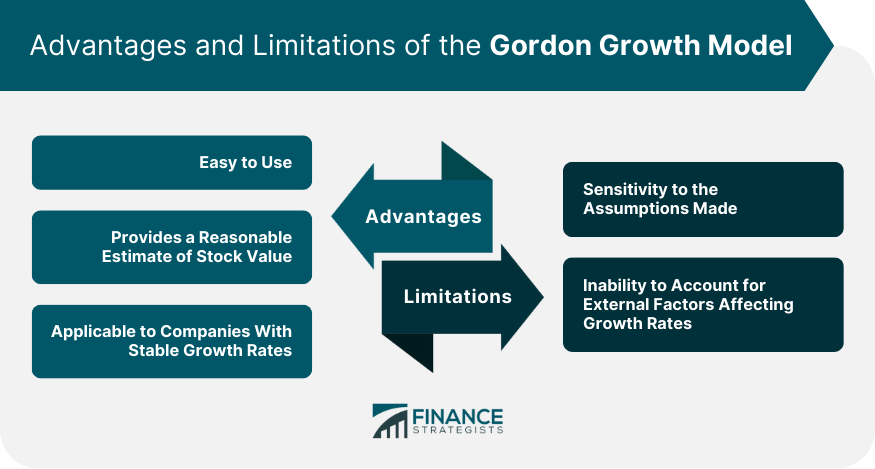

Advantages of the Gordon Growth Model

Easy to Use

Provides a Reasonable Estimate of Stock Value

Applicable to Companies With Stable Growth Rates

Limitations of the Gordon Growth Model

Sensitivity to the Assumptions Made

Inability to Account for External Factors Affecting Growth Rates

Final Thoughts

Gordon Growth Model FAQs

The Gordon growth model is a method used to estimate the intrinsic value of a stock based on its expected dividends and growth rate.

The model assumes a constant growth rate, a discount rate, and a stable dividend payout ratio.

It is easy to use, provides a reasonable estimate of stock value, and is applicable to companies with stable growth rates.

It is only applicable to companies with constant growth rates, is sensitive to the assumptions made, and cannot account for external factors affecting growth rates.

The model is calculated by dividing the expected dividend by the difference between the discount rate and the expected growth rate.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.