Retirement housing equity strategies involve utilizing the value of one's home to supplement retirement income, reduce financial stress, and maintain a comfortable lifestyle. Housing equity, which is the difference between the market value of a home and the outstanding mortgage balance, can play a significant role in retirement planning. Retirement housing equity strategies are options for retirees to use the equity in their homes as a source of income during their retirement years. There are several types of retirement housing equity strategies, each with its own features and benefits. The most common types of retirement housing equity strategies are as follows: A HELOC is a type of loan that uses the equity in your home as collateral. It works like a credit card, allowing you to borrow money up to a certain limit and pay interest only on the amount you borrow. HELOCs are often used for home improvements or to pay off other debts. This strategy can be considered when retirees need a source of income to supplement their retirement income, but want to retain ownership of their home. A reverse mortgage is a type of loan that allows retirees to convert the equity in their home into cash. Unlike a traditional mortgage, the borrower does not make payments on the loan. Instead, the loan is repaid when the borrower sells the home or passes away. This strategy can be considered when retirees need a source of income to supplement their retirement income and are willing to relinquish ownership of their home. A sale-leaseback is a transaction where the homeowner sells their home to an investor and then leases it back from them. This strategy can be considered when retirees want to access the equity in their home without having to move, but are willing to give up ownership of their home. Downsizing involves selling the current home and purchasing a smaller, less expensive one. This strategy can be considered when retirees want to access the equity in their home, but also want to reduce their housing expenses. Downsizing can also be a good option for retirees who want to move to a different location or community. Renting involves selling the current home and renting a more affordable one. This strategy can be considered when retirees want to access the equity in their home, but do not want the responsibilities and expenses of homeownership. Renting can also be a good option for retirees who want to travel or live in different locations during their retirement years. When selling a primary residence, homeowners may be subject to capital gains tax on the profit made from the sale. However, there is an exclusion for qualifying individuals, allowing them to exclude up to $250,000 ($500,000 for married couples filing jointly) of the gains from their taxable income. The mortgage interest paid on a primary residence may be tax-deductible, subject to specific limitations and requirements. Retirees should consult a tax professional to understand how their chosen housing equity strategy may affect their mortgage interest deduction. Reverse mortgage payments are generally tax-free, as they are considered loan proceeds rather than income. However, interest accrued on the loan balance is not tax-deductible until it is paid. For HELOCs, interest may be tax-deductible if the loan is used for qualified purposes, such as home improvements. It is essential to consult a tax professional for guidance on the tax implications of these strategies. Before retirement, individuals should focus on building home equity by paying down their mortgage, maintaining and improving their property, and monitoring local real estate market trends. Strategies to reduce mortgage debt before retirement include making extra principal payments, refinancing to a lower interest rate or shorter loan term, and avoiding taking on additional debt secured by the home. Pre-retirees should assess their future housing needs, considering factors such as location, accessibility, and long-term care requirements. This assessment will help inform their choice of retirement housing equity strategy. In early retirement, individuals should implement their chosen housing equity strategy, whether it be downsizing, obtaining a reverse mortgage, or utilizing a HELOC or HECM for Purchase. Early retirees should review and adjust their investment portfolios to align with their housing equity strategy and overall retirement income plan. It is crucial for retirees to monitor their cash flow and expenses regularly, ensuring they are living within their means and making any necessary adjustments to their housing equity strategy. In late retirement, individuals may need to reevaluate their housing equity strategy to accommodate changes in health, family dynamics, or financial circumstances. Retirees should consider how their housing equity strategy may impact their ability to fund long-term care, whether at home or in a care facility. It is essential to incorporate one's housing equity strategy into estate planning, ensuring that heirs and beneficiaries are informed of the potential implications of the chosen strategy. Each individual's financial situation, including income sources, debt levels, and investment portfolio, will play a significant role in determining the most appropriate housing equity strategy. Retirees should consider their desired lifestyle, including travel, hobbies, and social activities when selecting a housing equity strategy that supports their goals. Real estate market trends, interest rates, and economic conditions can impact the effectiveness and viability of different housing equity strategies. It is essential to monitor these factors and adjust plans accordingly. The tax consequences of various housing equity strategies may differ significantly. Consultation with a tax professional can help retirees choose a strategy that minimizes their tax liability while maximizing their retirement income. Family considerations, such as multigenerational living arrangements, caregiving responsibilities, and estate planning goals, should be taken into account when selecting a retirement housing equity strategy. Retirees have several options for utilizing their home equity as a source of income during their retirement years. Choosing the right strategy depends on individual financial situations, retirement goals, and personal preferences. HELOCs, reverse mortgages, sale-leasebacks, downsizing, and renting are among the most common types of retirement housing equity strategies, each with its own benefits and tax implications. Pre-retirement planning, implementing chosen strategies in early retirement, and reevaluating strategies in late retirement are crucial steps in maximizing retirement income and managing long-term care needs. It is important to consult with a tax professional and financial advisor to make informed decisions about retirement housing equity strategies that best suit individual needs. With careful planning and professional guidance, retirees can effectively utilize their home equity to maintain a comfortable and secure retirement lifestyle.Retirement Housing Equity Strategies Overview

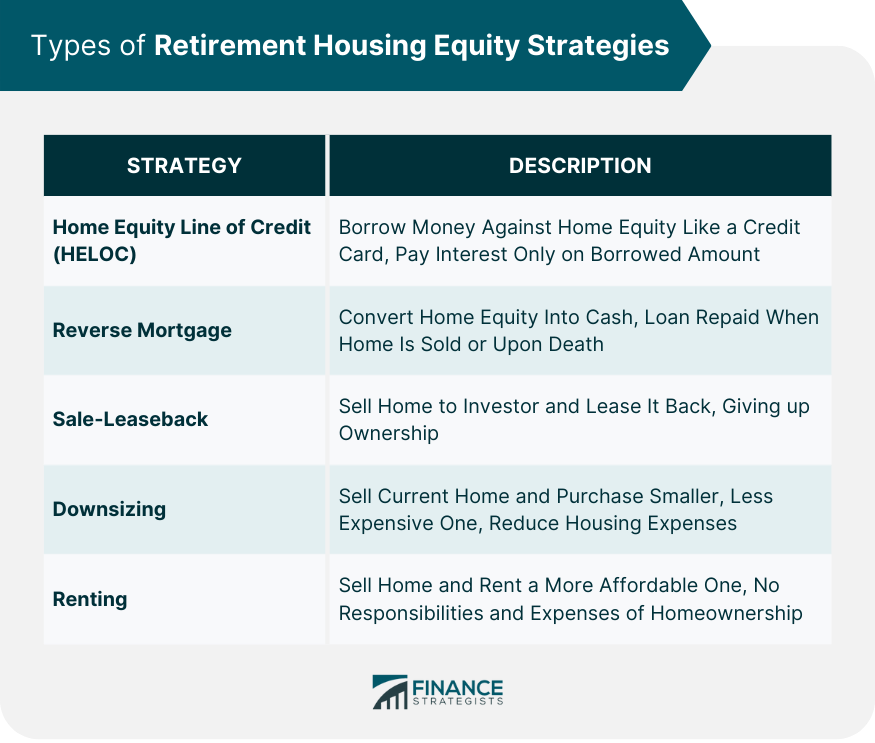

Types of Retirement Housing Equity Strategies

Home Equity Line of Credit (HELOC)

Reverse Mortgage

Sale-Leaseback

Downsizing

Renting

Tax Implications of Retirement Housing Equity Strategies

Capital Gains Tax on Selling a Home

Tax Deductions for Mortgage Interest

Tax Implications of Reverse Mortgages and HELOCs

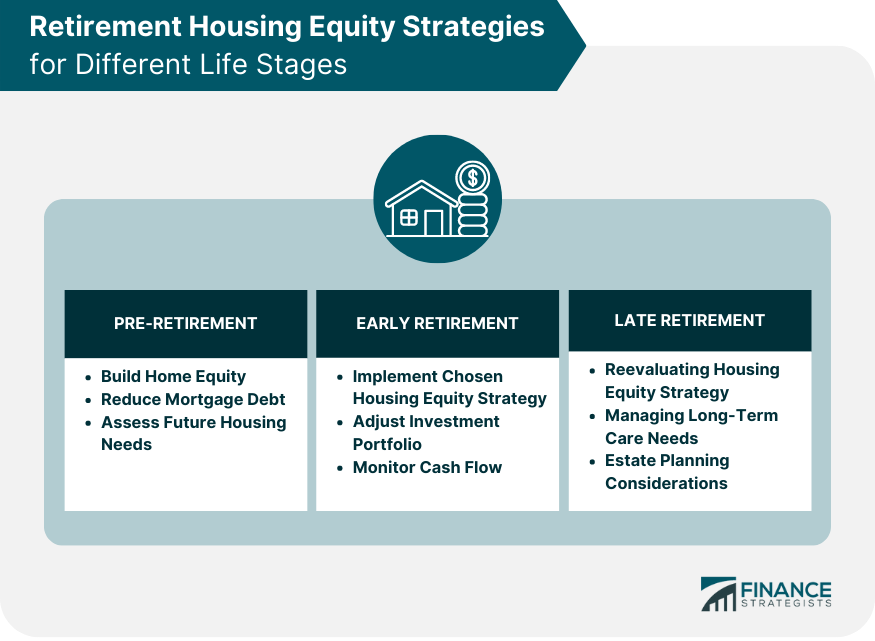

Retirement Housing Equity Strategies for Different Life Stages

Pre-retirement Planning

Building Home Equity

Reducing Mortgage Debt

Assessing Future Housing Needs

Early Retirement

Implementing Chosen Housing Equity Strategy

Adjusting Investment Portfolio

Monitoring Cash Flow and Expenses

Late Retirement

Reevaluating Housing Equity Strategy

Managing Long-Term Care Needs

Estate Planning Considerations

Factors to Consider When Choosing a Retirement Housing Equity Strategy

Personal Financial Situation

Retirement Goals and Lifestyle Preferences

Market Conditions

Tax Implications

Family Dynamics

Conclusion

Retirement Housing Equity Strategies FAQs

The main types of retirement housing equity strategies include downsizing, reverse mortgages, home equity lines of credit (HELOCs), and home equity conversion mortgages for purchase (HECMs). Each strategy has its advantages and disadvantages, so it's essential to choose the one that best aligns with your financial goals and lifestyle preferences.

Retirement housing equity strategies can have various tax implications, depending on the chosen strategy. For example, downsizing may involve capital gains tax on the profit from selling your home, while reverse mortgage payments are generally tax-free. It's important to consult with a tax professional to understand how your chosen strategy may affect your tax situation.

Yes, it's possible to combine different retirement housing equity strategies to achieve your financial goals. For example, you might downsize to a smaller home and use a reverse mortgage or HELOC to access additional funds. However, it's essential to carefully consider the benefits and risks associated with each strategy and consult with a financial advisor to ensure your approach is well-suited to your specific needs.

Choosing the best retirement housing equity strategy involves considering factors such as your personal financial situation, retirement goals, lifestyle preferences, market conditions, and tax implications. It's crucial to research each strategy thoroughly, evaluate its potential benefits and risks, and consult with financial and tax professionals to make an informed decision.

It's essential to review your retirement housing equity strategy regularly and make adjustments as needed based on changes in your financial circumstances, health, family dynamics, and market conditions. Some common reasons to reevaluate your strategy include changes in your income or expenses, shifting real estate market trends, or new tax laws that may affect your chosen strategy. Consulting with a financial advisor can help you determine whether it's time to reassess and make any necessary changes.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.