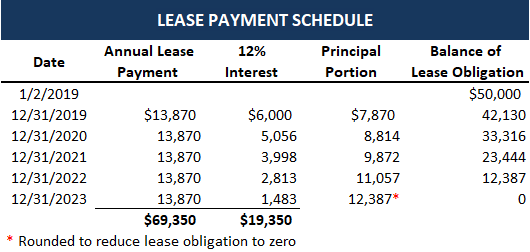

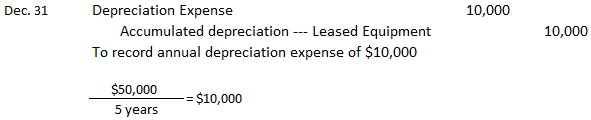

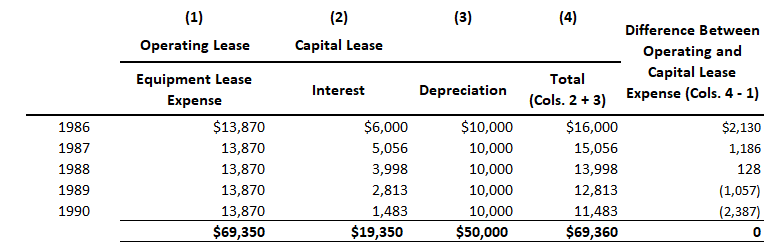

A lease is a contractual agreement between the lessor (the owner of the property) and the lessee (the user of the property). It gives the lessee the right to use the lessor's property for a specific period of time in exchange for stipulated cash payments. Accounting for leases has long been a controversial subject. The basic controversy centers on the classification and accounting for capital leases in terms of whether they are essentially equivalent to installment purchases. From the lessee's point of view, there are two types of leases: operating leases and capital leases. The distinction between these types of leases is important because a different accounting treatment is required for each. Thus, there are substantial effects on the balance sheet and income statement depending on whether a lease is classified as a capital lease or an operating lease. According to FASB Statement No. 13, Accounting for Leases, a lease should be classified as a capital lease if it meets one or more of the following criteria: Thus, capital leases are accounted for essentially as purchases of equipment or other property. A lease rather than a bank loan is used to finance the purchase. As we will see, accounting for these types of leases requires that the asset and the liability be recorded on the lessee's books just as if a purchase had taken place. A lease that does not meet any of the above criteria is considered an operating lease. With this type of lease, the lessor retains control and ownership of the property, which reverts back to the lessor at the end 0f the lease term. Accounting for this type of lease requires only that the lessee record an expense for the periodic lease payments as they are made. You should keep in mind that these two types of leases are not alternatives for the same transaction. If the terms of the lease agreement meet any of the above-mentioned four criteria, the lease must be accounted for as a capital lease. To demonstrate the process of accounting for leases, suppose that on 2 January 2019, Scully Corporation enters into a lease with Porter Company. Scully Corporation agrees to lease a piece of equipment for 5 equal annual payments of $13,850. Each payment is made at year-end. Note that most payments are made monthly, but we assume annual payments here for ease of illustration. To compare and contrast the accounting treatment for operating and capital leases, we will use this data to demonstrate the accounting procedures for each type of lease. This is for illustrative purposes only, however, because the lease must be considered either a capital lease or an operating lease. Assuming this agreement is an operating lease, Scully Corporation does not make any entry on 2 January 2019 when the lease agreement is signed. At this point, the lease is considered just an agreement or contract that neither party has yet carried out. Scully Corporation makes the following entry on 31 December of each of the next 5 years: The entire lease payment is shown as an expense. The equipment is still on the books of the lessor and is depreciated by the lessor. Over the 5-year lease term, Scully Corporation incurs total lease expenses of $69,350 (or $13,870 x 5 years). Under a capital lease, Scully Corporation actually records the equipment as an asset and the required lease payments as a liability. The asset and liability are recorded at the present value of the required lease payments by using an appropriate interest rate, which we will assume is 12% for this lease. Subsequently, Scully Corporation makes yearly payments that are divided between principal and interest, and it also depreciates the equipment. In a corresponding manner, the lessor takes the leased equipment off their books and records a receivable at the present value of the lease payments. The present value of the lease payments of $13,870 based on an interest rate of 12% is $50,000. This is determined by discounting the annuity of $13,870 for 5 years at 12%. Based on these data, Scully Corporation makes the following entry on 2 January 2019, the inception of the lease: The account entitled Leased Equipment Under Capital Lease is a non-current asset, which is generally shown under the property, plant, and equipment section. The account entitled Obligation Under Capital Lease is a liability, of which part is classified as current and part as long term. At the end of each year, Scully Corporation makes a $13,870 annual payment. The following table shows how these payments are divided between interest and principal: The interest each year is based on 12% of the balance of the lease obligation at the beginning of the year. Thus, in 2019, interest is $6,000, or 12% of $50,000, and in 2020, it is $5,056, or 12% of $42,130. The difference between the annual lease payment and the interest portion is the principal portion. The entry to record the first payment is: Scully Corporation needs to make one additional entry each year to record the depreciation expense on the leased equipment. The leased equipment is depreciated over its life of 5 years using straight-line depreciation and no salvage value. Thus, Scully Corporation makes the following adjusting entry at the end of each year: The following table shows the difference between accounting for Scully Corporation's lease as an operating lease or as a capital lease. Over the entire 5-year period, the total expense in both cases is $69,350, which represents the total cash outflows. However, each method results in a different expense pattern within a 5-year period of time. In the first 3 years, the capital lease method results in a higher annual expense than the operating lease method. This means that annual net income is lower in these years. This pattern then reverses in the last two years of the lease term. These relationships lie at the heart of the controversy over the process of accounting for leases. Prior to the issuance of Statement 13, companies had a good deal of latitude in deciding whether a lease should be classified as an operating or a capital lease. Most companies felt it was in their best interest to classify most leases as operating leases. Some obvious purchases that were being financed through leases were considered operating leases when they should have been considered capital leases. If a lease is considered an operating lease, no liability is recorded on the balance sheet for the required lease payments. This means that the lessee's working capital position or current ratio is not affected by the lease agreement. Remember that if a liability is recorded on a balance sheet, the next year's payment must be considered a current liability. The entire balance in the account entitled Leased Equipment Under Capital Lease is considered a non-current asset. The fact that the lessee was effectively making an installment purchase, but did not have to record the asset or liability on the balance sheet, is referred to as off-balance sheet financing. Off-balance sheet financing also has a tendency to decrease a firm's debt-to-equity ratio and to increase its return on investment. Furthermore, the annual expense associated with an operating lease is less in the first few years of the lease term compared to a capital lease. Due to these factors, as well as the fear that creditors might react adversely if leases are capitalized on the balance sheet, some managers have a definite bias toward classifying leases as operating leases. The criteria set forth in the FASB Statement No. 13 corrected a number of obvious situations in which agreements that were in substance capital leases were being accounted for as operating leases. The four criteria in Statement 13 ensure that leases that are in fact installment purchases are recorded as capital leases. Thus, the appropriate asset and liability, interest expense, and depreciation are recorded. In addition, current accounting rules require substantial footnote disclosure concerning lease terms and agreements.Lease: Definition

Types of Leases

Accounting for Leases

Accounting for Operating Leases

Accounting for Capital Leases

Operating vs. Capital Leases

Accounting for Leases FAQs

An operating lease is generally for items such as vehicles, computers, etc., i.e., items that are consumed over time whereas under a finance lease capital assets are leased to facilitate Cash Flow purposes.

There are four criteria that determine whether a transaction should be classified as an operating lease or a finance lease. These criteria are: (1) the term of the agreement, (2) the value of the asset, (3) ownership transferral, and (4) residual value risk.

The term should take into account any options to extend or terminate the agreement that are reasonably assured of being exercised. If less than 75% of the total life expectancy of the asset is covered by the lease term, then it is presumed that ownership transferral has taken place and the lease should be considered a finance lease.

The value of the asset should not be based on its purchase price or original cost but rather on its current fair market value. If less than 75% of the total life expectancy of the asset is covered by the agreement, then it is presumed that ownership transferral has taken place and the lease should be considered a finance lease.

Ownership transferral is presumed to have occurred if at least one of the following conditions exists: (1) The lessee has title to the asset, (2) the lessee has the right to buy the asset, (3) the lessee has the right to sell or use the asset, or (4) if there are no reasonable assurances that the lessee will continue paying rent throughout the life of the agreement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.