Spread duration is a measure used in fixed-income investing to estimate the sensitivity of a bond's price to changes in its credit spread. This measure reflects the potential change in the bond's value in response to a 100 basis point (1%) change in the credit spread, helping investors understand the associated risks. Spread duration plays a crucial role in fixed-income investing as it helps investors gauge the impact of credit spread changes on their bond portfolios. By understanding this sensitivity, investors can make better-informed decisions, manage risks more effectively, and potentially enhance their portfolio returns. The key components of spread duration include yield to maturity (YTM), option-adjusted spread (OAS), and modified duration. These components are essential in determining the spread duration and help investors assess the potential changes in bond prices resulting from fluctuations in credit spreads. Yield to maturity is the total return anticipated on a bond if it is held until maturity. YTM is a crucial component in the calculation of spread duration as it provides a benchmark for comparing the bond's yield with those of other fixed-income securities, ultimately helping to determine the bond's sensitivity to credit spread changes. Option-adjusted spread is a measure of the yield spread between a fixed-income security and a risk-free rate, adjusted for embedded options such as call or put provisions. OAS is used in spread duration calculations to estimate the bond's risk premium and sensitivity to changes in credit spreads while accounting for the potential impact of embedded options. Modified duration is a measure of a bond's price sensitivity to changes in interest rates. It is an essential component in calculating spread duration, as it helps investors estimate the bond's price volatility in response to changes in credit spreads, allowing them to assess and manage interest rate risk. The formula for spread duration is derived by dividing the bond's option-adjusted spread (OAS) by its yield to maturity (YTM) and then multiplying the result by the bond's modified duration. This calculation provides a measure of the bond's price sensitivity to changes in credit spreads, helping investors assess the potential impact of spread fluctuations on their portfolios. Spread duration is used in portfolio management for risk assessment by estimating the potential impact of credit spread changes on bond prices. Understanding this sensitivity enables investors to make informed decisions and manage credit risk more effectively, thus optimizing their fixed income portfolios. Measuring portfolio performance is another application of spread duration in portfolio management. By comparing the spread duration of individual bonds or portfolios, investors can assess their relative performance, identify potential opportunities, and make adjustments to enhance their returns. Spread duration aids in asset allocation by helping investors determine the optimal mix of fixed income securities to include in their portfolios. Investors can balance the trade-offs between risk and return by considering spread duration, diversifying their holdings and minimizing potential losses due to credit spread fluctuations. Relative value analysis is a trading strategy that utilizes spread duration to compare the attractiveness of different fixed income securities. By examining the spread duration of various bonds, investors can identify potential mispricings and capitalize on these opportunities to generate profits. Spread trades involve taking long and short positions in bonds with different credit spreads. Spread duration plays a key role in designing these trades, as it helps investors assess the potential price movements of the bonds in response to spread changes, thus allowing them to make informed decisions about which bonds to include in their spread trade strategy. Yield curve strategies involve taking positions in bonds with different maturities to capitalize on anticipated changes in the yield curve. Spread duration helps investors implement these strategies by assessing the potential price movements of bonds in response to credit spread changes, enabling them to optimize their positions and maximize returns. Hedging fixed income exposures involves managing interest rate risk to minimize potential losses. Spread duration is an essential tool in interest rate risk management, as it helps investors estimate the bond's price sensitivity to credit spread changes and implement hedging strategies using derivatives, such as interest rate swaps or futures. Credit risk management refers to the process of mitigating the potential losses resulting from an issuer's default or credit rating downgrade. Spread duration is valuable in credit risk management, as it allows investors to assess the impact of credit spread changes on their bond portfolios and employ appropriate hedging strategies, like credit default swaps or options. As reflected in an issuer's credit rating, credit quality influences spread duration. Generally, bonds with lower credit ratings exhibit higher spread durations, as investors demand higher yields to compensate for the increased risk, leading to greater price sensitivity to credit spread changes. The interest rate environment plays a significant role in determining spread duration. In a low-interest-rate environment, the spread duration tends to be higher as the yield spread becomes a more significant component of the bond's total return, leading to increased price sensitivity to credit spread changes. Liquidity conditions in the fixed income market can affect spread duration. When liquidity is low, bid-ask spreads may widen, resulting in higher spread durations. Conversely, spread durations may decrease in a more liquid market due to tighter bid-ask spreads and more efficient pricing. Economic conditions can influence spread duration by affecting credit spreads and investor sentiment. During economic downturns, credit spreads may widen as default risk increases, leading to higher spread durations. In contrast, during periods of economic growth, credit spreads may narrow, and spread durations may decline. Issuer-specific factors, such as financial performance, industry trends, and management quality, can also impact spread duration. Positive developments for an issuer may reduce credit spreads and lower spread durations, while negative developments can result in wider spreads and increased spread durations. Modified duration measures a bond's price sensitivity to interest rate changes, providing insights into interest rate risk. While spread duration focuses on the bond's sensitivity to credit spread changes, modified duration is more concerned with the overall impact of interest rate movements on bond prices. Effective duration accounts for the bond's price sensitivity to interest rate changes, considering embedded options such as call or put provisions. Unlike spread duration, which isolates the impact of credit spread changes, effective duration provides a more comprehensive measure of interest rate risk, including the effects of embedded options. Macaulay duration measures the weighted average time until a bond's cash flows are received, expressed in years. While spread duration and other duration metrics assess price sensitivity to various factors, Macaulay duration is primarily used for portfolio immunization and bond duration matching strategies. Each duration metric has specific use cases, depending on the investor's objectives and the characteristics of the bond or portfolio. Spread duration is ideal for analyzing credit risk, modified duration for assessing interest rate risk, effective duration for evaluating interest rate risk with embedded options, and Macaulay duration for implementing immunization and bond duration matching strategies. Investors should select the appropriate metric based on their specific needs and risk management goals. Spread duration relies on certain assumptions and simplifications, such as constant yield curve shifts and parallel credit spread changes, which may not always hold true in real-world market conditions. These assumptions can limit the accuracy of spread duration as a risk management tool and potentially lead to imprecise assessments of price sensitivity. Spread duration may not accurately predict price changes in response to credit spread movements due to factors such as non-linear price behavior, optionality, or the impact of liquidity conditions. As a result, investors should be cautious when relying solely on spread duration to anticipate bond price changes and manage risks. There may be a non-linear relationship between credit spread changes and bond prices, particularly for bonds with embedded options or bonds trading at significant premiums or discounts. This non-linearity can limit the usefulness of spread duration as a measure of price sensitivity and make it difficult to predict the exact impact of spread changes on bond prices. Spread duration is an essential tool for fixed-income investors, as it allows them to assess the sensitivity of bond prices to changes in credit spreads. Understanding spread duration can help investors make more informed decisions, manage risks, and potentially enhance portfolio returns. Despite its usefulness, spread duration has some limitations and challenges, including assumptions and simplifications, inaccuracies in predicting price changes, and non-linear relationships between spread changes and bond prices. To overcome the limitations of spread duration, investors should combine it with other risk measures, such as modified duration, effective duration, and credit ratings. Given the complexity of fixed-income investing and the limitations of individual risk measures like spread duration, investors may benefit from seeking professional wealth management services. What Is Spread Duration?

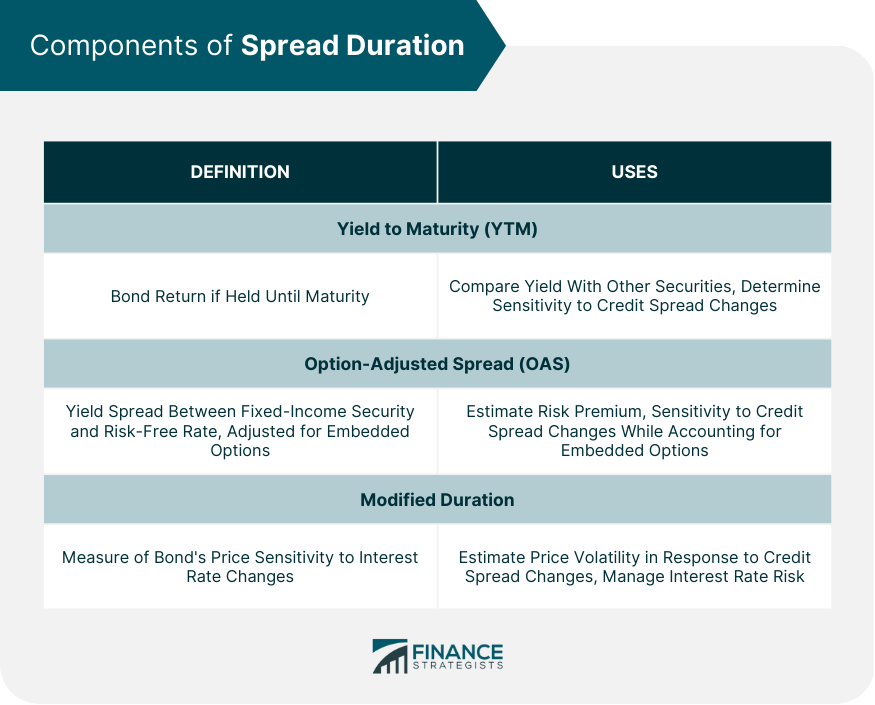

Components of Spread Duration

Yield to Maturity (YTM)

Option-Adjusted Spread (OAS)

Modified Duration

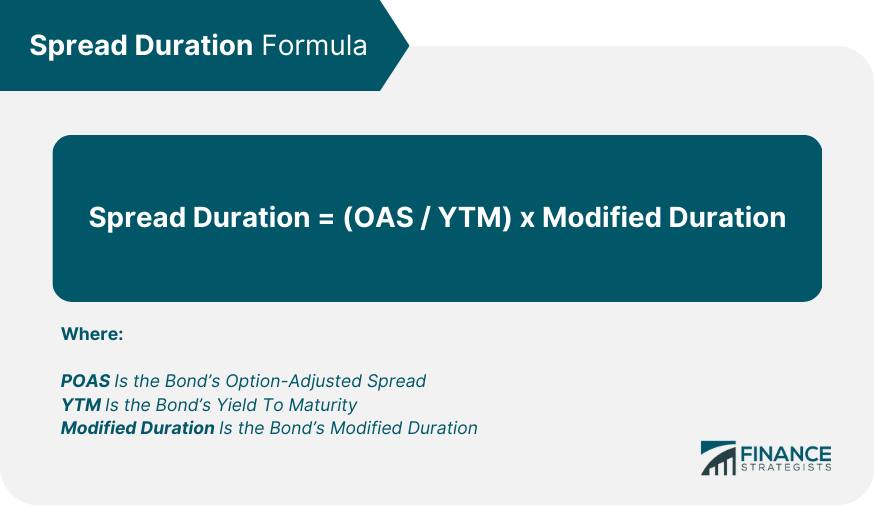

Formula for Spread Duration

Applications of Spread Duration

Portfolio Management

Risk Assessment

Performance Measurement

Asset Allocation

Trading Strategies

Relative Value Analysis

Spread Trades

Yield Curve Strategies

Hedging Fixed Income Exposures

Interest Rate Risk Management

Credit Risk Management

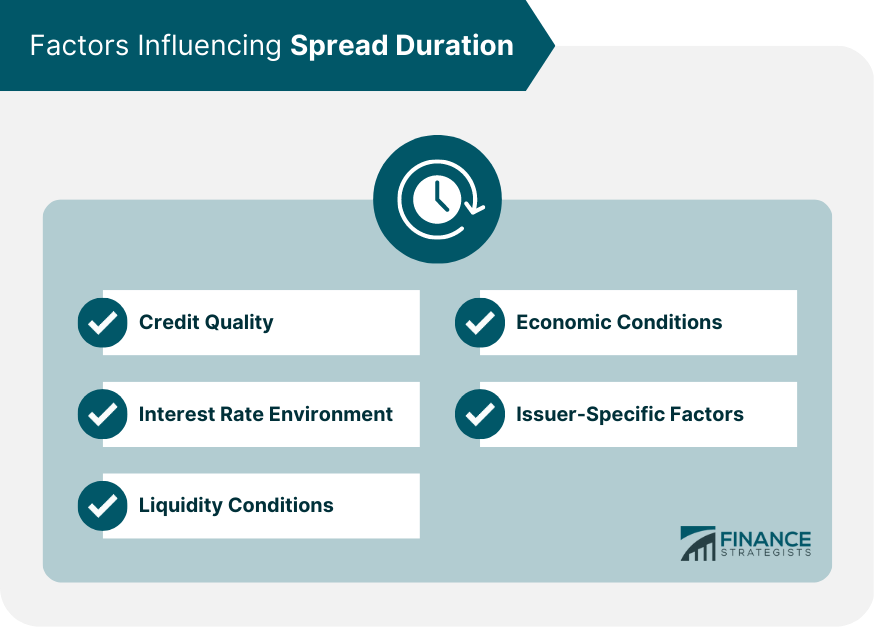

Factors Influencing Spread Duration

Credit Quality

Interest Rate Environment

Liquidity Conditions

Economic Conditions

Issuer-Specific Factors

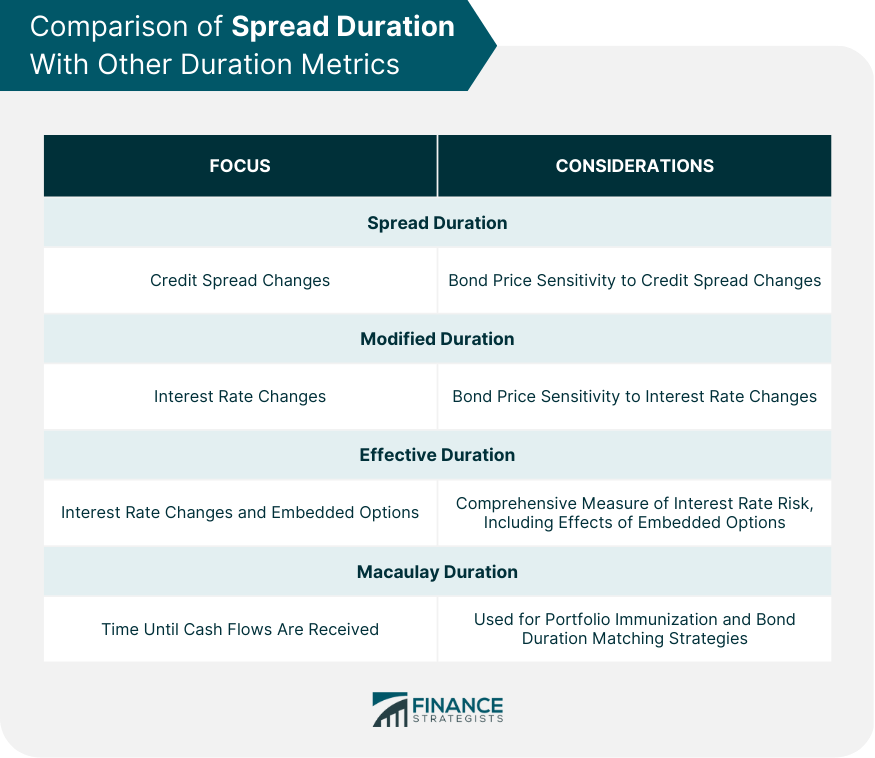

Spread Duration and Other Duration Metrics

Comparison of Spread Duration With Other Duration Metrics

Modified Duration

Effective Duration

Macaulay Duration

Appropriate Use Cases for Each Duration Metric

Limitations of Spread Duration

Assumptions and Simplifications

Inaccuracies in Predicting Price Changes

Non-linear Relationship Between Spread Changes and Bond Prices

Final Thoughts

Spread Duration FAQs

Spread duration is a measure of a bond's price sensitivity to changes in its credit spread. It helps fixed income investors understand the potential impact of credit spread fluctuations on their bond portfolios, enabling them to make better-informed decisions, manage risks effectively, and potentially enhance returns.

Spread duration is calculated by dividing a bond's option-adjusted spread (OAS) by its yield to maturity (YTM) and then multiplying the result by the bond's modified duration. This calculation provides a measure of the bond's price sensitivity to changes in credit spreads, helping investors assess the potential impact of spread fluctuations on their portfolios.

Spread duration can be used in various trading strategies, such as relative value analysis, spread trades, and yield curve strategies. In portfolio management, it assists in risk assessment, performance measurement, and asset allocation by helping investors understand the impact of credit spread changes on bond prices and optimize their fixed income portfolios.

The main factors influencing spread duration include credit quality, interest rate environment, liquidity conditions, economic conditions, and issuer-specific factors. These factors can affect credit spreads and, consequently, the sensitivity of bond prices to credit spread changes.

Spread duration focuses on a bond's price sensitivity to credit spread changes, while modified duration measures price sensitivity to interest rate changes. Effective duration accounts for price sensitivity to interest rate changes, considering embedded options, and Macaulay duration measures the weighted average time until a bond's cash flows are received. Each metric serves different purposes and helps investors assess various aspects of fixed income investment risks.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.