Bond valuation is the process of determining the fair value or theoretical price of a bond. This involves calculating the present value of the bond's future cash flows, which include periodic interest payments and the face value returned upon maturity. Bond valuation is crucial for investors as it allows them to assess the attractiveness of a bond relative to its market price. By comparing the bond's intrinsic value to its current price, investors can determine if the bond is overpriced, fairly priced, or undervalued, ultimately guiding their investment decisions. A bond is a debt instrument issued by entities, such as governments and corporations, to raise capital. It represents a loan made by an investor to the issuer, with the issuer promising to pay periodic interest and return the principal amount at maturity. Government bonds are issued by national governments to finance public projects and manage debt. They are considered low-risk investments due to the creditworthiness of the issuing government and are often used as benchmarks for interest rates. Corporate bonds are debt securities issued by companies to fund operations, acquisitions, or other business initiatives. They typically offer higher yields than government bonds to compensate for the additional credit risk associated with investing in a corporation. Municipal bonds are debt securities issued by local governments or their agencies to finance public projects, such as infrastructure or schools. They often provide tax advantages to investors, as interest income may be exempt from certain taxes. The face value, or par value, of a bond, is the amount that the issuer will repay the bondholder at maturity. It is the principal amount on which the periodic interest payments are calculated. The coupon rate is the annual interest rate paid on a bond, expressed as a percentage of the bond's face value. This rate determines the periodic interest payments made to the bondholder throughout the life of the bond. The maturity date is the date when the bond's principal amount is due to be repaid to the bondholder. Bonds can have short-term, medium-term, or long-term maturities, typically ranging from a few months to 30 years or more. The issuer's credit rating is an assessment of the issuer's creditworthiness and likelihood of defaulting on its debt obligations. Credit rating agencies, such as Standard & Poor's, Moody's, and Fitch, assign ratings based on their evaluation of the issuer's financial strength and stability. Present value is the concept of determining the value of future cash flows in today's terms. Discounting is the process of converting future cash flows to their present value by applying a discount rate, which accounts for the time value of money and the inherent risk associated with the cash flows. Yield to maturity (YTM) is the total return an investor can expect to receive if a bond is held until its maturity date. It takes into account the bond's current market price, face value, coupon rate, and time to maturity. YTM is a widely used metric for bond valuation and comparison. Duration is a measure of a bond's price sensitivity to changes in interest rates. It estimates the weighted average time until the bond's cash flows are received. Modified duration adjusts the duration to account for the bond's price change due to a one percent change in yield, making it a useful risk management tool. Convexity is a measure of the curvature of a bond's price-yield relationship, providing an estimate of how the bond's price will change as interest rates move. A higher convexity indicates greater price changes for a given change in interest rates, making it an essential tool for managing interest rate risk in a bond portfolio. The discounted cash flow (DCF) method is a widely-used bond valuation technique that calculates the present value of the bond's future cash flows, including coupon payments and principal repayment. By discounting these cash flows at an appropriate discount rate, the DCF method estimates the bond's intrinsic value, helping investors identify potential investment opportunities. The yield-to-maturity (YTM) method is another popular bond valuation approach that computes the total return an investor can expect to receive if a bond is held to maturity. This method considers the bond's current market price, face value, coupon rate, and time to maturity, allowing investors to compare bonds with different characteristics. Credit spread analysis involves comparing the yield of a bond to that of a benchmark bond, typically a government bond with a similar maturity. The difference in yields, known as the credit spread, reflects the additional risk associated with the bond being analyzed. A wider credit spread may signal a higher risk, while a narrower spread indicates lower risk. Bond benchmarking is the process of comparing a bond's performance and characteristics to those of a reference bond or a group of bonds with similar features. This method helps investors gauge the relative value of a bond, identify market trends, and make informed investment decisions. Callable bonds grant the issuer the right to redeem the bond before its maturity date, while puttable bonds allow the bondholder to sell the bond back to the issuer before maturity. These embedded options can affect a bond's valuation, as they influence the expected cash flows and risk profile of the investment. The option-adjusted spread (OAS) method accounts for the impact of embedded options on a bond's valuation. By adjusting the bond's yield spread for the value of these options, the OAS method provides a more accurate measure of the bond's risk and return, enabling investors to make better comparisons among bonds with different features. Interest rate fluctuations directly impact bond prices, as they influence the discount rate used in bond valuation. When interest rates rise, bond prices tend to fall, and vice versa. Investors must monitor interest rate movements to adjust their bond investment strategies accordingly. Inflation expectations can affect bond valuation, as they influence the real return on investment. Higher inflation expectations may lead to higher interest rates and lower bond prices, while lower inflation expectations can result in lower interest rates and higher bond prices. Credit rating changes can significantly impact a bond's valuation, as they alter the perceived risk associated with the investment. An upgrade in credit rating may result in a narrower credit spread and higher bond prices, whereas a downgrade can lead to a wider credit spread and lower bond prices. Economic conditions, including GDP growth, employment, and consumer sentiment, can influence bond valuation by affecting interest rates, inflation expectations, and credit risk. A strong economy may lead to higher interest rates and lower bond prices, while a weaker economy can result in lower interest rates and higher bond prices. Market liquidity refers to the ease with which a bond can be bought or sold in the market without affecting its price. A liquid bond market generally leads to more accurate bond valuations and narrower bid-ask spreads, while an illiquid market can result in wider spreads and greater price volatility, potentially affecting the bond's perceived value. The financial health of the bond issuer plays a critical role in bond valuation, as it directly impacts the issuer's creditworthiness and ability to meet its debt obligations. Strong financial performance and low debt levels can lead to higher bond prices, while financial distress or high debt levels can result in lower bond prices. Bond valuation is essential in achieving portfolio diversification, as it enables investors to identify undervalued or overvalued bonds and select investments with varying risk and return profiles. By including bonds with different characteristics in their portfolios, investors can spread risk and enhance overall portfolio performance. Accurate bond valuation allows investors to better manage risk by understanding the potential impact of interest rate changes, credit rating fluctuations, and other factors on their bond investments. By assessing these risks, investors can adjust their portfolios to minimize potential losses and optimize returns. Bond valuation helps investors identify income-generating opportunities in the fixed-income market. By selecting bonds with attractive yields and favorable risk-return profiles, investors can generate a steady stream of income from coupon payments, supporting their long-term financial goals. Bond valuation can also contribute to capital appreciation, as investors who buy undervalued bonds may benefit from price increases over time. By identifying mispriced bonds and capturing potential capital gains, investors can enhance their total return on investment. Estimating future cash flows in bond valuation can be subjective, as it requires assumptions about interest rates, inflation, and other factors that may change over time. This subjectivity can lead to differing valuations among investors, potentially resulting in price discrepancies and investment inefficiencies. A bond valuation can be affected by changes in market conditions, such as shifts in investor sentiment, regulatory changes, or market disruptions. These factors can alter the dynamics of the fixed-income market, potentially leading to inaccurate valuations and increased investment risk. Modeling complex bond structures, such as those with embedded options or variable interest rates, can be challenging for investors, as it requires sophisticated valuation techniques and a deep understanding of the bond's features. This complexity can lead to mispricing and investment mistakes, particularly for less experienced investors. Credit rating agencies, while providing valuable insights into an issuer's creditworthiness, may not always accurately reflect the true risk of a bond investment. Credit rating limitations, such as potential conflicts of interest, analytical errors, or delays in updating ratings, can result in misleading valuations and investment decisions. Bond valuation is a critical aspect of investment decision-making, enabling investors to assess the fair value of bonds and make informed choices. Different methods, such as discounted cash flow and yield to maturity, are used to determine the value of bonds. Factors such as interest rate changes, inflation expectations, credit rating changes, economic conditions, market liquidity, and the issuer's financial health affect bond valuation. Bond valuation helps investors achieve portfolio diversification, manage risk, generate income, and potentially earn capital appreciation. However, there are limitations and challenges, including subjectivity in estimating future cash flows, changes in market conditions, difficulty in modeling complex bond structures, and limitations of credit ratings. Awareness of these factors and limitations is essential for investors to make sound investment decisions.What Is Bond Valuation?

Types of Bonds

Government Bonds

Corporate Bonds

Municipal Bonds

Bond Components

Face Value

Coupon Rate

Maturity Date

Issuer's Credit Rating

Bond Valuation Theories and Concepts

Present Value and Discounting

Yield to Maturity (YTM)

Duration and Modified Duration

Convexity

Bond Valuation Methods

Traditional Bond Valuation Methods

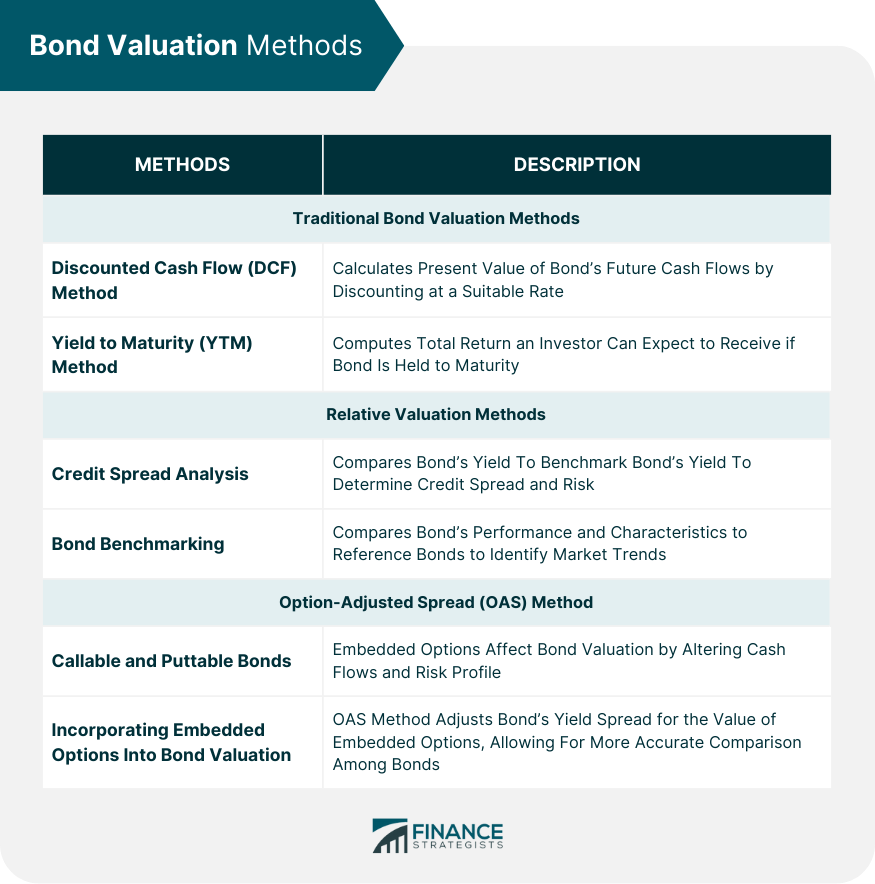

Discounted Cash Flow (DCF) Method

Yield to Maturity (YTM) Method

Relative Valuation Methods

Credit Spread Analysis

Bond Benchmarking

Option-Adjusted Spread (OAS) Method

Callable and Puttable Bonds

Incorporating Embedded Options Into Bond Valuation

Factors Affecting Bond Valuation

Interest Rate Changes

Inflation Expectations

Credit Rating Changes

Economic Conditions

Market Liquidity

Issuer's Financial Health

Bond Valuation in Investment Decisions

Portfolio Diversification

Risk Management

Income Generation

Capital Appreciation

Limitations and Challenges in Bond Valuation

Subjectivity in Estimating Future Cash Flows

Changes in Market Conditions

Difficulty in Modeling Complex Bond Structures

Credit Rating Limitations

Final Thoughts

Bond Valuation FAQs

Bond valuation is the process of determining the fair value or theoretical price of a bond by calculating the present value of its future cash flows, such as coupon payments and principal repayment. It is crucial for investors because it allows them to assess the attractiveness of a bond relative to its market price, guiding investment decisions and helping them manage risk, generate income, and achieve capital appreciation.

Changes in interest rates directly impact bond valuation, as they influence the discount rate used in calculating the present value of a bond's future cash flows. When interest rates rise, bond prices tend to fall, and vice versa. Monitoring interest rate movements is essential for investors to adjust their bond investment strategies accordingly.

Common bond valuation methods include the discounted cash flow (DCF) method, yield to maturity (YTM) method, credit spread analysis, bond benchmarking, and option-adjusted spread (OAS) method. These techniques help investors estimate a bond's intrinsic value, compare bonds with different characteristics, and account for embedded options in callable and puttable bonds.

In addition to interest rate changes, factors that can influence bond valuation include inflation expectations, credit rating changes, economic conditions, market liquidity, and the issuer's financial health. These factors can affect the perceived risk and return of a bond, altering its valuation and, ultimately, its attractiveness to investors.

Limitations and challenges in bond valuation include subjectivity in estimating future cash flows, changes in market conditions, difficulty in modeling complex bond structures, and credit rating limitations. Investors need to be aware of these challenges to make informed investment decisions and optimize their fixed income portfolios.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.