Bond rating agencies are specialized organizations that evaluate the creditworthiness of issuers of debt securities, such as bonds, and assign ratings to these securities based on their assessments. These ratings are used by investors to make informed decisions about the potential risks and returns of their investments. Bond ratings play a critical role in the financial markets by helping investors gauge the likelihood that a bond issuer will default on its debt obligations. These ratings influence the cost of borrowing for issuers and inform investment decisions by institutional and individual investors, thereby impacting the overall efficiency and stability of the financial system. Three major bond rating agencies dominate the industry: Standard & Poor's (S&P), Moody's Investors Service, and Fitch Ratings. Collectively, they are often referred to as the "Big Three" and are responsible for the majority of global bond ratings. The first bond rating agency, John Moody & Company, was founded in 1909 by John Moody. The company initially provided ratings for railroad bonds, which were the primary form of corporate debt at that time. The success of Moody's ratings led to the creation of other rating agencies, such as Poor's Publishing Company (later Standard & Poor's) and Fitch Publishing Company. Throughout the 20th century, bond rating agencies expanded their coverage to include various types of debt securities issued by corporations, municipalities, and sovereign governments. This growth was driven by increasing demand for credit analysis from investors, as well as the agencies ability to provide an independent, objective assessment of credit risk. By the late 20th century, the "Big Three" rating agencies—S&P, Moody's, and Fitch—had emerged as the dominant players in the bond rating industry. Their ratings became widely recognized and used by market participants around the world, solidifying their role in the global financial system. Rating agencies consider various qualitative factors in their assessments, including the quality of an issuer's management team, its competitive position within its industry, and the overall business environment. These factors help agencies gain a deeper understanding of the issuer's ability to meet its debt obligations. Quantitative factors, such as financial ratios, debt levels, and cash flow, are also considered in the bond rating process. These metrics provide insights into the issuer's financial strength and stability, enabling rating agencies to quantify the issuer's credit risk. Investment-grade ratings are assigned to bonds with a relatively low risk of default. These ratings generally range from AAA (highest quality) to BBB- (lowest investment grade) on the S&P and Fitch scales and from Aaa to Baa3 on Moody's scale. Investment-grade bonds are typically favored by conservative investors and are more likely to attract lower borrowing costs. Speculative-grade ratings, often referred to as "junk" or "high-yield" bonds, are assigned to bonds with a higher risk of default. These ratings generally range from BB+ to D on the S&P and Fitch scales and from Ba1 to C on Moody's scale. Speculative-grade bonds offer higher yields to compensate for their increased risk but also come with higher borrowing costs. Bond rating agencies continually monitor the creditworthiness of issuers and update their ratings as needed to reflect changes in the issuer's financial condition or business environment. This ongoing surveillance ensures that investors have access to accurate and up-to-date information on the credit risk associated with their bond investments. Bond ratings directly influence the borrowing costs for issuers, as higher-rated bonds are considered less risky and therefore attract lower interest rates. Conversely, lower-rated bonds carry higher interest rates, as investors demand higher yields to compensate for the increased risk of default. This dynamic helps allocate capital more efficiently across the financial system. Bond ratings serve as a critical tool for investors in managing the risk of their fixed-income portfolios. By providing an independent assessment of credit risk, rating agencies help investors make informed decisions about which bonds to include in their portfolios based on their risk tolerance and return objectives. Regulators use bond ratings to monitor the health of financial institutions and ensure the stability of the financial system. Ratings can inform capital adequacy requirements, which dictate the amount of capital financial institutions must hold to protect against potential losses. Additionally, regulators often rely on ratings to assess the credit risk of securities held by institutional investors, such as pension funds and insurance companies. Bond rating agencies have faced criticism for potential conflicts of interest, as they are typically paid by the issuers whose securities they rate. This arrangement may create an incentive for agencies to assign higher ratings to attract and retain clients, ultimately undermining the objectivity and credibility of their ratings. The role of bond rating agencies in the 2007-2008 financial crisis came under scrutiny, as they had assigned high ratings to mortgage-backed securities that subsequently defaulted. These inaccurate ratings contributed to the overvaluation of these securities, exacerbating the severity of the financial crisis and leading to calls for increased oversight and regulation of rating agencies. Inaccurate ratings have also been observed in other instances, such as the Enron scandal and the European sovereign debt crisis. These episodes have further highlighted the potential shortcomings of rating agencies and fueled ongoing debates about their effectiveness and reliability in assessing credit risk. In response to these controversies, regulators have introduced reforms aimed at enhancing the transparency, accountability, and independence of rating agencies. Measures include the Dodd-Frank Wall Street Reform and Consumer Protection Act in the United States and the European Union's Credit Rating Agencies Regulation, both of which impose stricter disclosure requirements and seek to mitigate conflicts of interest. Bond rating agencies play a critical role in the global financial system by evaluating the creditworthiness of debt issuers and providing investors with crucial information on credit risk. Despite their importance, these agencies have faced controversies and criticism, particularly in relation to conflicts of interest and inaccurate ratings. Technological advancements and evolving regulations are shaping the future of the bond rating industry, with the potential to improve rating methodologies and promote competition. In conclusion, bond rating agencies are essential to the functioning of global financial markets, as they help determine borrowing costs, facilitate risk management for investors, and inform regulatory oversight. While challenges and controversies persist, ongoing technological innovation and regulatory reform have the potential to strengthen the industry and enhance its ability to assess credit risk accurately and effectively.What Are Bond Rating Agencies?

History of Bond Rating Agencies

Early Origins

Growth and Expansion

Emergence of Major Players

Bond Rating Process

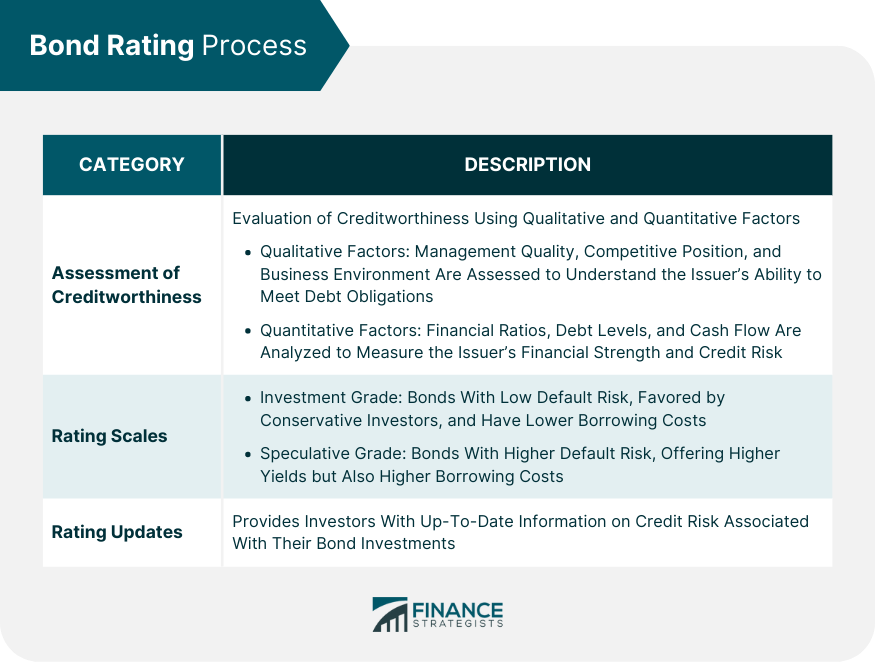

Assessment of Creditworthiness

Qualitative Factors

Quantitative Factors

Rating Scales

Investment Grade

Speculative Grade

Rating Updates and Surveillance

Role of Bond Rating Agencies in the Financial System

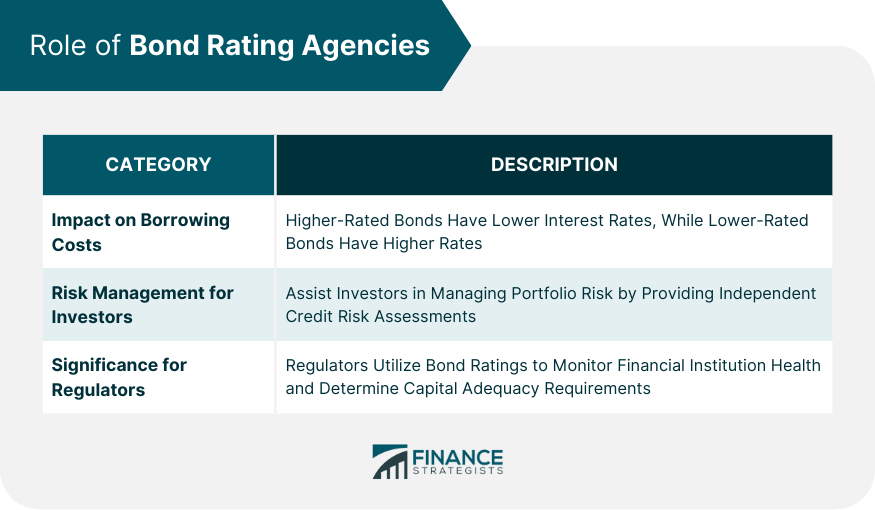

Impact on Borrowing Costs

Risk Management for Investors

Significance for Regulators

Controversies and Criticisms on Bond Rating Agencies

Conflicts of Interest

Inaccurate Ratings

Financial Crisis of 2007-2008

Other Notable Instances

Regulatory Responses and Reforms

Final Thoughts

Bond Rating Agencies FAQs

Bond rating agencies are specialized organizations that assess the creditworthiness of issuers of debt securities, such as bonds. They assign ratings to these securities based on their evaluations, which help investors gauge the potential risks and returns of their investments.

The three major bond rating agencies are Standard & Poor's (S&P), Moody's Investors Service, and Fitch Ratings. Often referred to as the "Big Three," these agencies dominate the bond rating industry and are responsible for the majority of global bond ratings.

Bond rating agencies consider both qualitative and quantitative factors when assessing creditworthiness. Qualitative factors include management quality, industry competitiveness, and the overall business environment. Quantitative factors involve financial metrics, such as debt levels, financial ratios, and cash flow. By analyzing these factors, rating agencies determine an issuer's ability to meet its debt obligations and assign a rating accordingly.

Bond rating agencies have faced controversies and criticisms related to conflicts of interest and inaccurate ratings. Since they are typically paid by the issuers they rate, there may be an incentive to assign higher ratings to attract and retain clients. Inaccurate ratings have also been a concern, as demonstrated by the financial crisis of 2007-2008, the Enron scandal, and the European sovereign debt crisis.

Technological advancements, such as automation, big data, and artificial intelligence (AI), have the potential to transform the bond rating process. Automation can streamline assessments and reduce human bias, while big data and AI can enable rating agencies to refine their methodologies and incorporate new sources of information. These advancements can lead to more accurate and timely bond ratings, ultimately benefiting investors and the financial system as a whole.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.