Tax planning for charitable giving is the process of strategically donating money or assets to charitable organizations to maximise the tax benefits while fulfilling philanthropic objectives. Tax planning for charitable giving is essential to financial and estate planning. It helps individuals and organizations achieve their charitable goals while minimizing the tax burden. Charitable donations play a vital role in funding various philanthropic causes, including education, healthcare, scientific research, poverty alleviation, environmental protection, and religious organizations. The government incentivizes charitable giving by providing tax benefits to donors. By taking advantage of these tax benefits, donors can support charitable organizations more efficiently and cost-effectively. The goals of tax planning for charitable giving include maximizing tax benefits, minimizing tax liabilities, achieving philanthropic objectives, and integrating charitable giving into an overall financial and estate plan. Cash donations are the most common form of charitable giving. Donors can deduct cash donations up to 60% of their adjusted gross income (AGI) in the year of the contribution. For example, if a donor's AGI is $100,000, they can deduct up to $60,000 in cash donations in that year. Non-cash donations include tangible personal property, real estate, securities and stocks, and life insurance policies. Tangible personal property includes items such as artwork, antiques, jewelry, and collectibles. Donors can deduct the fair market value of the property, subject to certain limitations. The deduction is limited to 30% of the donor's AGI in the year of the contribution, with a five-year carryover provision for any excess. Real estate donations can be an effective way to support charitable organizations while gaining significant tax benefits. Donors can deduct the fair market value of the property, subject to certain limitations. The deduction is limited to 30% of the donor's AGI in the year of the contribution, with a five-year carryover provision for any excess. Donating appreciated securities and stocks can be a tax-efficient way to support charitable organizations. Donors can deduct the fair market value of the securities or stocks on the date of the contribution, subject to certain limitations. Donors can also avoid paying capital gains tax on the appreciation of the securities or stocks. Donors can donate life insurance policies to charitable organizations and receive significant tax benefits. The tax deduction is generally the lesser of the policy's fair market value or the donor's basis in the policy. If the policy is fully paid up, the donor can deduct the policy's replacement value. Donor-advised funds (DAFs) are charitable giving vehicles that allow donors to make a charitable contribution to a fund and receive an immediate tax deduction. The donor can then recommend grants from the fund to eligible charitable organizations over time. DAFs provide flexibility and control over charitable giving while simplifying recordkeeping and administration. Charitable trusts are legal arrangements that allow donors to make charitable gifts while retaining some control over the donated assets. There are two types of charitable trusts: charitable remainder trusts and charitable lead trusts. Charitable remainder trusts (CRTs) allow donors to donate assets to a trust and receive income from the trust for a specified period. At the end of the period, the remaining assets are distributed to charitable organizations. CRTs provide donors with income tax deductions for the present value of the charitable remainder interest. Charitable lead trusts (CLTs) allow donors to donate assets to a trust and provide income to charitable organizations for a specified period. At the end of the period, the remaining assets are distributed to the donor or their beneficiaries. CLTs provide donors with gift tax deductions for the present value of the charitable lead interest. Bequests and estate gifts are charitable contributions made through a will or trust. Donors can leave a specific amount or a percentage of their estate to a charitable organization, providing tax benefits to their heirs and supporting philanthropic causes. Bequests and estate gifts effectively leave a lasting legacy and support charitable organizations beyond one's lifetime. Donors can deduct charitable contributions on their tax returns, reducing their taxable income and lowering their tax liability. The tax deduction is based on the type of donation and the donor's AGI. To be eligible for a tax deduction, the charitable organization must be qualified under Section 501(c)(3) of the Internal Revenue Code. Donors should verify the organization's eligibility before making a donation. The deduction limit for cash donations is 60% of the donor's AGI. The deduction limit for non-cash donations is generally 30% of the donor's AGI, with some exceptions. For example, donations of appreciated securities and stocks are limited to 30% of the donor's AGI but allow donors to avoid paying capital gains tax on the appreciation. If the donor's contributions exceed the deduction limit in a given year, they can carry over the excess to future years. The carryover period is generally five years. Charitable contributions reduce taxable income, providing donors with significant tax benefits. For example, if a donor's AGI is $100,000 and they make a $10,000 charitable donation, their taxable income is reduced to $90,000. Donating appreciated assets, such as securities and stocks, can provide donors with significant capital gains tax savings. Donors can deduct the fair market value of the assets and avoid paying capital gains tax on the appreciation. Charitable contributions can also provide estate and gift tax benefits. Donors can reduce their taxable estate by donating assets to charitable organizations, providing significant tax savings to their heirs. Additionally, donors can use charitable giving to make tax-free gifts to their heirs through charitable trusts and other estate planning techniques. Donors can strategically time their charitable contributions to maximize tax benefits. For example, if a donor expects to have a higher income in the current year than the following year, they can accelerate their charitable contributions to the current year to receive a higher tax deduction. Bunching deductions involve grouping several years of charitable contributions into a single year to exceed the standard deduction and receive a higher tax deduction. For example, if a donor typically donates $5,000 per year, they can donate $25,000 in a single year and itemize their deductions to receive a higher tax deduction. Donating appreciated assets, such as securities and stocks, can provide significant tax benefits. Donors can deduct the fair market value of the assets and avoid paying capital gains tax on the appreciation. Donors should consider donating appreciated assets that have been held for more than one year to receive the maximum tax benefits. Donors who are age 70 1/2 or older can make qualified charitable distributions (QCDs) from their Individual Retirement Accounts (IRAs) directly to charitable organizations. QCDs count towards the donor's required minimum distribution (RMD) and provide tax-free distributions of up to $111,000 in 2026 ($108,000 in 2025). QCDs are a tax-efficient way for donors to support charitable organizations while fulfilling their RMD requirements. Planned giving strategies involve making long-term commitments to charitable organizations, such as through charitable trusts, bequests, and endowments. Planned giving strategies provide donors significant tax benefits while supporting philanthropic causes for many years. Donors should work with tax and financial advisors to develop an effective planned giving strategy that aligns with their financial and philanthropic goals. Donors should keep receipts or other documentation of cash donations to charitable organizations. The documentation should include the name of the organization, the date of the donation, and the amount of the donation. Donors should obtain appraisals for non-cash donations, such as real estate and tangible personal property, that exceed $5,000. The appraisal should be conducted by a qualified appraiser and should include a description of the property, the appraised value, and the method used to determine the value. Donors must substantiate their charitable contributions to claim a tax deduction. The substantiation requirements vary based on the type and amount of the donation. Donors should consult the IRS guidelines for substantiation requirements. Donors should report their charitable contributions on their tax returns using Form 1040, Schedule A. Donors who donate appreciated assets, such as securities and stocks, may need to file additional tax forms, such as Form 8283, for non-cash donations exceeding $500. Donors should consult with their tax advisors to ensure they are filing the correct tax forms. Donors should work with a qualified tax advisor who specializes in charitable giving and understands the tax implications of different types of donations. The tax advisor should be knowledgeable about the tax laws and regulations related to charitable giving and should be able to provide guidance on the best tax planning strategies for maximizing the impact of charitable donations. Donors should work with their tax and financial advisors to develop a comprehensive charitable giving plan that aligns with their financial and philanthropic goals. The plan should include strategies for maximizing tax benefits, integrating charitable giving into an overall financial and estate plan, and selecting the most effective charitable giving vehicles. Donors should regularly monitor and update their charitable giving plan to ensure it aligns with their changing financial and philanthropic goals. Donors should review their plans with their tax and financial advisors annually or as their circumstances change. Tax planning for charitable giving is a valuable tool for individuals and organizations to maximize their donations and tax benefits while fulfilling philanthropic objectives. By strategically timing contributions, considering appreciated assets, utilizing qualified charitable distributions, and implementing planned giving strategies, donors can optimize their tax savings and support charitable causes effectively. It is crucial to maintain proper recordkeeping and documentation, including receipts and appraisals for non-cash donations, and consult with qualified tax advisors to navigate the complexities of tax laws and regulations. Developing a comprehensive charitable giving plan, regularly reviewing and updating it with the guidance of tax and financial advisors, ensures that charitable goals align with changing financial circumstances. Through strategic tax planning for charitable giving, individuals and organizations can make a lasting impact on philanthropic causes while minimizing their tax burden.What Is Tax Planning for Charitable Giving?

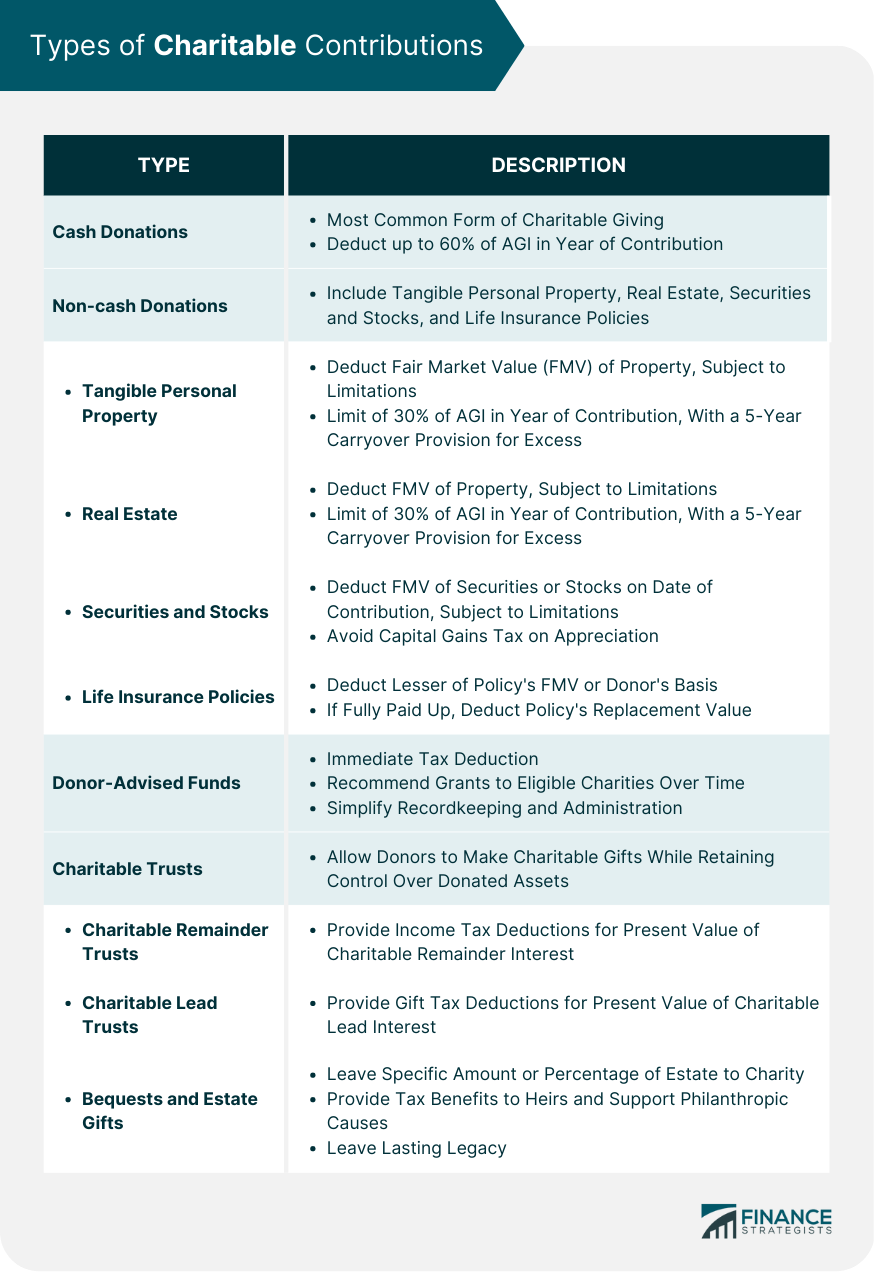

Types of Charitable Contributions

Cash Donations

Non-cash Donations

Tangible Personal Property

Real Estate

Securities and Stocks

Life Insurance Policies

Donor-Advised Funds

Charitable Trusts

Charitable Remainder Trusts

Charitable Lead Trusts

Bequests and Estate Gifts

Tax Benefits of Charitable Giving

Deduction for Charitable Contributions

Eligible Organizations

Limits on Deductions

Carryover Provisions

Reduction of Taxable Income

Capital Gains Tax Savings

Estate and Gift Tax Benefits

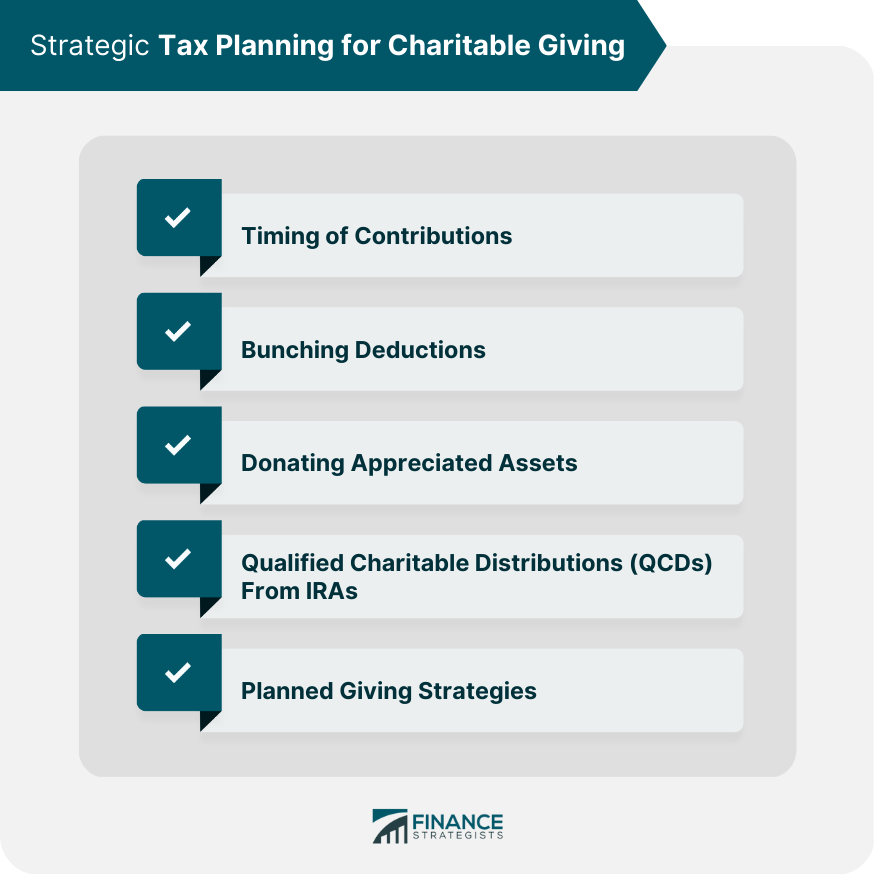

Strategic Tax Planning for Charitable Giving

Timing of Contributions

Bunching Deductions

Donating Appreciated Assets

Qualified Charitable Distributions (QCDs) From IRAs

Planned Giving Strategies

Recordkeeping and Documentation for Charitable Giving

Receipts for Cash Donations

Appraisals for Non-cash Donations

Substantiation Requirements

Filing Tax Forms

Working With Tax and Financial Advisors

Selecting a Tax Advisor

Developing a Charitable Giving Plan

Monitoring and Updating the Plan

Final Thoughts

Tax Planning for Charitable Giving FAQs

Tax planning for charitable giving is the process of strategically donating money or assets to charitable organizations in a way that maximizes tax benefits while fulfilling philanthropic objectives.

Tax benefits of charitable giving include deductions for charitable contributions, reduction of taxable income, capital gains tax savings, and estate and gift tax benefits.

Strategic tax planning techniques for charitable giving include timing of contributions, bunching deductions, donating appreciated assets, qualified charitable distributions (QCDs) from IRAs, and planned giving strategies.

The different types of charitable contributions include cash donations, non-cash donations such as tangible personal property, real estate, securities and stocks, and life insurance policies, donor-advised funds, charitable trusts such as charitable remainder trusts and charitable lead trusts, and bequests and estate gifts.

Working with tax and financial advisors is important for tax planning for charitable giving because they can provide expertise on the tax laws and regulations related to charitable giving and help donors develop a comprehensive charitable giving plan that aligns with their financial and philanthropic goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.