National Insurance Contributions (NIC) are mandatory payments made by employees, employers, and self-employed individuals in the United Kingdom. These contributions fund various state benefits, including pensions, unemployment benefits, and maternity allowances. The primary purpose of NIC is to support the UK's social security system and provide funding for state benefits. These contributions help ensure that individuals have access to a safety net in times of need, such as retirement, illness, or unemployment. NIC was first introduced in the UK in 1911 as a part of the National Insurance Act. The system has evolved over the years to accommodate changes in society and the economy, with the current structure established in 1975 comprising four different classes of contributions. Class 1 NIC applies to employees and employers, with both parties required to contribute based on the employee's earnings. Employees pay Class 1 NIC on their earnings above a certain threshold. The amount they pay depends on their income level and is deducted automatically from their wages by their employer. Employers are also required to pay Class 1 NIC on their employees' earnings above a specified threshold. The employer's contribution is in addition to the employee's contribution and is paid directly to HM Revenue and Customs (HMRC). Class 2 NIC is designed for self-employed individuals and includes voluntary contributions. Self-employed individuals pay Class 2 NIC at a fixed weekly rate, regardless of their profits. These contributions count toward the individual's state pension and other qualifying benefits. Voluntary Class 2 NIC allows individuals with gaps in their NIC record to make additional contributions to qualify for state benefits, such as the state pension. Class 3 NIC is a voluntary contribution that individuals can make to increase their entitlement to state benefits. Individuals who have gaps in their NIC record or who are not required to pay Class 1 or Class 2 NIC, can choose to pay Class 3 NIC to qualify for state benefits. To pay Class 3 NIC, individuals must meet certain eligibility criteria, such as being over 16 years old and having gaps in their NIC record. Class 4 NIC applies to self-employed individuals whose profits exceed a certain threshold. Self-employed individuals with profits above the specified threshold pay Class 4 NIC in addition to Class 2 NIC. Class 4 NIC is calculated as a percentage of the individual's taxable profits. The amount of Class 4 NIC paid depends on the individual's profit level, with higher profits resulting in a higher percentage contribution. NIC rates are determined by the UK government and vary depending on the class of contribution and the individual's earnings or profits. Rates and thresholds are usually reviewed and updated annually to account for inflation and other economic factors. Class 1 NIC rates are divided into primary (employee) and secondary (employer) rates. Both rates are determined as a percentage of the employee's earnings, with different thresholds and percentage rates applicable depending on the level of earnings. Class 2 NIC has a fixed weekly rate that applies to all self-employed individuals, regardless of their profits. The rate is subject to annual review and may be adjusted to reflect changes in the economy. Class 3 NIC rates are set as a fixed weekly amount. Individuals choosing to pay voluntary Class 3 contributions can do so to fill gaps in their NIC record and increase their eligibility for state benefits. Class 4 NIC rates are determined as a percentage of the self-employed individual's taxable profits. The rates are divided into two bands, with different percentage rates applicable depending on the level of profits. Rates and thresholds for NIC are subject to annual review by the UK government. Changes are typically announced during the annual budget and implemented at the beginning of the new tax year to account for inflation and other economic factors. Qualifying years are the number of years an individual has paid or been credited with NICs. These years determine eligibility for the state pension, with a minimum number of qualifying years required to receive any pension and a higher number needed for a full state pension. To be eligible for the state pension, individuals must have paid or been credited with sufficient NICs throughout their working life. Both Class 1 and Class 2 NICs count towards the state pension, while voluntary Class 3 NICs can be used to fill gaps in the individual's NIC record. Jobseeker's Allowance (JSA) is a benefit for individuals who are unemployed and actively seeking work. Eligibility for JSA depends on the individual's NIC record, age, and meeting specific work-related requirements. There are two types of JSA: contribution-based and income-based. Contribution-based JSA is dependent on the individual's NIC record, while income-based JSA is determined by the individual's income and savings. Employment and Support Allowance (ESA) provides financial support for individuals who are unable to work due to illness or disability. Eligibility for ESA is based on the individual's NIC record, medical assessments, and work-related requirements. ESA is available as contribution-based and income-based allowances. Contribution-based ESA depends on the individual's NIC record, while income-based ESA takes into account the individual's income and savings. Maternity Allowance is a benefit for pregnant women or new mothers who do not qualify for Statutory Maternity Pay. Eligibility for Maternity Allowance is based on the individual's NIC record and employment status. To qualify for Maternity Allowance, individuals must have paid sufficient NICs during a specific test period before their baby is due. Both Class 1 and Class 2 NICs count towards Maternity Allowance and deduct Class 1 NICs from employees' wages using their payroll system. This process includes keeping track of employees' earnings, applying the correct NIC rates and thresholds, and accounting for any changes in rates during the tax year. Employers are required to report and pay NICs to HMRC on a regular basis, typically monthly or quarterly. Reporting and payment deadlines are set by HMRC and must be adhered to in order to avoid penalties and interest charges. Failure to comply with NIC responsibilities, such as not paying the correct amount of NICs or missing payment deadlines, can result in penalties from HMRC. Penalties can include fines, interest charges, and potential legal action. Self-employed individuals are responsible for registering with HMRC as self-employed, maintaining accurate records of their business income and expenses, and calculating and paying Class 2 and Class 4 NICs as required. NIC payment deadlines for self-employed individuals depend on the class of NIC being paid. Class 2 NICs are typically paid through the Self-Assessment tax return, while Class 4 NICs are paid in two installments throughout the tax year. Self-employed individuals must complete a Self-Assessment tax return annually to report their business income, expenses, and calculate their tax and NIC liabilities. This process includes declaring Class 2 and Class 4 NICs and making any necessary payments to HMRC. There are some exemptions and special circumstances for self-employed individuals regarding NIC. For example, individuals with low profits may be exempt from paying Class 2 NICs, and those with specific circumstances, such as working abroad, may have different NIC requirements. Non-resident workers in the UK may still be required to pay NICs depending on their employment status and the length of their stay. Understanding the rules and requirements for non-resident workers is crucial to ensure compliance with UK tax regulations. The UK has social security agreements with various countries to prevent double payment of NICs for individuals working in more than one country. These agreements help determine which country's social security system the individual should contribute to and can simplify NIC obligations for international workers. Expatriate workers and individuals on temporary postings may have different NIC requirements based on their home country, the duration of their stay, and their employment status. It is essential for these workers to understand and comply with the relevant NIC rules and regulations. Non-residents who have previously lived or worked in the UK and have gaps in their NIC record can choose to make voluntary NICs to maintain their eligibility for UK state benefits. This option is particularly beneficial for individuals who plan to return to the UK or claim UK state benefits in the future. Direct Debit is a convenient and secure method for paying NICs, allowing individuals and employers to automate their payments and ensure they are made on time. This payment method reduces the risk of missed deadlines and penalties. Online and telephone banking provide alternative methods for making NIC payments. These options offer flexibility and convenience, allowing individuals and employers to manage their NIC obligations from anywhere with internet or telephone access. Cheque and postal payments are traditional methods for paying NICs, which may still be used by some individuals and employers. It is essential to allow sufficient time for postal payments to reach HMRC before the payment deadline to avoid penalties. Payment on account is an option for self-employed individuals to make advance payments towards their NIC liabilities for the current tax year. This method helps individuals spread the cost of their NICs and reduce the risk of unexpected tax bills at the end of the tax year. Meeting NIC payment deadlines is crucial to avoid penalties and interest charges. Deadlines vary depending on the class of NIC, employment status, and chosen payment method. It is essential to understand and adhere to the relevant deadlines for each individual or employer. National Insurance Contributions (NIC) in the United Kingdom are mandatory payments made by employees, employers, and self-employed individuals to fund state benefits such as pensions, jobseeker's allowance, employment and support allowance, and maternity allowance. There are different classes of NICs, including Class 1 for employees and employers, Class 2 for self-employed individuals, Class 3 for voluntary contributions, and Class 4 for self-employed individuals based on taxable profits. NIC rates and thresholds are determined by the government and are subject to annual review. Qualifying years of NICs are essential for eligibility for state benefits, and individuals must meet specific criteria for each benefit. Self-employed individuals have additional responsibilities such as registration, record-keeping, and tax returns. Compliance with NIC obligations, including payment deadlines, is crucial to avoid penalties. Various payment methods, including direct debit, online banking, and postal payments, are available for NIC payments. Understanding the complexities of NIC and state benefits is vital for individuals and employers to ensure compliance and access to the appropriate benefits.What Are National Insurance Contributions (NIC)?

Types of NIC

Class 1 NIC

Employee Contributions

Employer Contributions

Class 2 NIC

Self-Employed Individuals

Voluntary Contributions

Class 3 NIC

Voluntary Contributions

Eligibility Criteria

Class 4 NIC

Self-Employed Individuals

Profit-Based Contributions

NIC Rates and Thresholds

Class 1 NIC Rates and Thresholds

Class 2 NIC Rates and Thresholds

Class 3 NIC Rates and Thresholds

Class 4 NIC Rates and Thresholds

Annual Updates and Changes to Rates and Thresholds

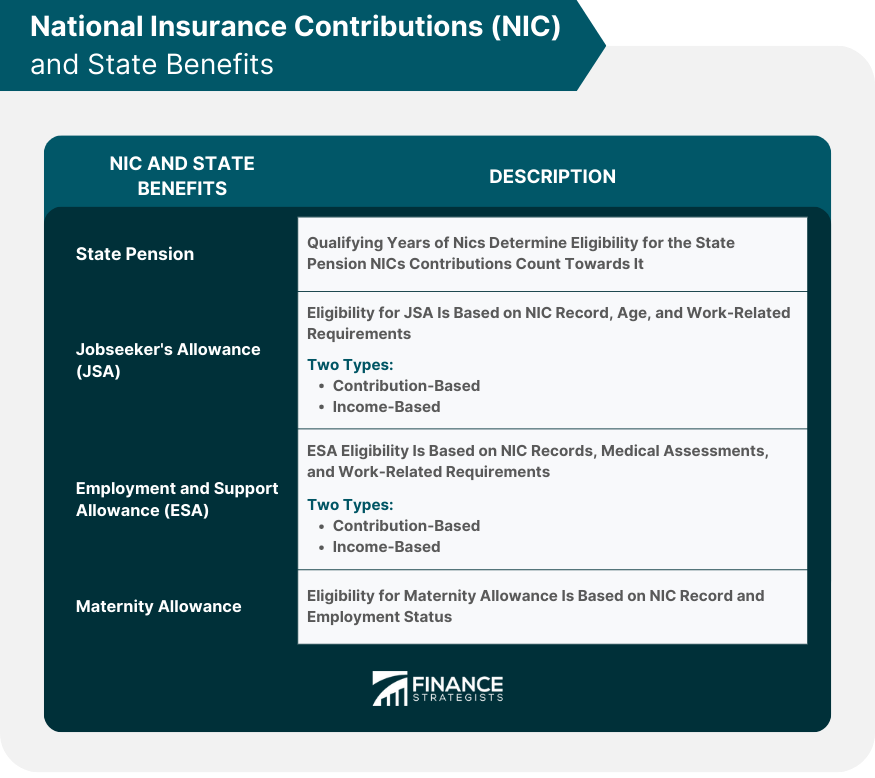

NIC and State Benefits

State Pension

Qualifying Years

Contribution Requirements

Jobseeker's Allowance

Eligibility Criteria

Contribution-Based and Income-Based Allowances

Employment and Support Allowance

Eligibility Criteria

Contribution-Based and Income-Based Allowances

Maternity Allowance

Eligibility Criteria

Contribution Requirements

Reporting and Payment Deadlines

Penalties for Non-compliance

NIC for the Self-Employed

Registration and Record-Keeping

NIC Payment Deadlines

Tax Returns and NIC

Exemptions and Special Circumstances

NIC for Expatriates and International Workers

Non-resident Workers

Social Security Agreements

Temporary Postings and Expatriate Workers

Voluntary NIC for Non-residents

NIC Payment Methods and Deadlines

Direct Debit

Online and Telephone Banking

Cheque and Postal Payments

Payment on Account

Payment Deadlines and Penalties

Final Thoughts

National Insurance Contributions (NIC) FAQs

There are four classes of NICs: Class 1 for employees and employers, Class 2 for self-employed individuals, Class 3 for voluntary contributions, and Class 4 for self-employed individuals with profit-based contributions. The type of NIC you pay depends on your employment status and income.

NICs are crucial for determining your eligibility for various UK state benefits. A sufficient number of qualifying years and contributions are required for benefits like the State Pension, Jobseeker's Allowance, Employment and Support Allowance, Maternity Allowance, and Bereavement Support Payment.

Employers are responsible for deducting Class 1 NICs from employees' wages, paying employers' Class 1 NICs, maintaining accurate payroll records, and reporting and paying NICs to HMRC. Failure to comply with these responsibilities can result in penalties and interest charges.

Expatriates and international workers may have different NIC requirements based on their home country, duration of their stay, and employment status. Social security agreements between the UK and other countries can help determine which country's system they should contribute to and simplify NIC obligations for international workers.

Payment methods for NICs include Direct Debit, online and telephone banking, cheque and postal payments, and payment on account for self-employed individuals. Deadlines for payments vary depending on the class of NIC, employment status, and chosen payment method. Adhering to payment deadlines is essential to avoid penalties and interest charges.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.