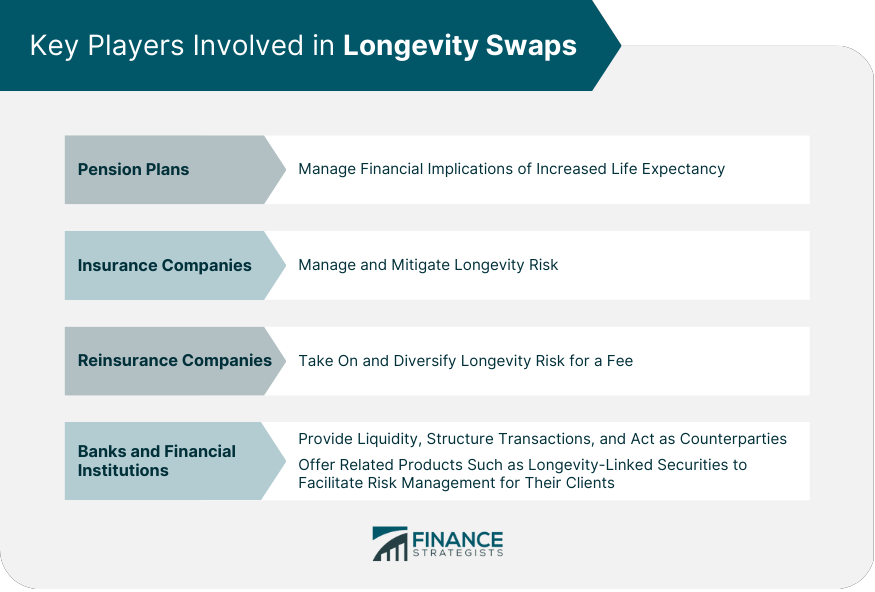

Longevity swaps are financial instruments designed to mitigate the risks associated with increased life expectancy for pension plans and insurance companies. These products allow institutions to hedge against the financial consequences of their policyholders or pensioners living longer than expected. This article explores the mechanics, risk management, pricing, and valuation of longevity swaps, along with the market developments and trends shaping this growing sector. Longevity swaps involve various stakeholders, including pension plans, insurance companies, reinsurance companies, banks, and other financial institutions. Each player serves a critical role in facilitating and managing these complex transactions. Pension plans, both defined benefit and defined contribution, are designed to provide income to retirees. As life expectancy increases, pension plans face a significant risk of underfunding, as they must support retirees for a longer period. Longevity swaps help pension plan sponsors manage the financial implications of increased life expectancy. Insurance companies, particularly those offering life insurance and annuity products, are also exposed to longevity risk. As policyholders live longer, insurers must make payments over an extended period, potentially straining their financial resources. Longevity swaps provide insurers with a means to manage and mitigate this risk. Reinsurance companies act as intermediaries, taking on the longevity risk transferred by pension plans and insurance companies. They assume this risk in exchange for a fee, providing financial stability and risk diversification for the primary institutions. Banks and other financial institutions may participate in the longevity swap market by providing liquidity, structuring transactions, and acting as counterparties. They may also offer related products, such as longevity-linked securities, to facilitate risk management for their clients. To better understand longevity swaps, we must examine the transaction process, reference population determination, swap payment calculations, and the duration and termination of these agreements. In a typical longevity swap, a pension plan or insurer (the protection buyer) enters into an agreement with a counterparty, such as a reinsurer or bank (the protection seller). The protection buyer agrees to pay a fixed series of payments to the protection seller, while the protection seller agrees to pay a floating series of payments linked to the actual longevity experience of a specified reference population. The reference population is a critical aspect of a longevity swap, as it serves as the basis for calculating the floating payments. The reference population can be the pension plan's members or policyholders of an insurance company or a broader, representative population index. The swap payments comprise two components: fixed leg payments and floating leg payments. Fixed Leg Payments: The fixed leg payments are predetermined and usually based on the expected mortality experience of the reference population, accounting for factors such as age, gender, and socio-economic status. Floating Leg Payments: The floating leg payments are based on the actual mortality experience of the reference population. If the reference population lives longer than expected, the protection seller will make higher payments to the protection buyer, effectively compensating for the increased longevity risk. At each payment date, the fixed and floating leg payments are netted, and the resulting net payment is made from one party to the other. This netting process reduces the overall transaction costs and streamlines the payment process. Longevity swap agreements typically have a long duration, often spanning decades, to align with the lifespan of the reference population. The swap agreement may include termination provisions, allowing either party to exit the transaction under specific conditions, such as a change in regulations or a significant credit event impacting the counterparty. Effective risk management is essential for parties involved in longevity swaps. This section explores longevity risk, hedging strategies, counterparty risk, and regulatory considerations. Longevity risk refers to the uncertainty surrounding future life expectancies and the potential financial consequences for pension plans and insurers. Key sources of longevity risk include medical advancements, demographic shifts, and lifestyle changes. As life expectancy increases, pension plans and insurers must manage the financial implications of making payments over longer periods. Longevity swaps serve as a valuable hedging tool for managing longevity risk. By transferring the risk to a counterparty, pension plans and insurers can stabilize their cash flows and reduce the uncertainty surrounding their future liabilities. Counterparty risk is the potential for one party in the swap agreement to default on its payment obligations. To mitigate counterparty risk, both parties should assess the creditworthiness of their counterparties and may employ credit risk transfer mechanisms, such as collateral arrangements or credit default swaps. Regulators impose capital requirements on pension plans and insurers to ensure financial stability and solvency. Longevity swaps can help institutions meet these requirements by reducing their exposure to longevity risk. Reporting and disclosure requirements for longevity swaps may vary depending on jurisdiction, necessitating regular communication with regulators and stakeholders. Pricing and valuation are critical aspects of longevity swaps. This section discusses the factors affecting swap pricing, valuation methodologies, and the challenges associated with pricing and valuation. Several factors influence the pricing of longevity swaps, including mortality and life expectancy projections, interest rates, credit spreads, and market liquidity. Mortality and Life Expectancy Projections: Accurate projections of mortality and life expectancy are crucial for determining the fixed and floating leg payments in a longevity swap. Interest Rates: Interest rates impact the present value of future swap payments, affecting the overall pricing of the swap agreement. Credit Spreads: Credit spreads represent the credit risk associated with the counterparty and can influence the pricing of longevity swaps. Market Liquidity: Market liquidity impacts the ease with which longevity swaps can be traded and the pricing of these instruments. Valuation methodologies for longevity swaps can be broadly categorized into actuarial models, market-based approaches, and hybrid models. Actuarial Models: Actuarial models rely on historical mortality data and assumptions about future mortality improvements to estimate the present value of swap payments. Market-Based Approaches: Market-based approaches utilize market data, such as interest rates and credit spreads, to derive the present value of swap payments. Hybrid Models: Hybrid models combine elements of both actuarial and market-based approaches, incorporating mortality projections and market data to estimate the present value of swap payments. Pricing and valuation of longevity swaps present several challenges, including data limitations, model risk, and market uncertainty. Data Limitations: Accurate mortality data, particularly for specific subpopulations, may be limited or difficult to obtain. Model Risk: The choice of valuation model can significantly impact the estimated present value of swap payments, introducing model risk into the pricing process. Market Uncertainty: Fluctuations in interest rates, credit spreads, and other market factors can introduce uncertainty into the pricing and valuation of longevity swaps, making it challenging to establish a precise value for these instruments. The longevity swap market has experienced significant growth and innovation in recent years. This section examines the evolution of the longevity swap market, emerging product innovations, and the outlook for future market growth. The longevity swap market has grown considerably since its inception, with an increasing number of transactions and milestones achieved. This growth can be attributed to a greater understanding of longevity risk, the need for effective risk management tools, and the development of more sophisticated financial products. The longevity swap market has seen the introduction of several innovative products and structures, including customized solutions, index-based swaps, and longevity-linked securities. Customized Solutions: Customized longevity swaps cater to the unique needs of individual pension plans or insurers, offering tailored risk management solutions. Index-Based Swaps: Index-based longevity swaps utilize a broad, representative population index as the reference population, providing a more diversified and transparent means of managing longevity risk. Longevity-Linked Securities: Longevity-linked securities, such as bonds or notes, offer another avenue for transferring longevity risk to investors, expanding the range of available risk management tools. The longevity swap market is expected to continue its growth trajectory, driven by several factors: Drivers of Market Growth: The aging population, increased life expectancy, and the growing need for effective risk management tools will likely fuel the demand for longevity swaps. Potential Barriers and Challenges: Regulatory changes, market volatility, and data limitations may pose challenges to the growth of the longevity swap market. However, ongoing innovation and product development are likely to help overcome these barriers. Emerging Trends and Their Implications: New trends, such as the adoption of technology and data analytics in the pricing and valuation process, may further enhance the efficiency and effectiveness of longevity swaps as a risk management tool. Longevity swaps have emerged as a crucial risk management tool for pension plans and insurers, providing an effective means of managing the financial implications of increased life expectancy. As the market continues to evolve and innovate, longevity swaps will likely play an increasingly important role in the long-term financial stability of these institutions. As life expectancies continue to rise and the need for effective risk management tools intensifies, the longevity swap market's growth and development will be a critical area to watch.What Are Longevity Swaps?

Key Players Involved in Longevity Swaps

Pension Plans

Insurance Companies

Reinsurance Companies

Banks and Other Financial Institutions

Mechanics of Longevity Swaps

Overview of the Transaction Process

Determination of the Reference Population

Calculation of Swap Payments

Netting and Settlement of Payments

Duration and Termination of the Swap Agreement

Risk Management in Longevity Swaps

Longevity Risk

Hedging Longevity Risk

Counterparty Risk

Regulatory Considerations

Pricing and Valuation of Longevity Swaps

Factors Affecting Swap Pricing

Valuation Methodologies

Challenges in Pricing and Valuation

Market Developments and Trends in Longevity Swaps

Evolution of the Longevity Swap Market

Innovations in Longevity Swap Products

Market Outlook and Future Opportunities

Conclusion

Longevity Swaps FAQs

Longevity swaps are financial contracts between two parties, where one party agrees to make payments to the other party, based on the lifespan of a designated group of individuals, typically retirees or pensioners.

Pension funds use longevity swaps to manage the risk of their members living longer than expected, which can cause a significant increase in pension payments, leading to financial strain on the fund.

In a longevity swap, one party, typically a pension fund, pays a premium to the other party, typically an insurance company, in exchange for protection against the risk of increased pension payments due to longer lifespans. The insurance company takes on the risk of the pension fund's members living longer than expected.

Both parties can benefit from a longevity swap. The pension fund can reduce the risk of having to make larger-than-expected pension payments, while the insurance company can generate income from the premium paid by the pension fund.

Longevity swaps are becoming more common in the financial industry, particularly among pension funds and insurance companies. The market for longevity swaps has grown significantly in recent years, as the risk of increased pension payments due to longer lifespans has become a more pressing concern for pension funds.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.