Fiduciary services are professional financial services that are provided by a fiduciary, a person or entity who is legally bound to act in the best interests of their clients. These services typically include trust administration, investment management, estate planning, retirement planning, and other related financial planning services. The fiduciary is obligated to act with the utmost loyalty, care, and good faith toward their clients and to avoid conflicts of interest. Revocable living trusts allow individuals to maintain control over their assets while providing flexibility and privacy. The trust can be amended or revoked during the grantor's lifetime. Irrevocable trusts cannot be altered or revoked once established, offering greater asset protection and tax benefits but sacrificing control over assets. Testamentary trusts are created upon the death of an individual through their will, providing asset management and distribution according to the deceased's wishes. Charitable trusts are established for philanthropic purposes, offering tax benefits to the grantor and supporting designated charitable organizations. Special needs trusts are designed to support individuals with disabilities by providing financial assistance without jeopardizing their eligibility for government benefits. A will outlines the distribution of an individual's assets upon their death, ensuring their wishes are fulfilled and minimizing potential legal disputes. Power of attorney designates a trusted individual to make financial and legal decisions on behalf of the grantor in the event of incapacity. Health care directives, such as living wills and health care proxies, provide guidance on medical treatment preferences and appoint a representative to make decisions when the individual is unable to do so. Beneficiary designations ensure that assets, such as life insurance policies and retirement accounts, are distributed to the intended recipients upon the account holder's death. Asset protection planning safeguards wealth from potential creditors, lawsuits, and other financial threats while ensuring lawful and ethical practices. Portfolio management involves creating and maintaining a diversified investment strategy that aligns with an individual's financial goals, risk tolerance, and time horizon. Asset allocation refers to the process of dividing an investment portfolio among various asset classes, such as stocks, bonds, and cash, to optimize returns and manage risk. Risk management entails identifying and mitigating potential investment risks to preserve capital and achieve long-term financial objectives. Performance monitoring involves tracking investment returns and evaluating the effectiveness of the overall investment strategy. Tax-efficient investing seeks to minimize tax liabilities by strategically managing interest income, capital gains and dividends. Retirement income planning focuses on generating a sustainable and reliable income stream during retirement while minimizing taxes and preserving assets. Social Security and pension optimization strategies ensure that retirees maximize their benefits and make informed decisions regarding their retirement income. RMDs are the minimum amounts that must be withdrawn from retirement accounts annually, starting at a specific age. Proper planning can help minimize taxes and penalties. Long-term care planning addresses the potential need for long-term care services, such as nursing homes or assisted living, and evaluates various funding options. Legacy planning focuses on preserving and transferring wealth to future generations while minimizing estate taxes and other expenses. The fiduciary standard is a set of ethical and legal principles that require a fiduciary to act in the best interests of their clients, prioritizing their clients' needs above their own. Fiduciaries must act solely in the best interests of their clients, avoiding any conflicts of interest and disclosing any potential conflicts that may arise. Fiduciaries must exercise diligence, skill, and care when providing advice and managing clients' assets, ensuring that their actions are well-informed and well-executed. Fiduciaries must identify and avoid conflicts of interest that could compromise their ability to act in their clients' best interests, and fully disclose unavoidable conflicts. Fiduciaries must provide clear, accurate, and timely information to clients, ensuring that they are fully informed about fees, risks, and potential outcomes of any recommended actions. Evaluate the provider's professional designations, educational background, and industry experience to ensure that they possess the necessary expertise. Research the provider's reputation and client feedback to gain insight into their level of service, expertise, and client satisfaction. Review the provider's range of fiduciary services to ensure that they align with your unique needs and financial objectives. Understand the provider's fee structure, including any potential conflicts of interest that may arise from their compensation model. Assess the provider's communication style, availability, and commitment to ongoing support, as effective communication is crucial for a successful fiduciary-client relationship. RIAs are regulated by the Securities and Exchange Commission (SEC) or state securities regulators and are held to a fiduciary standard when providing investment advice. Trust companies specialize in providing trust and estate services, managing assets on behalf of clients, and ensuring proper administration and distribution. Banks and financial institutions often offer fiduciary services as part of their wealth management offerings, providing a comprehensive range of financial solutions. Law firms and attorneys specializing in estate planning and trust administration can serve as fiduciaries, providing legal expertise and guidance. Wealth management firms offer a holistic approach to managing clients' financial lives, including fiduciary services as part of their comprehensive offerings. RIAs and other investment professionals are subject to oversight by the SEC, ensuring compliance with federal securities laws and regulations. State regulatory authorities play a role in overseeing fiduciary service providers, such as trust companies and certain investment advisors, to protect consumers and maintain industry standards. Some fiduciary service providers may be subject to FINRA rules, which govern the conduct of broker-dealers and registered representatives in the securities industry. Fiduciaries must adhere to legal and ethical obligations, including the fiduciary standard, to ensure they act in their clients' best interests. Client protection measures, such as insurance coverage and safeguards against fraud, help ensure that clients' assets are secure and well-protected. Fiduciary services play a vital role in safeguarding clients' financial well-being and helping them achieve their financial objectives. By understanding the types of fiduciary services, the fiduciary standard, and how to select the right service provider, individuals can make informed decisions that protect their assets and secure their financial future. As the financial world continues to evolve, seeking professional fiduciary guidance can be an invaluable investment in one's financial success.What Are Fiduciary Services?

Fiduciary services play a critical role in financial planning and wealth management, ensuring that clients' best interests are protected and their financial goals are achieved. Types of Fiduciary Services

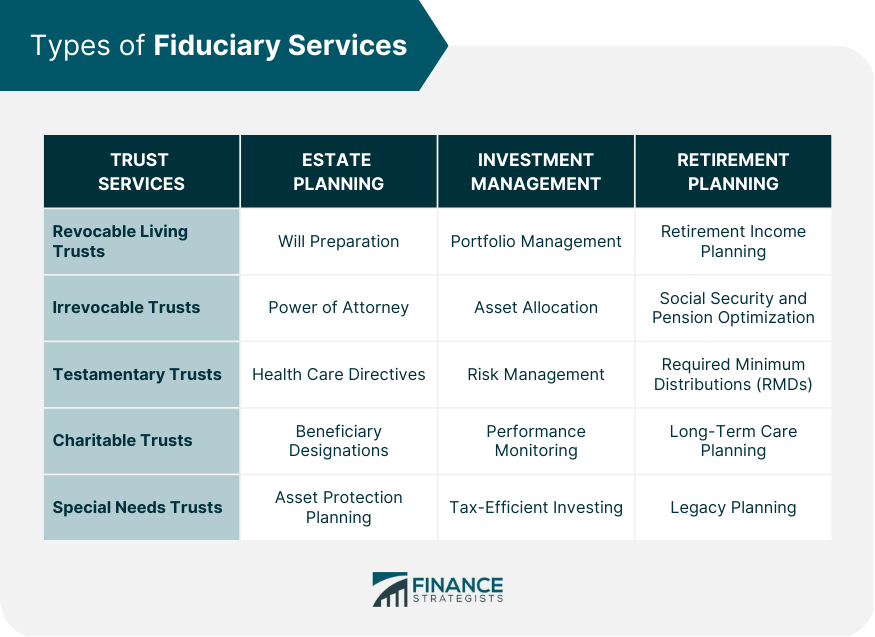

Trust Services

Revocable Living Trusts

Irrevocable Trusts

Testamentary Trusts

Charitable Trusts

Special Needs Trusts

Estate Planning

Will Preparation

Power of Attorney

Health Care Directives

Beneficiary Designations

Asset Protection Planning

Investment Management

Portfolio Management

Asset Allocation

Risk Management

Performance Monitoring

Tax-Efficient Investing

Retirement Planning

Retirement Income Planning

Social Security and Pension Optimization

Required Minimum Distributions (RMDs)

Long-Term Care Planning

Legacy Planning

The Fiduciary Standard

Definition and Principles

Duty of Loyalty

Duty of Care

Duty to Avoid Conflicts of Interest

Importance of Transparency and Full Disclosure

Selecting a Fiduciary Service Provider

Criteria for Choosing a Provider

Credentials and Experience

Reputation and Client Reviews

Service Offerings

Fee Structure

Communication and Ongoing Support

Types of Providers

Registered Investment Advisors (RIAs)

Trust Companies

Banks and Financial Institutions

Law Firms and Attorneys

Wealth Management Firms

Regulatory and Compliance Considerations

Securities and Exchange Commission (SEC) Oversight

State Regulatory Authorities

Financial Industry Regulatory Authority (FINRA) Rules

Legal and Ethical Obligations

Client Protection Measures

Conclusion

Fiduciary Services FAQs

Fiduciary services refer to a range of financial services provided by professionals who are legally and ethically bound to act in the best interests of their clients, often in a trustee or advisory capacity.

Fiduciary services can be provided by a variety of professionals, including financial advisors, wealth managers, estate planners, attorneys, and trustees.

A fiduciary service provider is legally and ethically obligated to act in the best interests of their clients, while a non-fiduciary service provider is not held to the same standard of care and may prioritize their own financial interests over their clients.

Working with a fiduciary service provider can provide peace of mind knowing that their interests are being prioritized, while also potentially helping to reduce conflicts of interest and the risk of financial abuse or exploitation.

No, not all financial advisors are considered fiduciaries. However, some financial advisors may choose to operate as fiduciaries to provide an added level of transparency and trust to their clients.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.