Fiduciary safe harbor refers to specific provisions in laws or regulations that provide protection to fiduciaries from legal liability under certain circumstances. In the context of retirement plans, fiduciary safe harbors are guidelines that, when followed, shield plan fiduciaries from liability for certain actions or decisions related to the management of the plan. These safe harbors are designed to encourage prudent and responsible behavior by fiduciaries while protecting them from legal claims. However, it's important to note that fiduciaries must still prudently select and monitor the investment options offered under the plan. The safe harbor does not absolve them of this responsibility. One common example of a fiduciary safe harbor is found in Section 404(c) of the Employee Retirement Income Security Act of 1974 (ERISA). This safe harbor provision protects fiduciaries of participant-directed individual account plans, such as 401(k) plans, from liability for investment losses that result from the investment decisions made by plan participants. To qualify for this safe harbor, the plan must meet specific requirements, including offering a broad range of investment options, allowing participants to exercise control over their accounts, and giving participants sufficient information about the investment options available to them. If a plan meets these requirements and operates in accordance with Section 404(c), the plan's fiduciaries are generally shielded from liability for the investment decisions made by participants. The Employee Retirement Income Security Act was enacted in 1974 to protect employees' retirement plan benefits. It sets standards and guidelines for pension and welfare benefit plans, ensuring that fiduciaries act in the best interest of plan participants and their beneficiaries. Reporting and disclosure requirements Fiduciary responsibility and prohibited transactions Minimum funding standards Enforcement mechanisms ERISA emphasizes the responsibility of plan sponsors and fiduciaries to act prudently and in the best interest of plan participants. Fiduciaries must follow specific guidelines and requirements to uphold their duties. Over the years, several provisions have been introduced to protect fiduciaries who follow specific guidelines and requirements. ERISA's Fiduciary Safe Harbor provisions were introduced to clarify the responsibilities of plan sponsors and fiduciaries, providing protection from liability when adhering to specific guidelines. Fiduciary Safe Harbor provisions have been updated periodically to address evolving retirement plan management practices and regulatory changes. Section 404(c) of ERISA provides a Fiduciary Safe Harbor for plan sponsors who comply with specific requirements. 404(c) Compliance relieves plan fiduciaries from liability for participants' investment decisions if specific requirements are met. Protection from fiduciary liability for participants' investment decisions Encouragement of participant engagement in retirement planning Providing participants with a broad range of investment options Offering sufficient information for informed decision-making Permitting participants to exercise control over their investments Qualified Default Investment Alternatives (QDIAs) are investment options that plan sponsors can select as the default investment for participants who do not make an election. QDIAs are designed to provide participants an appropriate default investment option, balancing risk and return. Target-date funds plan sponsors Balanced funds Managed accounts Plan sponsors must follow a prudent process to select and monitor QDIAs, ensuring they remain appropriate for participants. Fiduciary relief provisions provide protection for plan sponsors and fiduciaries who comply with specific requirements. These provisions protect fiduciaries from liability if they follow a prudent process and meet specific requirements. Fiduciary relief provisions protect fiduciaries from liability for investment performance and participant investment decisions, provided they meet the requirements of the applicable provisions. Fiduciary relief provisions do not provide absolute protection, as fiduciaries are still responsible for selecting and monitoring investments, maintaining plan documentation, and adhering to other ERISA requirements. A prudent process is essential for fiduciaries to fulfill their responsibilities and achieve Fiduciary Safe Harbor protection. An Investment Policy Statement (IPS) is a critical document that outlines the investment objectives, risk tolerance, and guidelines for a retirement plan. Developing and adhering to an IPS ensures that fiduciaries follow a consistent investment management process. Fiduciaries must implement a prudent process for selecting, monitoring, and reviewing investment options. This includes regularly reviewing investment performance, fees, and overall suitability for plan participants. Maintaining thorough documentation is essential for demonstrating a prudent process. Fiduciaries should retain records of investment decisions, meetings, and other relevant plan-related activities. Effective communication and education ensure that plan participants understand their investment options and make informed decisions. Plan sponsors must provide participants with essential information, such as plan features, investment options, and fees, allowing them to make informed decisions about their retirement savings. Providing participants with educational resources and tools can help them better understand their investment options, retirement planning, and overall financial wellness. Regular oversight and review help fiduciaries maintain compliance with Fiduciary Safe Harbor provisions and ensure that the retirement plan remains suitable for participants. Fiduciaries should conduct periodic plan reviews to assess investment performance, fees, compliance with ERISA requirements, and participant engagement. Benchmarking against industry standards and peer groups can help fiduciaries evaluate their retirement plan's effectiveness and identify improvement areas. Engaging professional advisors or consultants can help fiduciaries navigate complex regulatory requirements and implement best practices for retirement plan management. Fiduciaries must be aware of their responsibilities' potential risks and liabilities. Fiduciary breaches occur when fiduciaries fail to fulfill their duties, leading to potential liability and consequences for the plan sponsor. Failure to follow the IPS Inadequate investment selection and monitoring Failure to communicate and educate participants Fiduciary breaches can lead to penalties, litigation, and reputational damage. Retirement plan fiduciaries may face lawsuits and litigation if they fail to uphold their duties. Excessive fees Poor investment performance Failure to follow ERISA requirements Implementing a prudent process, maintaining thorough documentation, and following Fiduciary Safe Harbor provisions can minimize the risk of litigation. Fiduciary safe harbor provisions are guidelines designed to encourage responsible behavior by fiduciaries while protecting them from legal claims. Best practices for fiduciary safe harbor compliance include establishing a prudent process, providing essential information and educational resources to plan participants, and conducting periodic plan reviews. Fiduciaries must also be aware of their potential risks and liabilities, such as fiduciary breaches, lawsuits, and litigation, and implement strategies to minimize these risks. Overall, following fiduciary safe harbor provisions and best practices can help retirement plan fiduciaries fulfill their responsibilities and protect plan participants' retirement plan benefits.What Is a Fiduciary Safe Harbor?

Example of Fiduciary Safe Harbor

Background of Fiduciary Safe Harbor

The Employee Retirement Income Security Act (ERISA)

Key Provisions of ERISA

The Role of ERISA in Fiduciary Responsibilities

Development of Fiduciary Safe Harbor Provisions

Regulatory History

Amendments and Updates

Fiduciary Safe Harbor Provisions

404(c) Compliance

Definition and Purpose

Benefits of Compliance

Requirements for 404(c) Compliance

Qualified Default Investment Alternatives (QDIAs)

Definition and Purpose

Types of QDIAs

QDIA Selection and Monitoring

Fiduciary Relief Provisions

Definition and Purpose

Scope of Relief

Limitations

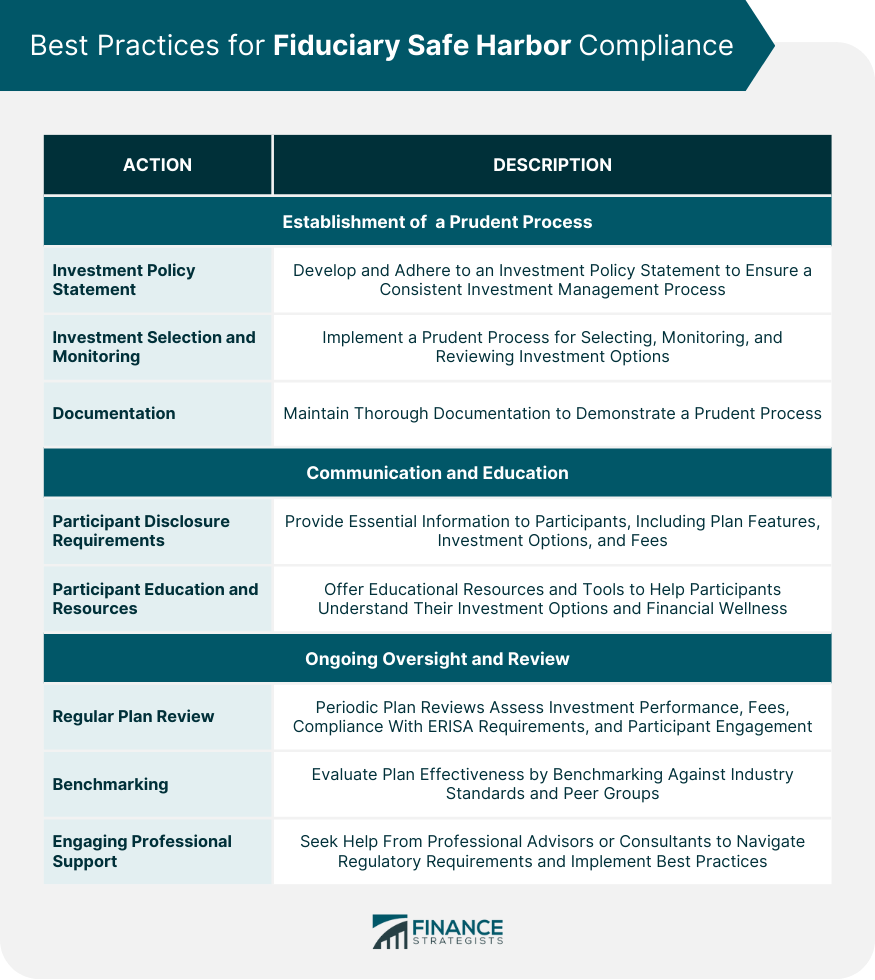

Best Practices for Fiduciary Safe Harbor Compliance

Establishment of a Prudent Process

Investment Policy Statement

Investment Selection and Monitoring

Documentation

Communication and Education

Participant Disclosure Requirements

Participant Education and Resources

Ongoing Oversight and Review

Regular Plan Review

Benchmarking

Engaging Professional Support

Potential Risks and Liabilities of Fiduciaries

Fiduciary Breaches

Types of Breaches

Consequences of Breaches

Lawsuits and Litigation

Common Causes of Fiduciary Litigation

Strategies to Minimize Risk

Conclusion

Fiduciary Safe Harbor FAQs

The Fiduciary Safe Harbor provision is a set of rules established by the Employee Retirement Income Security Act (ERISA) to protect fiduciaries from liability for certain investment decisions made on behalf of a retirement plan.

Generally, plan fiduciaries who satisfy the Fiduciary Safe Harbor provision requirements are protected from liability for certain investment decisions related to retirement plans.

To qualify for the Fiduciary Safe Harbor provision, fiduciaries must follow specific guidelines outlined in ERISA, such as providing investment options with varying degrees of risk and return and following a predetermined process for selecting investments.

The Fiduciary Safe Harbor provision helps ensure that plan fiduciaries act prudently in selecting and monitoring investments for retirement plans, which can help protect plan participants from poor investment outcomes.

Yes, fiduciaries can still be held liable for investment decisions that do not meet the Fiduciary Safe Harbor provision requirements or that breach their fiduciary duties under ERISA. However, meeting the requirements of the Safe Harbor can be strong evidence that the fiduciary has acted prudently.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.