Fiduciary Liability Insurance is a specialized type of insurance designed to protect individuals and organizations that act as fiduciaries in managing employee benefit plans, pensions, trusts, or investments. The coverage protects against financial losses and legal expenses resulting from alleged breaches of fiduciary duty, errors, or omissions in the administration and management of these plans or assets. Fiduciary Liability Insurance plays a crucial role in safeguarding fiduciaries from potential financial and reputational damage arising from legal claims. Given the complex nature of fiduciary responsibilities and the potential for high-stakes litigation, having adequate insurance coverage can be vital for organizations and their fiduciaries.' This type of coverage is designed for fiduciaries who manage and administer employee benefit plans, including pension, health, and welfare benefit plans. It protects against claims arising from alleged mismanagement or breaches of fiduciary duty. Investment Advisor Fiduciary Liability Insurance covers individuals and firms that provide investment advice to clients, including financial planners, wealth managers, and registered investment advisors. The coverage protects against claims arising from alleged fiduciary breaches or errors in providing investment advice. Trustee Fiduciary Liability Insurance is designed for individuals and organizations that act as trustees for personal trusts, estates, or other types of trust. The coverage protects trustees against legal liability stemming from alleged mismanagement or breaches of fiduciary duty in the administration of the trust. Non-Profit Fiduciary Liability Insurance covers board members, officers, and other key personnel of non-profit organizations who may have fiduciary duties related to the management of the organization's assets or employee benefit plans. Private companies may also have fiduciary responsibilities, particularly in relation to employee benefit plans, pensions, or the management of company assets. Fiduciary Liability Insurance can protect these entities from potential claims arising from alleged mismanagement or breaches of fiduciary duty. Fiduciary Liability Insurance provides coverage for claims alleging a breach of fiduciary duty, errors, or omissions in the management and administration of employee benefit plans or other fiduciary activities. The policy covers the cost of legal defense, including attorney fees, court costs, and other expenses associated with defending against a fiduciary breach claim. Fiduciary Liability Insurance indemnifies the insured for any settlements or judgments resulting from covered claims, subject to policy limits and deductibles. The policy may also cover regulatory penalties and fines imposed by governmental agencies for violations of applicable laws and regulations related to fiduciary activities. Some policies include coverage for the costs associated with voluntary compliance programs, such as correcting plan errors or implementing remedial measures to address fiduciary breaches. A fiduciary has a duty to act in the best interests of the plan participants or beneficiaries. A breach of this duty may occur if a fiduciary puts their interests or those of a third party above those of the plan participants or beneficiaries. Fiduciaries must exercise the care, skill, prudence, and diligence that a prudent person would use under similar circumstances. A breach of the duty of care can occur when a fiduciary fails to properly manage or administer the plan or assets. Fiduciaries are required to act prudently when making decisions on behalf of plan participants or beneficiaries. A breach of the duty of prudence may arise from a failure to diversify investments, inadequate due diligence, or other imprudent actions. Fiduciaries must avoid engaging in prohibited transactions, such as self-dealing, conflicts of interest, or transactions that benefit the fiduciary at the expense of the plan or its participants. Prohibited transaction claims can result in significant financial penalties and legal liability. Fiduciaries have a duty to monitor and evaluate the performance of service providers, such as investment managers, recordkeepers, and consultants. A failure to properly monitor these service providers can result in fiduciary breach claims. The type and size of an organization can impact insurance premiums, as larger organizations or those with more complex benefit plans may face higher risks and require more coverage. The type and size of the benefit plans being managed can also affect premiums, as certain types of plans, such as defined benefit pension plans, may present greater risks than others. A history of prior claims, particularly those involving fiduciary breaches or litigation, can result in higher premiums for fiduciary liability insurance. Organizations with strong internal controls and governance practices are often seen as lower risks by insurers, which can result in lower premiums. Higher coverage limits and lower deductibles will generally result in higher premiums, as the insurer assumes more risk. Implementing robust governance practices can help minimize the risk of fiduciary breaches and related claims. This may include establishing clear policies and procedures, maintaining documentation, and conducting regular audits or reviews. Fiduciaries should regularly monitor and evaluate the performance of the plans and assets they manage, as well as the performance of service providers, to ensure that they are acting in the best interests of plan participants or beneficiaries. Providing ongoing training for key personnel on fiduciary duties and responsibilities can help ensure that they understand their roles and are equipped to manage potential risks. Selecting experienced and competent service providers with strong track records can help mitigate the risk of fiduciary breaches and related claims. Maintaining thorough documentation of fiduciary decisions and actions can provide a record of the fiduciary's efforts to act in the best interests of plan participants or beneficiaries, which can be valuable in the event of a claim. Organizations should carefully assess their coverage needs and limits based on the type and size of their organization, the benefit plans they manage, and the potential risks they face. It is important to ensure that coverage limits are sufficient to address potential claims and legal expenses. Comparing different policies and insurance carriers can help organizations find the best fit for their needs. It is important to consider factors such as policy coverage, exclusions, endorsements, and the reputation and financial stability of the insurance carrier. Organizations should carefully review any policy exclusions and endorsements to ensure that they understand the scope of coverage provided. Exclusions may limit coverage for certain types of claims, while endorsements may provide additional coverage or modify the terms of the policy. Organizations can potentially lower their insurance premiums by negotiating with insurance carriers, particularly if they have strong internal controls, governance practices, and a favorable claims history. Additionally, organizations may consider adjusting deductibles to balance premium costs with the level of risk they are willing to assume. It is important for organizations to periodically review their fiduciary liability insurance policies to ensure that coverage remains adequate and up to date. Changes in the organization's structure, benefit plans, or regulatory environment may necessitate adjustments to coverage limits, policy terms, or endorsements. Fiduciary Liability Insurance is an essential tool for protecting fiduciaries from the financial and reputational risks associated with legal claims alleging breaches of duty, errors, or omissions. Having the right coverage in place can help to ensure that fiduciaries can focus on fulfilling their responsibilities without the fear of potentially devastating financial consequences. By encouraging the implementation of strong governance practices and risk management strategies, Fiduciary Liability Insurance can also play a role in promoting the overall health and stability of organizations and their benefit plans. Finally, it is important for organizations to regularly review and update their Fiduciary Liability Insurance policies to ensure that they remain adequately protected against the evolving risks and challenges that come with serving as a fiduciary.What Is Fiduciary Liability Insurance?

Types of Fiduciary Liability Insurance

Pension and Welfare Benefit Plan Fiduciary Liability

Investment Advisor Fiduciary Liability

Trustee Fiduciary Liability

Non-profit Fiduciary Liability

Fiduciary Liability for Private Companies

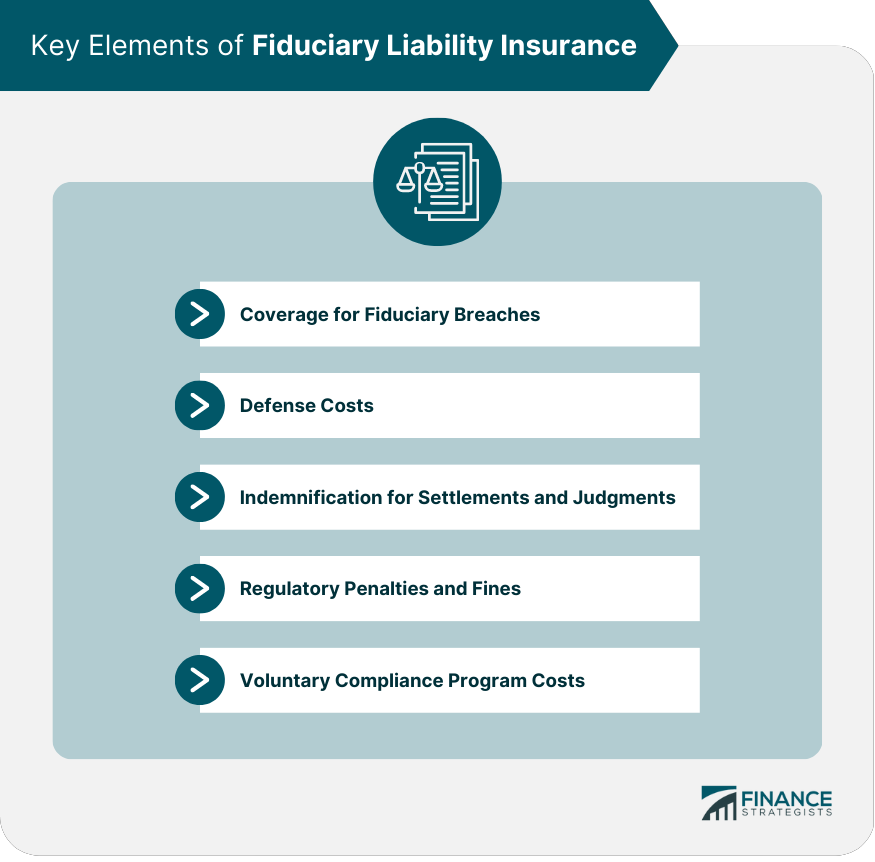

Key Elements of Fiduciary Liability Insurance

Coverage for Fiduciary Breaches

Defense Costs

Indemnification for Settlements and Judgments

Regulatory Penalties and Fines

Voluntary Compliance Program Costs

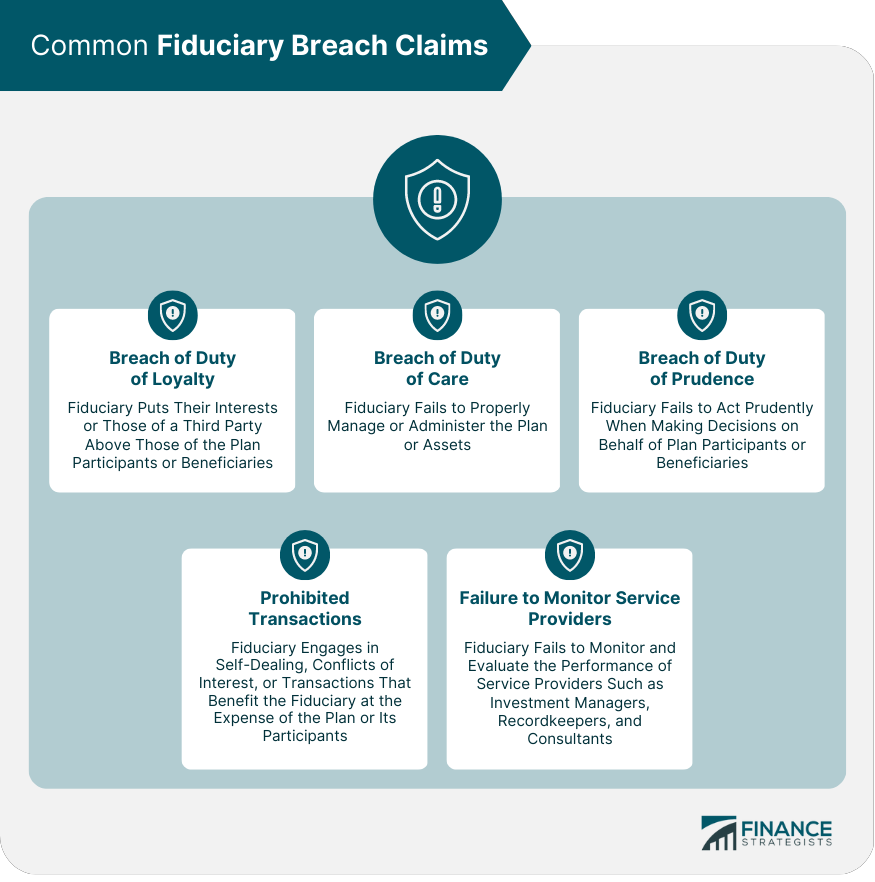

Common Fiduciary Breach Claims

Breach of Duty of Loyalty

Breach of Duty of Care

Breach of Duty of Prudence

Prohibited Transactions

Failure to Monitor Service Providers

Factors Affecting Fiduciary Liability Insurance Premiums

Type and Size of Organization

Type and Size of Benefit Plans

Claims History

Internal Controls and Governance Practices

Coverage Limits and Deductibles

How to Minimize Fiduciary Liability Risks

Developing and Implementing Strong Governance Practices

Regularly Monitoring and Evaluating Plan Performance

Providing Ongoing Fiduciary Training for Key Personnel

Engaging Competent and Experienced Service Providers

Documenting All Fiduciary Decisions and Actions

Choosing the Right Fiduciary Liability Insurance Policy

Assessing Coverage Needs and Limits

Comparing Policies and Insurance Carriers

Evaluating Policy Exclusions and Endorsements

Negotiating Premiums and Deductibles

Reviewing Policies Periodically

Conclusion

Fiduciary Liability Insurance FAQs

Fiduciary liability insurance is a type of insurance that provides coverage for claims arising from breaches of fiduciary duties in the administration of employee benefit plans. This insurance is designed to protect plan fiduciaries, such as plan administrators and trustees, from personal liability in the event of a lawsuit.

Any person or entity that serves as a fiduciary for an employee benefit plan, such as a retirement plan or health plan, should consider obtaining fiduciary liability insurance. This includes plan administrators, trustees, investment managers, and other plan fiduciaries.

Fiduciary liability insurance typically covers claims arising from breaches of fiduciary duties, such as claims for errors in plan administration, conflicts of interest, and breaches of duty of loyalty. The insurance may also provide coverage for legal defense costs, settlements, and judgments.

The cost of fiduciary liability insurance can vary depending on factors such as the size of the plan, the types of assets held in the plan, and the level of risk associated with the plan's investments. Generally, the cost of the insurance is based on the amount of coverage requested and the risk profile of the plan fiduciaries.

Fiduciary liability insurance is often required by the Employee Retirement Income Security Act (ERISA) for plan fiduciaries. While ERISA does not specifically require fiduciary liability insurance, it does require fiduciaries to act prudently and to protect the interests of plan participants. Fiduciary liability insurance is one way for fiduciaries to mitigate the risk of personal liability in the event of a lawsuit.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.