Financial advisors and registered investment advisors (RIAs) can be either “fee-only” or “fee-based.” With fee-only financial advisors, the management fee is where the client’s fees end, whereas, for fee-based advisors, the management fee is where those fees begin. Fee-only financial advisors cannot legally receive compensation for the investments they recommend. Fee-based financial advisors are allowed to receive compensation on investments they recommend but must disclose whether a conflict of interest exists. Practically speaking, this might take the form of investing a client’s money into a mutual fund, which provides the advisor with a kickback on the management fee that they charge the client. The advisor may charge a 1% management fee, but by investing the client’s money with a specific mutual fund, the advisor may receive an additional 0.1% fee (10 basis points) on the client’s assets. Have a financial question? Click here. The fiduciary standard exists for both fee-only and fee-based financial advisors. The fiduciary standard states that advisors must act in the best interests of their clients. The fiduciary standard contrasts with the suitability standard, which states that advisors must make a “suitable” recommendation, rather than a recommendation that is in the client’s best interests. Financial advisors operate based on trust when functioning as counselors in matters pertaining to one's finances. Although they are legally obligated to reveal any conflicts of interest, financial advisors can easily convince clients that the investments they recommend are in the client’s best interest due to the high degree of trust their role entails. Unfortunately for the client, it can be very difficult to prove that their financial advisor did not act in their best interest when recommending an investment. For this reason, it is best to work with a financial professional who has removed any conflicts of interest by operating as a fee-only financial advisor. You can tell if a financial advisor is fee-only by looking at Item 5.E.(5) under “Compensation Arrangements” of the firm’s most recent Form ADV filed with the SEC. If there is no checkmark next to “Commissions,” then the RIA (Registered Investment Advisory) firm is a fee-only financial advisory firm that cannot receive a commission on investments they recommend. Below is a screenshot of a fee-only RIA’s Form ADV filing: Visit the SEC’s IAPD website at https://adviserinfo.sec.gov/. Type in the firm or advisor you would like to research. If you would like to look up a firm, change the tab at the top from “individual” to “firm.” After selecting “search,” choose the correct individual or firm. The Form ADV can only be found on the firm’s profile. Select “View Latest Form ADV Filed” to view the firm’s Form ADV (highlighted below). Scroll down to “Compensation Arrangements” under Item 5 within the firm’s most recently filed Form ADV. If the box next to “Commissions” is checked, then the firm is fee-based. If the box is not checked, then the firm is fee-only. Some financial advisors require minimum investments for them to manage your account. This can be a deterrent for some people, especially if you are just starting out and do not have a lot of money to invest. You can check whether a firm has investment minimums by looking at the firm’s website, or by checking their Part 2 Firm Brochure: Typically, firms will list their required account minimums under Item 7: “Types of Clients.” Refer to the brochure’s table of contents to find what page Item 7 is on. Often firms are willing to make an exception if a client is close to their account minimum, or if the individual was referred by an existing client, such as a client’s child. If you do not meet a firm’s account minimum, many advisors do not have investment minimums. The client-to-advisor ratio is the number of clients that an advisor has compared to the number of advisors at the firm. The best way to determine whether an advisor is already stretched thin by their existing clients is to simply ask the advisor how many accounts they are currently managing. If an advisor already has a full book of business (say, over 100 clients), it may be difficult for them to give you the attention you need. A firm’s overall client-to-advisor ratio can be calculated by taking the number of advisors at the firm (Item 5.B.(1) on Form ADV) and dividing it by the number of accounts (Item 5.F.(2).(f) on Form ADV). Be careful when calculating a client-to-advisor ratio, since adding up the total number of clients divided by the total number of advisors may not be reflective of the individual advisor in question. Many of the accounts may also be a part of the firm’s robo-advisor offering. Checking the services offered by a firm is also an important consideration when evaluating them. Some firms can have significantly deeper offerings than others. Nearly all firms offer investment management, although some only offer hourly financial planning. Some offer comprehensive wealth management, which includes the creation of a financial plan, determining the correct asset allocation to meet your financial goals, and managing your assets. Some firms are only a custodian of the assets and do not offer financial planning. A custodian is a firm that holds the client’s assets. Firms with a more robust offering will also include tax planning and estate planning. This is often available only to high-net-worth individuals, such as those who have more than $1 million in investments. In some cases, a firm may not show that they offer tax and estate planning on Item 6.A.(12) and 6.A.(13) of their Form ADV, but they may still offer it to clients by subcontracting out the work to a partnering CPA or law firm. Here’s an example of a firm that offers tax and estate planning to clients, but does not have any such boxes checked on their Form ADV: The services a firm offers can typically be found on its website. A firm with a large number of assets under management can be an indicator that they are more trustworthy and established. A larger firm may also offer more support to its financial advisors than a smaller firm, both technologically and with teams that help make the client successful (such as a financial planning team). Additionally, a firm that is growing its assets under management is also a good sign that the firm has high retention rates and services its clients well. Like anything in life, the more experience someone has, the better they tend to be at it. While this factor is by no means the only one that should be considered, typically, the more experience, the better. Be mindful that an advisor nearing their retirement age may retire and pass you on to a junior advisor. Typically, advisors give plenty of notice and will involve the new advisor in client meetings before transferring their book of business. Additionally, it is preferable to find an advisor who has experience with your situation. For example, you may be a widow or a business owner looking to transfer your business to your children in the most tax-efficient way possible. If an advisor works with a clientele similar to you, this is a sign that they may be better equipped to help with your specific situation. Having higher fees is not necessarily a bad sign. This may mean that they provide deeper services than other firms, such as tax and estate planning. In fact, Forbes/SHOOK Research scores firms higher for having higher fees. A common management fee for wealth management services is around 1%. If the firm has a robo-advisor offering, management fees are typically lower. A fee schedule is the management fee at varying amounts managed by the firm, with higher amounts invested typically receiving a lower management fee as a percentage of the assets managed. A firm’s fee schedule can be found in the brochure they file with the SEC (and is sometimes published somewhere on the firm’s website). There are different fee schedules based on whether the account is discretionary or non-discretionary, as well as what type of assets are held in the account. Discretionary accounts allow the firm to buy and sell securities at their discretion, whereas a non-discretionary account means the firm must first get approval from the client before buying or selling on their behalf. An advisor must hold the proper designations and licenses that make them eligible to help with your unique needs. If an advisor is executing trades on a client’s behalf, they must hold a Series 63 license and either a Series 6 or Series 7 license. All advisors receiving compensation for financial advice must hold a Series 65 license, or a CFP® designation that fulfils this requirement. For advisors offering financial planning, the CFP® (Certified Financial Planner™) designation is the gold standard, although many other designations exist. The CFA® (Chartered Financial Analyst) charter is the preferred designation for those buying and selling securities on behalf of a firm. For tax-related needs, a financial professional should be a CPA (Certified Public Accountant) or EA (Enrolled Agent). As mentioned previously, many other designations also exist. However, these designations represent the highest standard available for the needs mentioned above. It is easy to make the mistake of hiring a financial advisor based on their likeability, common interests, or alma mater, rather than their qualifications, expertise, and the way they are compensated. Qualitative variables are still important. How trustworthy an advisor seems, or how well they understand the nuances of your goals and financial situation, plays a critical role in the advisor successfully helping their clients. The recommendations on how to evaluate a financial advisor laid out in this article should be complemented by qualitative research, including the trustworthiness of the friend who may have referred their advisor or the advisor’s overall competency and experience. Hopefully, this guide has provided you with new ways to objectively evaluate the plethora of financial advisors ready to take on new clients. To find a financial advisor in your area, search your location using the Finance Strategists financial advisor search tool.Fee-Only vs Fee-Based Financial Advisors

The Fiduciary Standard

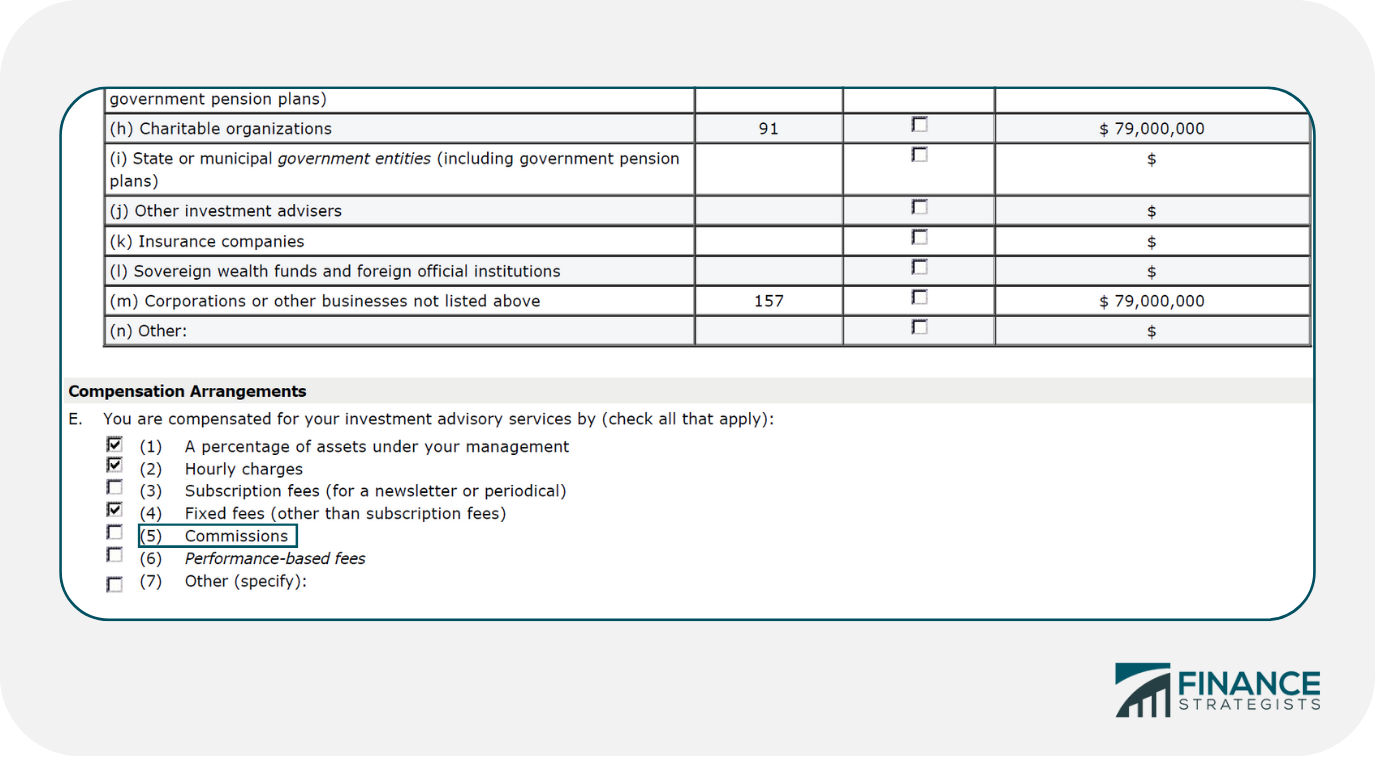

How You Can Tell if a Financial Advisor is Fee-Only

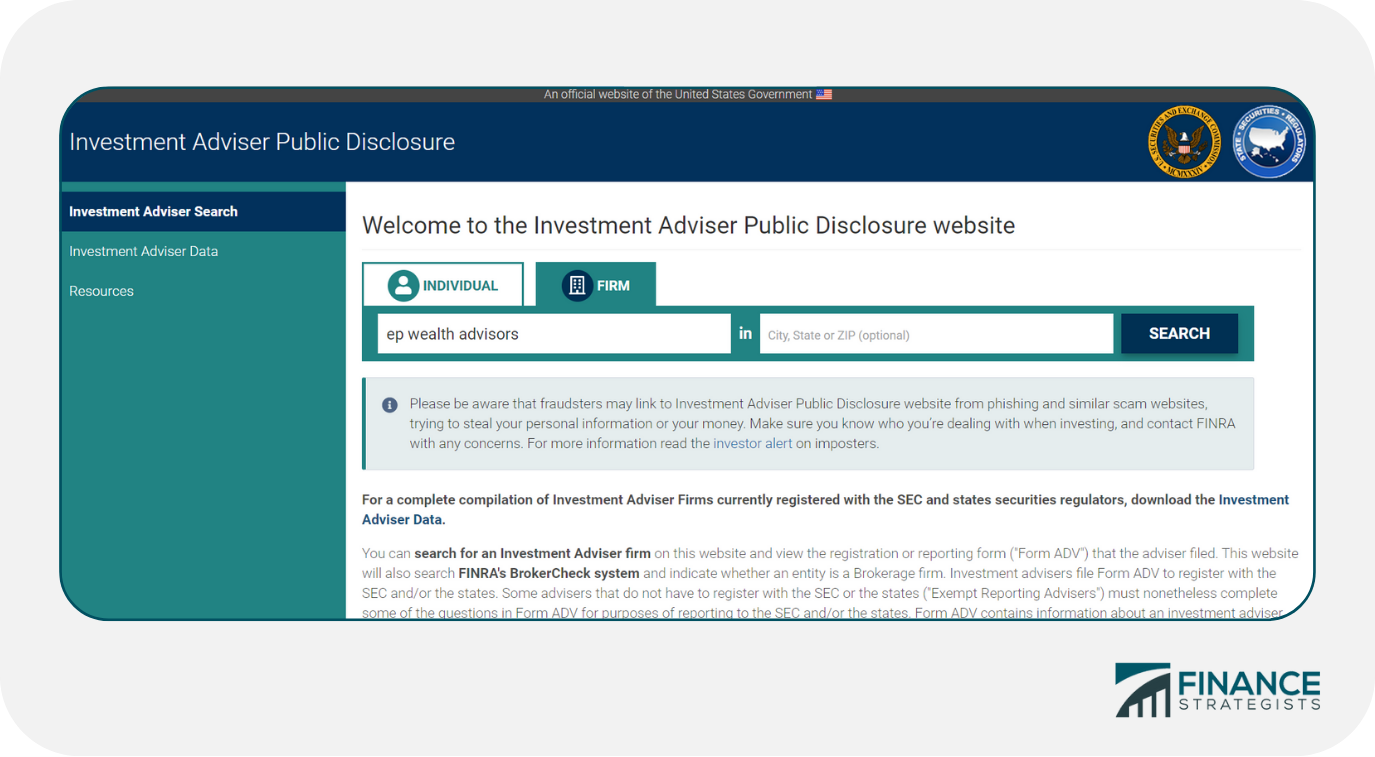

How to Look Up a Firm Using the SEC’s Investment Adviser Public Disclosure (IAPD) Website

Step 1 - Visit SEC Website

Step 2 - Search Firm

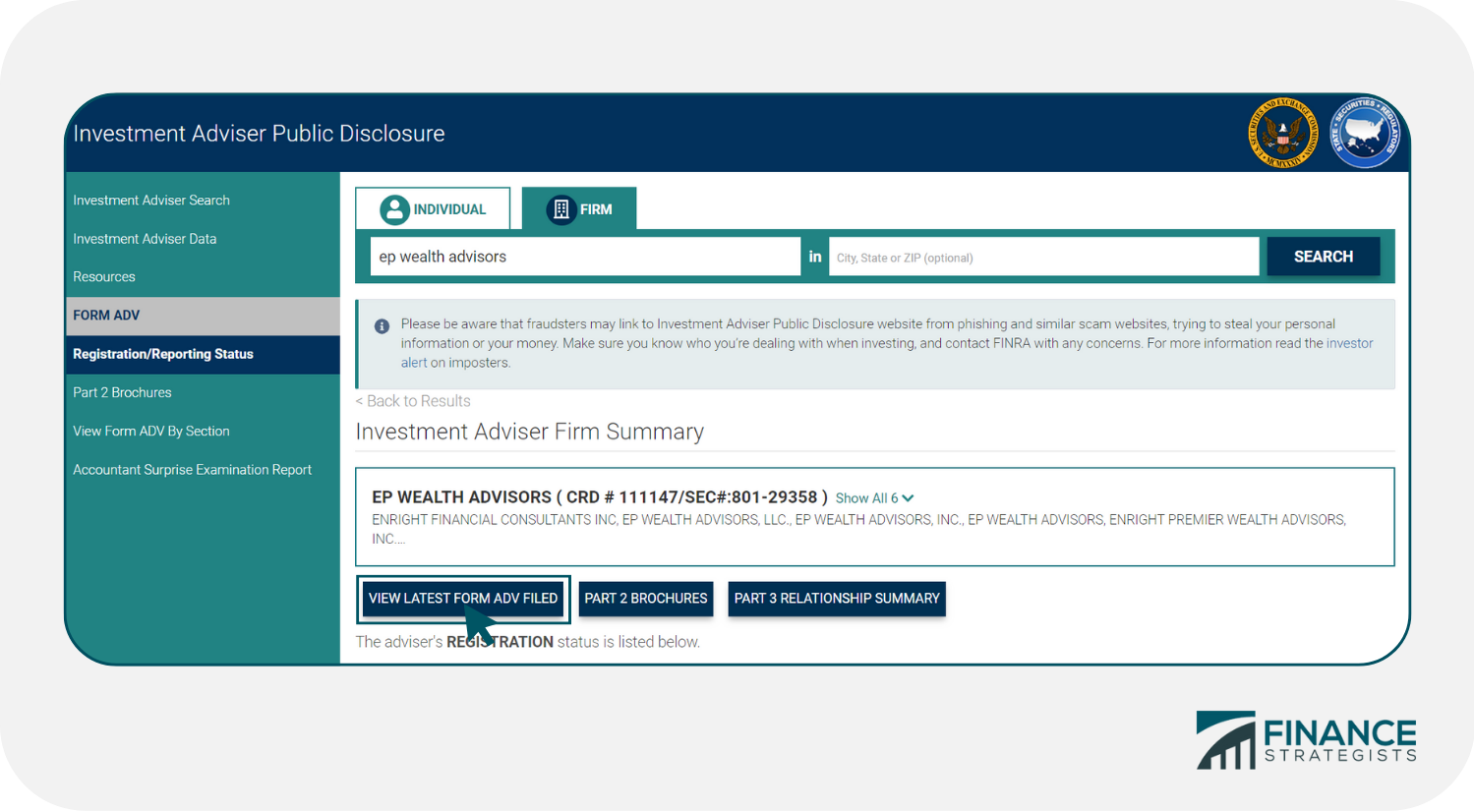

Step 3 - Select View Latest Form ADV Filed

Step 4 - Scroll Down to Item 5.E.(5) Under “Compensation Arrangements”

Other Things to Consider When Evaluating Financial Advisors

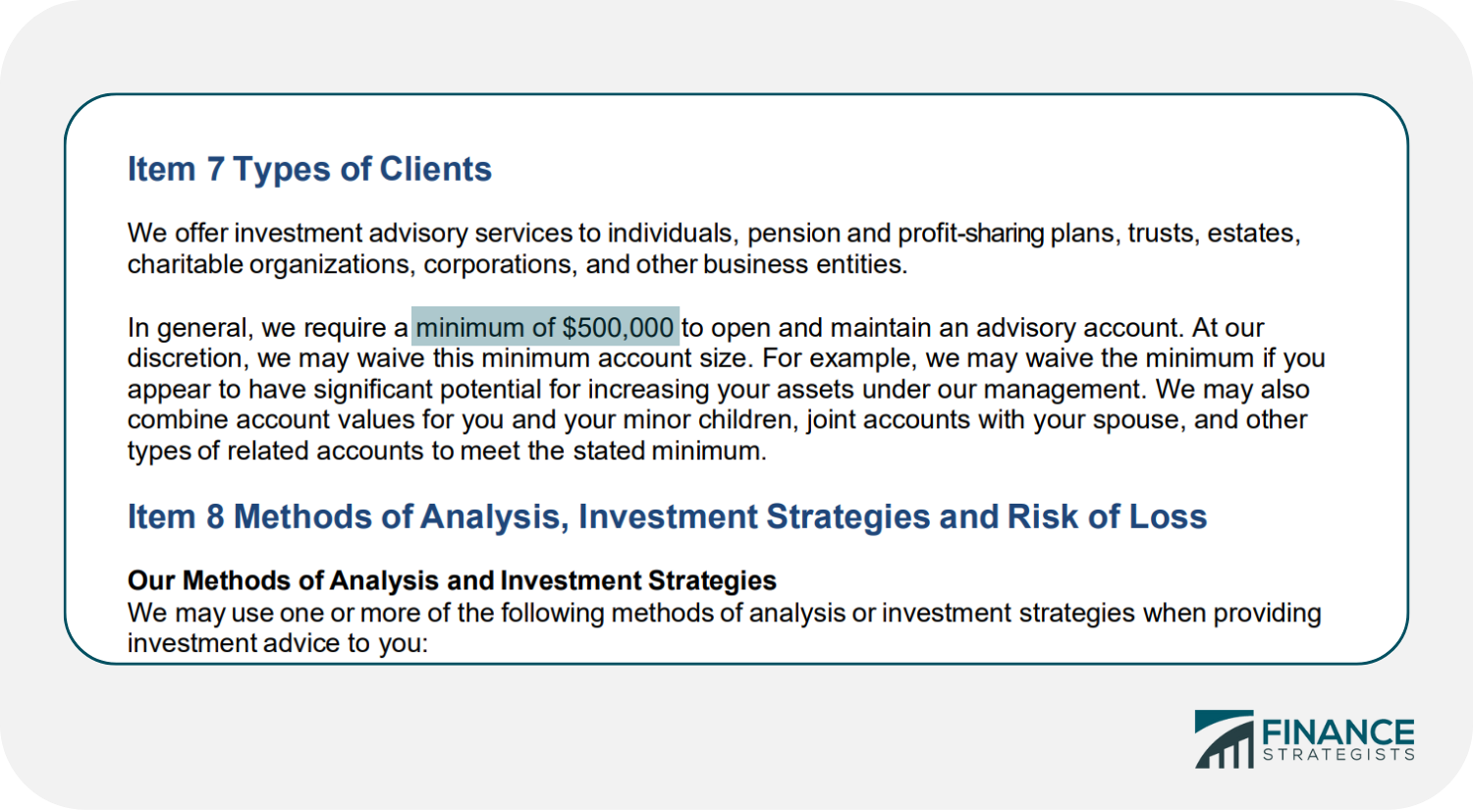

Investment Minimums

Client-to-Advisor Ratio

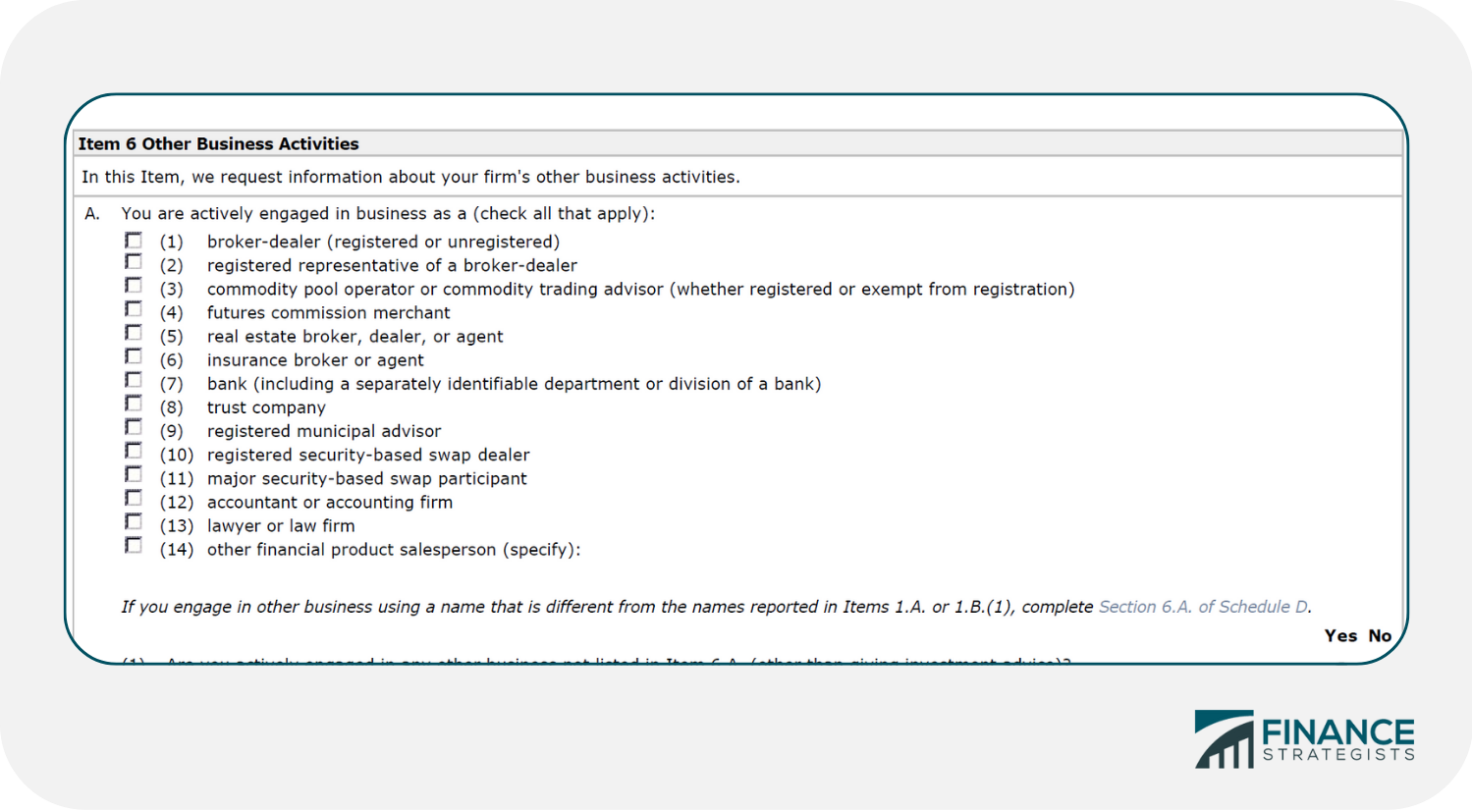

Services Offered

Assets Under Management

Experience

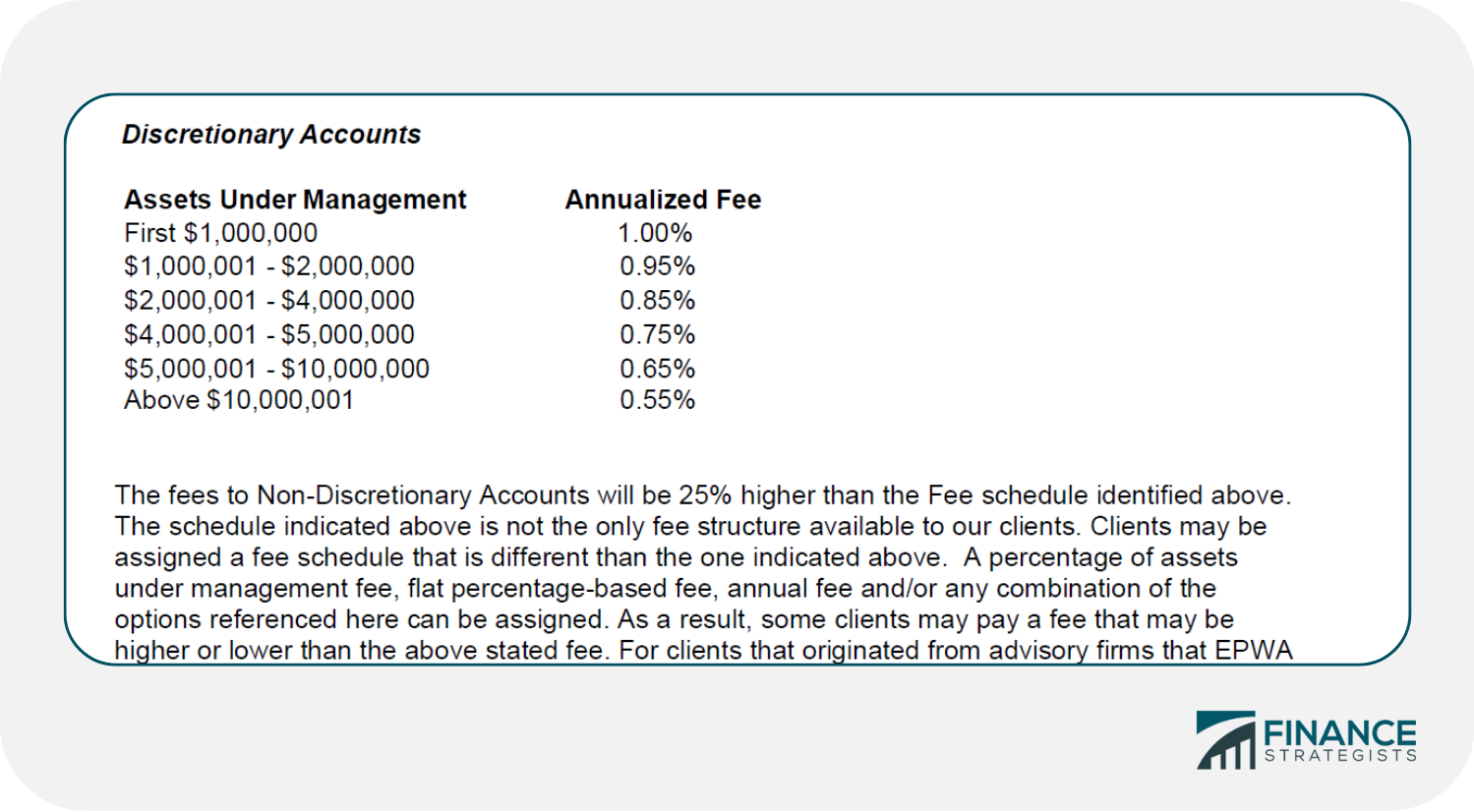

Fees and Fee Schedule

Advisor’s Professional Designations

Licenses

Designations

The Bottom Line

How to Tell if a Financial Advisor Is Fee-Only FAQs

Fee-only financial advisors are compensated solely by their clients' fees. They do not receive commissions from the sale of financial products.

Fee-based financial advisors are compensated by both fees and commissions. This means that they may receive commissions from the sale of financial products, in addition to the fees that their clients pay them.

Some other things to consider when hiring a financial advisor include: - The types of services you are looking for - The advisor's investment philosophy - The advisor's experience and credentials - The size of the firm - The client-to-advisor ratio

A financial planner is a type of financial advisor who provides comprehensive financial planning services. Financial advisors can provide a variety of services, including investment advice, but not all of them offer comprehensive financial planning.

There are many different financial advisor designations, but some of the most popular ones include the Certified Financial Planner (CFP®) designation, the Chartered Financial Analyst (CFA®) designation, and the Certified Public Accountant (CPA) designation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.