Fee-only financial advisors are paid a set fee for services like advising on personal finances, investments, retirement planning, estate planning, taxes, and insurance. They do not receive any type of commission from the sale of products they are advising on. This helps ensure that their primary focus is on providing sound financial guidance that is in their client’s best interest rather than seeking to make a profit through product sales. They are paid directly from their clients through hourly fees or a flat percentage based on assets under management (AUM). Depending on the service provided, they can earn from retainer or flat fees. They differ from fee-based advisors because they do not receive compensation from third parties for recommending certain products, such as mutual funds or annuities. Fee-only advisors generally adhere to a fiduciary standard. Fee-based advisors, especially those registered with the Securities and Exchange Commission (SEC), also adhere to fiduciary standards when acting as advisors. However, the suitability standard generally applies when they sell products. The cost of a fee-only advisor depends on the complexity of the advice sought and will likely vary depending on factors such as location, years of experience, and the type of service provided. Fees can range from an hourly rate, a retainer fee, an AUM percentage, or a flat fee. This fee structure is best for clients who do not need a comprehensive financial plan or ongoing advice. A fee-only advisor can charge anywhere from $100 to $500 per hour depending on their location, qualifications, experience, and expertise. An advantage of the hourly fee structure is that it allows you to pay for the exact advice and services you need without committing to a long-term relationship. It also gives you more control over your finances since you can choose when and how much to invest in financial planning services. A retainer fee, or an ongoing management fee, is paid to the advisor on a regular basis for continued financial planning and advice. Retainers generally range anywhere from $1,000 to $8,000 annually, depending on the complexity of the advice sought. This is best if your financial goals and plans change frequently or require frequent monitoring. Your advisor will be able to get to know you and understand your financial situation better, making it easier for them to provide personalized advice and guidance. Additionally, since the retainer fee is paid upfront, there is no need for your advisor to increase the number of trades or other activities to make more money. This gives them more time and flexibility to focus on providing you with quality advice. This usually ranges from 0.5% to 2% annually, depending on how much money and other assets are managed by the advisor. The percentage charged tends to decrease as the amount of AUM increases. For example, a fee-only advisor may charge a 1% AUM fee on investments up to $500,000 and 0.75% for investments over $500,000. AUM percentage is ideal if you have a large portfolio that requires ongoing management. In this case, it is more cost-effective than hourly or retainer fees. This fee structure encourages advisors to focus on achieving long-term results for their clients since their earnings are tied to their performance. This incentivizes them to give sound advice and ensure any investment changes are properly monitored over time. This is a one-time payment for a comprehensive financial plan or other specialized services such as estate planning. The cost will vary depending on the complexity of the services sought and can range from $1,000 to $3,000 or higher. The advantage of a flat fee is knowing exactly how much you will need to pay upfront for your financial planning needs. This helps avoid any surprises in terms of costs and makes budgeting for such services easier. It also removes the incentive for advisors to push their clients into investing in products that may be more lucrative for them since they are paid a flat fee regardless of what investments are made. This ensures the advisor always looks out for their client’s best interests. A complete disclosure of the financial advisor’s conflicts of interests and fee policies can be viewed on the Investment Adviser Public Disclosure website. The site contains registration and reporting details that financial advisors are required to file with the agency before setting up shop for clients. The ADV form provides comprehensive information about the advisor’s business, including description of services offered, explanation of fees, billing practices, and past criminal history, if any. Specific information within the form is designed to alert clients about details relating to the financial advisor’s dealings with the ecosystem that they operate in. There are three parts to the form. The first part provides ownership information about the advisory firm. Part II asks the applicant to create a narrative brochure with information about the firm. They are also required to provide brochure supplements pertaining to their business in this part. The final part consists of a relationship summary in which the advisor discloses their relationships with investment firms, fees received from these and other companies, and potential conflicts of interest in their business. Thorough evaluation of the ADV form can reveal relationships between advisors and related parties. Conflict of interest is minimized when working with a fee-only advisor. Other benefits include ensured fiduciary responsibility, unbiased and objective advice, and a transparent fee structure. Fee-only financial advisors are not compensated for selling any financial product or services. They do not receive commissions, bonuses, or incentives for selling products. This ensures that their advice is not biased towards increasing their own profit. They will work and recommend investments, products, assets, or strategies that provide the highest benefit without ulterior motives. They only serve to benefit the client. Eliminated conflict of interest leads to ensured fiduciary responsibility. A fiduciary is a person who has been entrusted with another’s money, assets, or property. As such, they are legally required to act in their client's best interest at all times. Since fee-only advisors do not have any incentive to sell products and services and get paid solely through fees charged to their clients, they can be trusted to put the interests of their clients first. Since they are fiduciary and have no conflict of interest, you can be more confident with their advice. The fee-only advisor will provide you with various options without any financial incentive or pressure to choose one particular option over another. They can be more objective and unbiased when recommending investments and strategies, as they are not tied to any financial product or service. Fee-only advisors make their fee structure clear upfront so that clients know what they are paying for. They can charge by the hour or through a retainer, collect a percentage of total assets managed, or ask for a flat fee depending on the service provided. This helps prevent any misunderstandings or hidden fees down the line. It also allows you to compare different fee-only advisors more easily and select the one that best fits your needs and budget. Despite said benefits, working with fee-only financial advisors also comes with some drawbacks, mainly related to higher costs and limited products and services. Fee-only advisors may not be the most cost-effective option as they can be significantly more expensive compared to other financial advisors. This is because their services are typically not bundled with any products and thus incur additional costs. Because they are usually paid based on AUM percentage, their fee can also increase as your assets grow. These charges can eat into the returns of your investments, so be sure to compare different advisors and understand what you are paying for in order to get the best value. Because fee-only advisors do not earn a commission, their services are often less varied than those offered by a fee-based advisor. Fee-only financial advisors generally focus on providing advice rather than selling products like insurance or investments. For example, a fee-based advisor might be a better option if you want insurance. This is because a fee-based advisor is more likely able to offer you a variety of insurance policies. In contrast, a fee-only advisor would only provide advice and guidance on the types of insurance that may be best for you. When deciding between a fee-only and fee-based financial advisor, it is important to consider the cost of services and what type of advice you need most. Fee-only advisors cost more, but they offer completely unbiased advice. On the other hand, fee-based advisors charge lower fees, but their advice may have a conflict of interest due to commissions earned through sales of products like insurance or investments. Fee-only advisors are held to a fiduciary standard. In contrast, fee-based advisors are only fiduciary when giving financial advice because they are generally held to a suitability standard when selling products. This means that fee-based advisors are only required to suggest and sell investments or products that are suitable for their clients, not necessarily what is best for them. In addition, fee-only advisors are generally limited in terms of providing products and sales, whereas fee-based advisors may be able to provide more comprehensive services, including product information. Fee-only advisors may be more suitable for higher-income clients, while fee-based advisors may benefit those who prefer to work with only one financial advisor. Ultimately, it is important to research and compare both options before deciding which type of financial advisor best suits your needs. Do your research. Finding a fee-only financial advisor is easy, as various online resources and directories are available. One of the most popular platforms includes the National Association of Personal Financial Advisors (NAPFA). NAPFA provides detailed information about the advisors in their network, such as location, services provided, credentials, and more. Fittingly, NAPFA requires its members to be fee-only and not charge commissions. Be sure to thoroughly research any potential financial advisor before engaging them for their services, as this will ensure that you find one that meets your needs and expectations. Fee-only financial advisors provide unbiased advice and do not receive any commissions from the products or services they offer. This can make them pricier than fee-based financial advisors, but the peace of mind provided by going commission-free is often worth it. Fee structures include hourly rates, retainer fees, AUM fees, and flat rates. These fees will also vary depending on the advisor’s location, experience, expertise, and credentials. Fee-only advisors do not have conflicts of interest, ensuring they abide by fiduciary standards and give objective advice. Their fees are also paid upfront, which increases transparency. Nonetheless, disadvantages include higher costs and limited services. Before hiring a financial advisor, carefully research them using different resources. In doing so, you can be sure that the individual you hire is best suited for your financial objectives and situation.What Is a Fee-Only Financial Advisor?

Fee Structures of Fee-Only Advisors

Hourly Rate

Retainer Fee

AUM Percentage

Flat Fee

How to Evaluate Your Fee-Only Financial Advisor

Advantages of Hiring a Fee-Only Financial Advisor

Free From Conflict of Interest

Fiduciary

Unbiased and Objective Advice

Transparent Fee Structure

Disadvantages of Hiring a Fee-Only Financial Advisor

Expensive and Favorable for Higher-Income Clients

Limited in Products or Services

Fee-Only vs Fee-Based Financial Advisors

Where to Find a Fee-Only Financial Advisor

The Bottom Line

Fee-Only Financial Advisor FAQs

Costs will depend on the type of service needed, the location, and the financial advisor’s experience and credentials. Fees range from $100-$500 per hour, $1,000-$8,000 retainer per annum, 0.5%-2% AUM per year, or a flat fee of $1,000-$3,000 or higher.

Fee-only financial advisors do not earn a commission, so they are free from conflicts of interest. They abide by fiduciary standards and give objective and unbiased advice. Their fees also provide transparency.

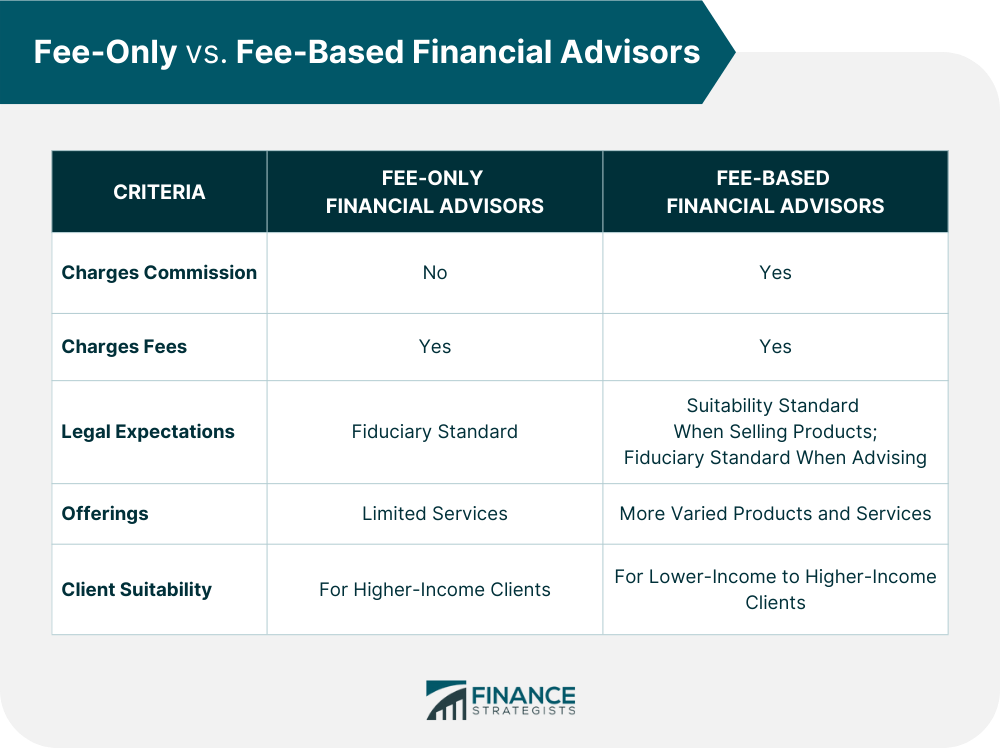

Fee-only advisors do not earn a commission, abide by fiduciary standards, offer limited services, are more expensive, and are more suited to higher-income clients. On the other hand, fee-based financial advisors earn commissions, abide by suitability standards when selling and fiduciary when advising, offer more varied products and services, and are suitable for clients of diverse income levels.

Fee-only financial advisors charge higher fees and are more suitable for higher-income clients. They also offer limited services.

Do your research. You may use online resources like the National Association of Personal Financial Advisors (NAPFA) website. Before choosing one, it is important to read about a potential financial advisor’s credentials, fee structure, location, services provided, and more.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.