A joint bank account can be opened by two or more individuals. These individuals could be friends, relatives, business partners, or couples. However, every bank has its own specific set of eligibility criteria. Most require account holders to be of legal age and possess valid identification. It is advisable to contact the bank for specific eligibility criteria before proceeding. When opening a joint bank account, all parties involved must provide personal identification documents. This typically includes proof of identity (such as a passport or driver’s license) and proof of address (like a utility bill). Some banks may also require additional documentation like social security cards or employment details. Once the joint account is opened, all account holders have equal rights to make deposits or withdrawals. The bank doesn't need the consent of all parties for transactions. This is why trust is paramount in a joint bank account relationship. In a joint account, if one account holder incurs an overdraft, all holders are equally liable for the debt. Some banks may offer overdraft protection, which should be considered when selecting a bank for a joint account. One of the primary rules of a joint bank account is that all account holders have equal ownership of the funds, irrespective of who deposited the money. This equal ownership applies unless an agreement states otherwise. Joint bank accounts typically include the right of survivorship. This means if one account holder passes away, the remaining balance in the account automatically passes to the surviving account holder(s), bypassing probate. If an account holder becomes incapacitated, a designated Power of Attorney (PoA) can manage the account. However, the specifics can vary based on the bank's rules and the PoA's stipulations. All account holders are equally liable for any debts associated with the account. This means if the account goes into overdraft or if there's a loan associated with the account, all account holders are responsible. Interest earned on the money in a joint bank account is subject to income tax. This tax liability is often shared among the account holders, depending on their individual income tax rates. Closing a joint bank account usually requires the consent of all account holders. Each bank has its own specific procedures, so it's crucial to consult with the bank to ensure the correct process is followed. Upon closure, the funds in the account must be disbursed. How these funds are divided can depend on the initial agreement between the account holders. In the absence of such an agreement, an equal division is typically implied. Each bank has specific procedures for closing a joint account. Documentation of account closure, disbursement of funds, and consent from all parties are usually necessary. Joint bank accounts offer a myriad of advantages and disadvantages that should be carefully weighed before deciding to open one. Shared Financial Responsibility: Joint bank accounts are often used by couples, relatives, or business partners to manage shared expenses. These accounts enable shared financial responsibilities, simplifying the process of budgeting, bill paying, and tracking expenses. Simplified Estate Planning: Joint accounts often come with the right of survivorship. When one account holder passes away, the remaining balance in the account bypasses probate and transfers directly to the surviving holder(s). Increased Account Insurance Coverage: Federal Deposit Insurance Corporation (FDIC) insures bank deposits up to a certain limit per account holder. With a joint account, the insurance limit is effectively doubled, providing increased coverage. Potential for Conflict: Despite the convenience of joint accounts, they can be a source of conflict, especially in the absence of clear communication and agreement about how the funds should be used. Risk of Credit Issues: All account holders are responsible for debts associated with the account. If one holder mismanages the account or incurs debt, it could impact all holders' credit scores. Difficulty in Dissolving the Account: Closing a joint bank account or removing a holder from the account often requires the consent of all account holders. This can prove difficult if the relationship between the holders becomes strained. Joint accounts can simplify finances for married couples by consolidating income and expenses. However, they should also consider the risks, such as the potential for financial disagreements or the impact of possible separation or divorce. In some cases, it may make sense for an aging parent to open a joint account with an adult child to help manage finances. This can ease financial management and provide a simple transfer of assets upon the parent's death. However, it's crucial to understand the potential risks, such as disputes among siblings or the impact on the parent's eligibility for financial aid. Business partners often use joint accounts to manage business finances. It simplifies the management of shared business expenses and revenue. However, clear agreements should be in place to govern the use of the account. If a joint account holder files for bankruptcy, the entire account may be at risk. Creditors may be able to claim the funds in the account to pay off debts. In a divorce, a joint account is typically considered marital property and is subject to division. The specifics can depend on the divorce agreement and the laws in the jurisdiction. As mentioned earlier, joint accounts usually come with the right of survivorship, meaning that upon the death of one account holder, the funds are automatically transferred to the surviving account holder(s). However, it's essential to understand that this could have implications for estate and inheritance tax. When disputes arise over a joint account, mediation can be an effective first step. A neutral third party helps the account holders discuss their issues and reach a mutually acceptable solution. If mediation is unsuccessful, legal recourse may be necessary. This could involve going to court or engaging in formal arbitration. It's critical to consult with a legal professional in such scenarios. Navigating the rules of joint bank accounts can seem daunting, but with the right knowledge and understanding, these tools can be effectively utilized. While joint accounts offer many advantages, like consolidated financial management and ease of fund access, they also come with potential risks and responsibilities. Therefore, clear communication, mutual trust, and shared financial responsibility are crucial when opening and maintaining a joint bank account. In any special circumstance, such as marriages, aging parents with adult children, or business partnerships, it's worth consulting with a financial advisor to ensure the arrangement aligns with everyone's best interests. Finally, understanding the implications of legal issues—like bankruptcy, divorce, or the death of an account holder—can help prevent unpleasant surprises down the road.Guide to Joint Bank Account Rules

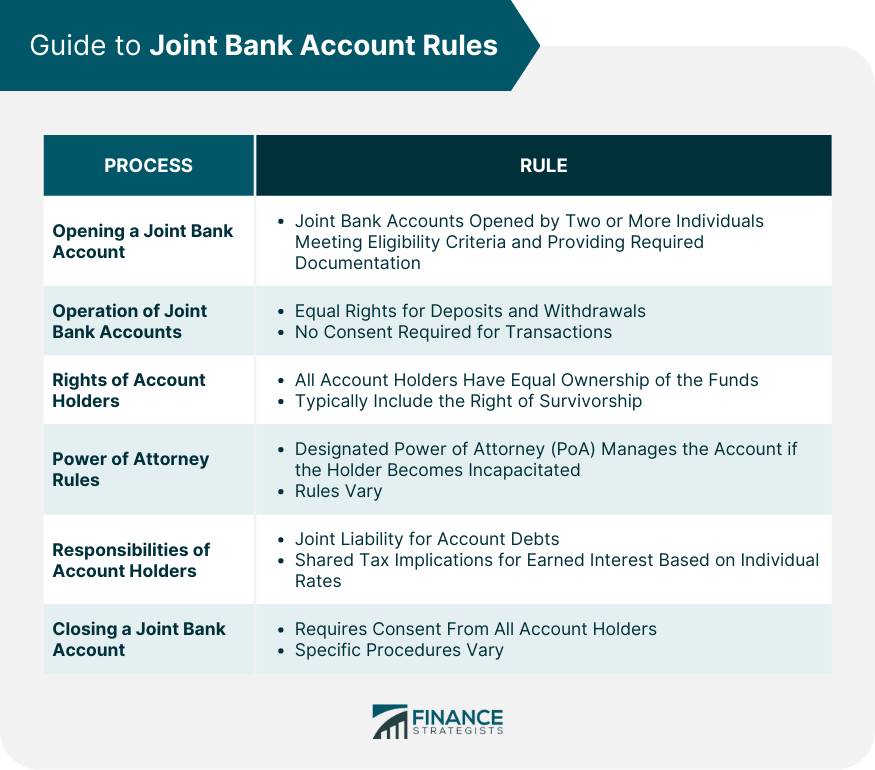

Opening a Joint Bank Account

Eligibility Criteria

Required Documentation

Operation of Joint Bank Accounts

Deposits and Withdrawals

Overdraft Rules

Rights of Account Holders

Equal Ownership

Right of Survivorship

Power of Attorney Rules

Responsibilities of Account Holders

Liability for Debts

Tax Implications

Closing a Joint Bank Account

Consent of All Parties

Disbursement of Funds

Procedure and Documentation

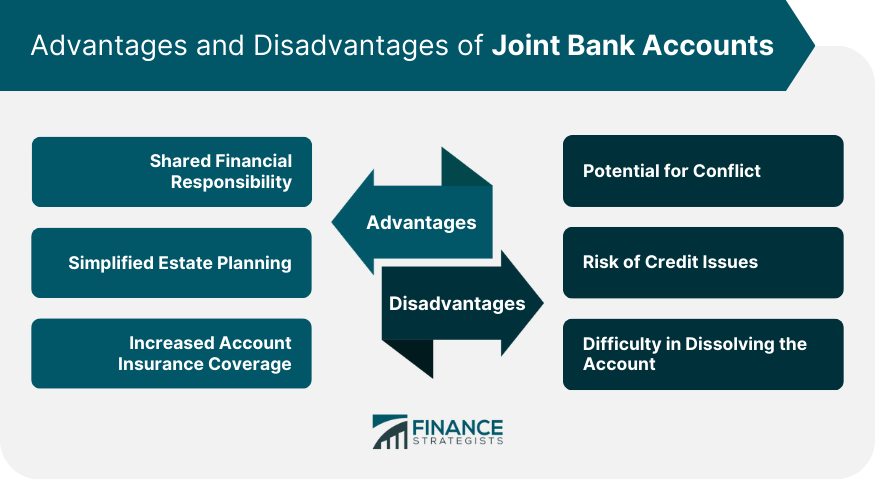

Advantages and Disadvantages of Joint Bank Accounts

Advantages

This can significantly simplify the estate planning process.Disadvantages

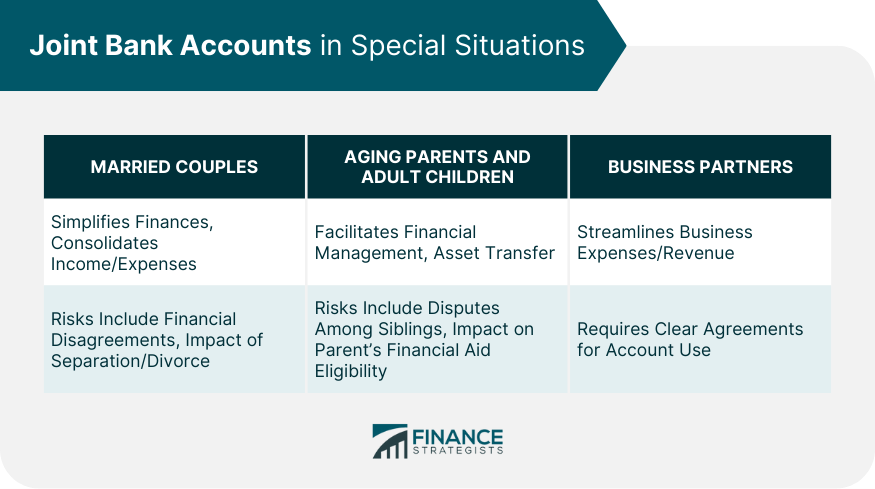

Joint Bank Accounts in Special Situations

Joint Bank Accounts for Married Couples

Joint Bank Accounts for Aging Parents and Adult Children

Joint Bank Accounts for Business Partners

Legal Considerations for Joint Bank Accounts

Bankruptcy and Joint Bank Accounts

Divorce and Joint Bank Accounts

Death of a Joint Account Holder

How to Solve Disputes Related to Joint Bank Accounts

Mediation

Legal Recourse

Conclusion

Joint Bank Account Rules FAQs

Generally, closing a joint bank account requires the consent of all account holders. However, the exact process can vary from bank to bank, so it's always a good idea to consult with your bank about their specific policies.

All account holders are equally responsible for any overdrafts that occur in a joint bank account. This means if one account holder incurs an overdraft, all account holders are equally liable for the debt.

If a joint account holder files for bankruptcy, the entire account may be at risk. Creditors may be able to claim the funds in the account to pay off debts. The specifics can vary based on jurisdiction and individual circumstances.

Interest earned on the money in a joint bank account is subject to income tax. This tax liability is often shared among the account holders, depending on their individual income tax rates.

Joint bank accounts typically include the right of survivorship. This means that if one account holder passes away, the remaining balance in the account automatically passes to the surviving account holder(s), bypassing probate. However, there could be implications for estate and inheritance tax.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.