A unitized fund is a type of investment vehicle that pools money from multiple investors to purchase securities. The fund's assets are divided into units, which represent a portion of the total value of the fund. Each unit has a specific price, which is determined by dividing the total value of the fund's assets by the number of units outstanding. Unitized funds can invest in a variety of securities, including stocks, bonds, and other financial instruments. They are commonly used by individual investors and institutional investors to gain exposure to a diversified portfolio of securities with the convenience of professional management and liquidity. Units are the basic building blocks of unitized funds. They represent a portion of the total value of the fund's assets. Each unit has a specific price, which is determined by dividing the total value of the fund's assets by the number of units outstanding. For example, if a fund has $10 million in assets and 1 million units outstanding, each unit is worth $10. Units are created and redeemed by the fund's manager based on the demand from investors. When an investor wants to purchase units in the fund, they send their money to the fund's manager, who then creates new units and adds them to the total number of units outstanding. When an investor wants to sell their units, they submit a redemption request to the fund's manager, who then buys back the units at the current unit price and reduces the total number of units outstanding. The unit price is an important metric for investors in unitized funds. It represents the value of each unit of the fund and is used to calculate the value of an investor's holdings in the fund. The unit price is determined by dividing the total value of the fund's assets by the number of units outstanding. The unit price can fluctuate based on changes in the value of the fund's assets or changes in the number of units outstanding. Mutual funds are a type of unitized fund that is open-ended, which means that units can be created and redeemed at any time. They are managed by a professional fund manager, who invests the fund's assets in a diversified portfolio of stocks, bonds, or other securities. Mutual funds are popular among individual investors because they offer diversification and professional management at a relatively low cost. ETFs are a type of unitized fund that is traded on an exchange like a stock. They are also open-ended, which means that units can be created and redeemed at any time. ETFs are designed to track a specific index or sector, such as the S&P 500 or the technology sector. These funds are popular among investors who want to gain exposure to a specific market segment or index. Unit investment trusts are a type of unitized fund that has a fixed portfolio of securities. UITs are closed-end, which means that a fixed number of units are issued at the time of the trust's creation, and no new units are created or redeemed. UITs are managed by a trustee, who selects the securities for the trust and holds them until the trust's termination date. These trusts are popular among investors who want to invest in a fixed portfolio of securities for a specific period of time. CITs are similar to mutual funds but are only available to institutional investors, such as pension plans or 401(k) plans. They are managed by a trustee or a bank, which invests the fund's assets in a diversified portfolio of securities. CITs are typically less expensive than mutual funds because they are not subject to the same regulatory requirements. CITs are also more customizable than mutual funds, allowing institutional investors to tailor the fund's investment strategy to meet their specific needs. It is the annual fee charged as a percentage of the fund's assets. The expense ratio includes the cost of managing the fund, as well as any administrative fees and other expenses. Expense ratios can vary widely among unitized funds and can have a significant impact on the fund's returns over time. In addition to the expense ratio, unitized funds may also charge other fees and expenses, such as sales charges, redemption fees, or account maintenance fees. These fees can vary widely among unitized funds and can have a significant impact on the overall cost of investing in the fund. Fees and expenses can have a significant impact on the returns of unitized funds over time. Investors should be aware of the fees and expenses associated with a unitized fund before investing and should compare the fees of different funds to determine which one offers the best value. Investors gain exposure to a diversified portfolio of securities, which can help to reduce the risk of individual company failures impacting the portfolio. Diversification can also help to smooth out the ups and downs of the stock market, potentially leading to more consistent returns over time. Unitized funds are supervised by professional fund managers who have experience in selecting and handling securities. These managers have access to research and analysis that individual investors may not have, allowing them to make informed investment decisions. Professional management can also help to reduce the risk of investor mistakes, such as selling securities at the wrong time or investing in companies that are not profitable. Unitized funds are generally more liquid than individual securities, meaning investors can buy and sell units anytime. This makes them a more convenient investment option than individual securities, which may be more difficult to buy or sell. Liquidity also helps to ensure that investors can access their funds when they need them. Investing in unitized funds can be a convenient option for investors who do not have the time or expertise to select and manage individual securities. These funds provide a one-stop-shop for investors who want to gain exposure to a diversified portfolio of securities without having to research and select individual companies. Like any investment, unitized funds are subject to market risk. This means that changes in the overall market can impact the value of the fund's assets and the unit price. It can be caused by various factors, such as economic conditions, interest rates, or geopolitical events. Management risk refers to the risk that the fund manager will make poor investment decisions or fail to adequately diversify the fund's assets. Poor management can lead to underperformance and potentially result in the loss of the investor's principal investment. While unitized funds are generally more liquid than individual securities, it still carries risk. If a large number of investors try to sell their units at the same time, it can cause the unit price to decline and potentially lead to a liquidity crisis. This can make it difficult for investors to sell their units at the desired price. Some unitized funds may be heavily concentrated in a specific sector or market segment. This can increase the risk of the fund's performance being impacted by changes in that sector or segment. It can also lead to underperformance if the sector or segment underperforms compared to the broader market. The first step in choosing a unitized fund is to determine your investment objective. Are you looking for long-term growth or income? Do you want exposure to a specific market segment or sector? Understanding your investment objective can help you narrow down the universe of available unitized funds and select the one that is best suited to your needs. Some unitized funds may be riskier than others, depending on the types of securities in the fund's portfolio and the investment strategy employed by the fund manager. Investors should select a unitized fund that aligns with their risk tolerance and investment objectives. Past performance is not a guarantee of future results, but it can provide insight into how the fund has performed in different market conditions. Investors should compare the performance of different unitized funds over different time periods to determine which one has a track record of consistent returns. Investors should research the fund manager's background, investment philosophy, and experience managing similar funds. A fund manager with a track record of successful performance and a clear investment philosophy may be more likely to deliver consistent returns over time. Finally, investors should consider the fees and expenses associated with a unitized fund before investing. As mentioned earlier, fees and expenses can have a significant impact on the returns of a unitized fund over time. Investors should compare the fees and expenses of different funds to determine which one offers the best value. Unitized funds can be an effective way to achieve long-term investment goals. They provide investors with diversification, professional management, liquidity, and convenience. However, investors should be aware of the risks associated with unitized funds, including market risk, management risk, liquidity risk, and concentration risk. It's essential to carefully consider investment objectives, risk tolerance, and the fees and expenses associated with a unitized fund before investing. By doing proper due diligence and selecting the right unitized fund, investors can take advantage of the benefits of unitized funds and achieve their long-term investment goals. Additionally, staying informed about market trends and changes in the fund's performance can help investors make informed decisions about when to buy or sell units. Overall, unitized funds are a valuable investment option for investors seeking exposure to a diversified portfolio of securities with the convenience of professional management and liquidity.What Is a Unitized Fund?

Structure of Unitized Funds

What are Units?

How are Units Created and Redeemed?

Importance of the Unit Price

Types of Unitized Funds

Mutual Funds

Exchange-Traded Funds (ETFs)

Unit Investment Trusts (UITs)

Collective Investment Trusts (CITs)

Fees and Expenses of Unitized Funds

Expense Ratios

Other Fees

Impact on Returns

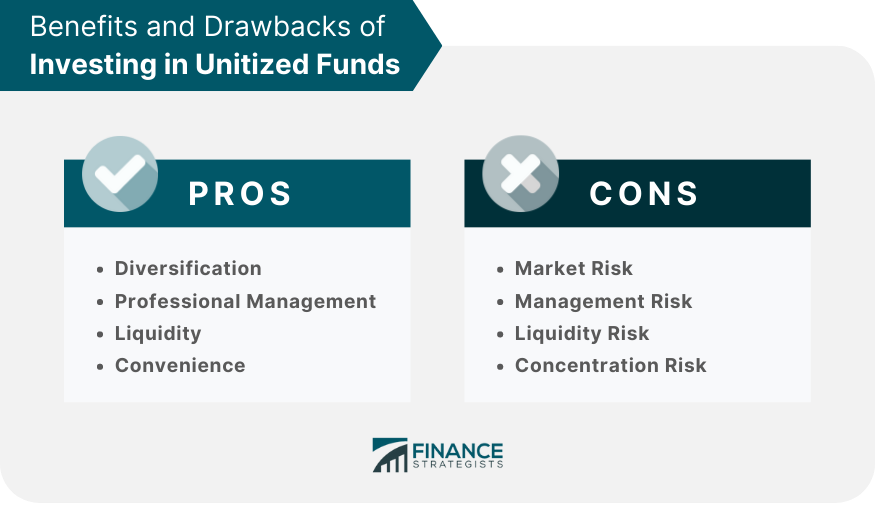

Benefits of Investing in Unitized Funds

Diversification

Professional Management

Liquidity

Convenience

Drawbacks of Investing in Unitized Funds

Market Risk

Management Risk

Liquidity Risk

Concentration Risk

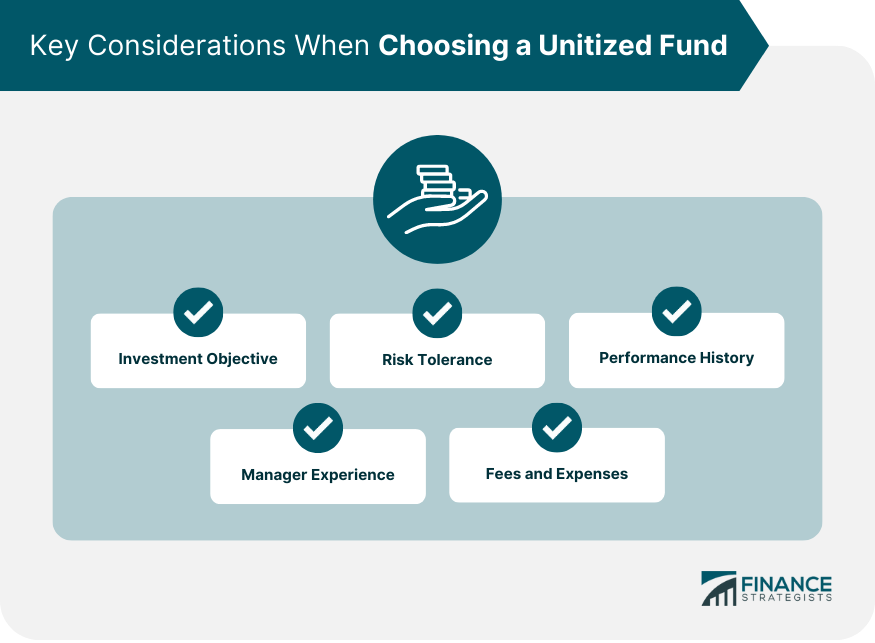

Key Considerations When Choosing a Unitized Fund

Investment Objective

Risk Tolerance

Performance History

Manager Experience

Fees and Expenses

Final Thoughts

Unitized Fund FAQs

A unitized fund is a type of investment fund that pools money from multiple investors and issues units of ownership to each investor based on the proportion of their investment in the fund. The value of each unit is calculated based on the net asset value (NAV) of the fund, which is determined by dividing the total value of the assets held in the fund by the total number of units outstanding.

One of the main advantages of investing in a unitized fund is that it allows investors to access a diversified portfolio of assets that they might not be able to afford on their own. Additionally, because the value of each unit is based on the NAV of the fund, investors are able to buy and sell units at any time without having to worry about the liquidity of individual assets in the portfolio.

Unitized funds are typically managed by professional portfolio managers who are responsible for making investment decisions on behalf of the fund's investors. The portfolio manager will invest the fund's assets according to the investment objectives and strategy of the fund, with the goal of generating returns for the investors.

There are many different types of unitized funds available to investors, including mutual funds, exchange-traded funds (ETFs), and index funds. Each type of fund has its own unique investment strategy and objective, and investors can choose the type of fund that best fits their investment goals and risk tolerance.

Like any investment, there are risks associated with investing in a unitized fund. One of the main risks is the potential for loss of principal, which can occur if the value of the assets held in the fund declines. Additionally, the value of each unit can fluctuate based on changes in the NAV of the fund, which can be affected by a variety of factors such as market conditions and the performance of individual assets in the portfolio.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.