A Third-Party Administrator is an organization that provides administrative services, such as recordkeeping, compliance testing, and participant communication, to retirement plans. TPAs serve as intermediaries between plan sponsors and other service providers, helping to streamline plan administration and ensure regulatory compliance. TPAs play a crucial role in the efficient management of retirement plans by providing specialized expertise and handling various administrative tasks on behalf of plan sponsors. This allows plan sponsors to focus on their core business activities while ensuring the effective operation of their retirement plans. TPAs maintain accurate records of plan assets, participant accounts, contributions, and investment transactions. TPAs facilitate the processing of employee and employer contributions to retirement plans, ensuring timely and accurate allocation of funds to participant accounts. TPAs perform various compliance tests, such as nondiscrimination testing and top-heavy testing, to ensure that retirement plans meet regulatory requirements. TPAs create and distribute enrollment materials, such as plan descriptions, enrollment forms, and beneficiary designation forms, to help educate participants about their retirement plan options and guide them through the enrollment process. TPAs prepare and distribute periodic benefit statements to participants, providing an overview of account balances, investment performance, and other relevant plan information. TPAs may assist in creating and distributing SPDs, which outline key plan features and benefits, to ensure that participants have access to comprehensive plan information. TPAs prepare plan documents, such as adoption agreements, summary plan descriptions, and plan amendments, to ensure compliance with applicable laws and regulations. TPAs work with plan sponsors to design and implement custom retirement plans tailored to their specific needs and objectives. TPAs can help plan sponsors navigate the process of amending their retirement plans, ensuring that any changes comply with regulatory requirements and are effectively communicated to participants. TPAs assist plan sponsors with the preparation and filing of Form 5500, an annual report required by the Department of Labor and the Internal Revenue Service. TPAs perform nondiscrimination testing to ensure that retirement plans do not unfairly favor highly compensated employees or violate other regulatory requirements. TPAs may coordinate with plan auditors to facilitate plan audits and ensure that any issues identified are addressed in a timely and compliant manner. Evaluate potential TPAs based on their industry certifications, such as the American Society of Pension Professionals & Actuaries (ASPPA) or the National Institute of Pension Administrators (NIPA), which indicate a commitment to professionalism and ongoing education. Review client testimonials and case studies to gain insight into the experiences of other plan sponsors working with the TPA. Consider the TPA's years in business as an indicator of their experience and stability within the retirement plan industry. Assess the range of services offered by the TPA to ensure they can meet your retirement plan's specific administrative needs. Determine whether the TPA has specialized expertise in areas relevant to your retirement plan, such as plan design, compliance testing, or participant communication. Ensure that the TPA can accommodate your retirement plan's growth and changing needs over time. Evaluate the TPA's fee structure to ensure transparency and a clear understanding of the costs associated with their services. Compare the TPA's fees with those of other providers to ensure competitive pricing for the services provided. Consider the overall value provided by the TPA in terms of expertise, service quality, and support, in addition to pricing. Determine if the TPA assigns dedicated account managers to provide personalized support and guidance throughout the engagement. Assess the TPA's responsiveness to inquiries and requests for assistance, as this can impact the efficiency and effectiveness of your retirement plan administration. Ensure that the TPA provides ongoing support and education to help plan sponsors stay informed about regulatory changes, industry trends, and best practices. TPAs offer specialized expertise and knowledge in retirement plan administration, helping plan sponsors navigate complex regulatory requirements and industry best practices. TPAs help manage compliance and mitigate risk by performing regular testing, preparing required filings, and monitoring plan operations for adherence to applicable laws and regulations. By outsourcing administrative tasks to a TPA, plan sponsors can save time and resources that can be better allocated to their core business activities. TPAs can improve the participant experience by providing clear communication, educational materials, and prompt responses to inquiries, helping participants make informed decisions about their retirement savings. The costs and fees associated with engaging a TPA can be a potential drawback for some plan sponsors, particularly if the TPA's pricing structure is not transparent or competitive. Working with a TPA may require additional coordination between plan sponsors and other service providers, such as investment managers or custodians, which can create potential inefficiencies or communication challenges. Depending on the specific services offered by the TPA, there may be gaps in the administration of the retirement plan, which could require additional resources or support from the plan sponsor. Establish clear lines of communication with the TPA to ensure effective collaboration and prompt resolution of any issues or concerns. Conduct regular reviews of the TPA's performance and services to ensure alignment with your retirement plan's objectives and evolving needs. Track key performance metrics, such as response times, accuracy of recordkeeping, and participant satisfaction, to evaluate the TPA's effectiveness and identify areas for improvement. Maintain a collaborative approach with the TPA, recognizing that both parties share responsibility for the successful administration of the retirement plan. TPAs play a critical role in retirement plan administration by providing specialized expertise, managing complex administrative tasks, and ensuring regulatory compliance on behalf of plan sponsors. When selecting a TPA, plan sponsors should consider factors such as reputation, experience, service offerings, fees, and customer support, to ensure the best fit for their retirement plan's needs and objectives. While working with TPAs can offer numerous benefits, plan sponsors should also be aware of potential challenges and drawbacks, such as costs, coordination with other service providers, and potential service gaps. By carefully selecting a TPA and implementing best practices for working with them, plan sponsors can effectively balance these benefits and challenges, ensuring a successful partnership and the efficient administration of their retirement plans.What Is a Third-Party Administrator (TPA)?

Services Provided by TPAs

Plan Administration

Recordkeeping

Contribution Processing

Compliance Testing

Participant Communication

Enrollment Materials

Benefit Statements

Summary Plan Descriptions (SPDs)

Plan Design and Consulting

Plan Document Preparation

Custom Plan Design

Plan Amendments

Regulatory Compliance

Form 5500 Preparation

Nondiscrimination Testing

Plan Audits

Factors to Consider in Choosing a Third-Party Administrator

Reputation and Experience

Industry Certifications

Client Testimonials

Years in Business

Range of Services Offered

Comprehensive Service Offerings

Specialized Expertise

Scalability

Fees and Pricing Structure

Transparent Fee Structure

Competitive Pricing

Value for Services Provided

Customer Service and Support

Dedicated Account Managers

Responsiveness

Ongoing Support and Education

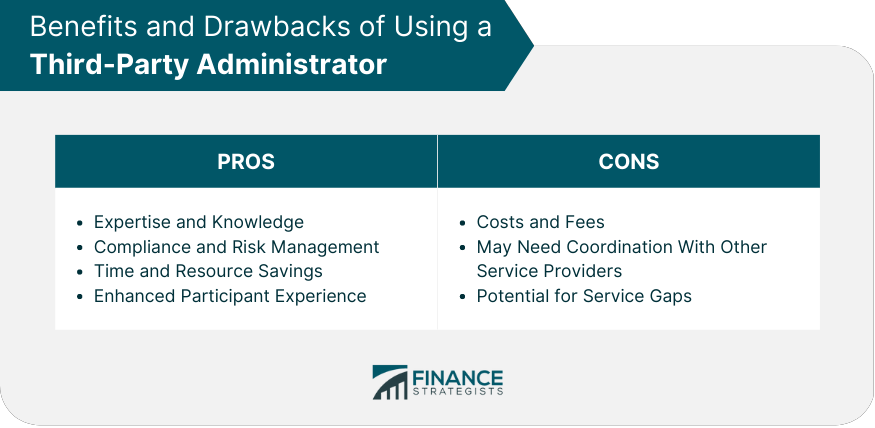

Benefits of Using a Third-Party Administrator

Expertise and Knowledge

Compliance and Risk Management

Time and Resource Savings

Enhanced Participant Experience

Potential Challenges and Drawbacks

Costs and Fees

May Need Coordination With Other Service Providers

Potential for Service Gaps

Best Practices for Working With TPAs

Clear Communication

Regular Reviews and Updates

Monitoring Performance Metrics

Collaborative Approach

Conclusion

Third-Party Administrator (TPA) FAQs

A Third-Party Administrator is a company that provides administrative and record-keeping services for retirement plans, such as 401(k) plans, profit-sharing plans, and pension plans.

Third-Party Administrators (TPAs) offer a range of services for retirement plans, including plan design, compliance testing, record-keeping, investment management, and participant education.

Companies benefit from using Third-Party Administrators (TPAs) for their retirement plans because TPAs are experts in retirement plan administration and can help ensure that the plan is compliant with IRS and Department of Labor regulations. TPAs also offer a range of services that can save companies time and money, such as record-keeping and compliance testing.

Third-Party Administrators (TPAs) are typically compensated on a fee-for-service basis, meaning that they charge a fee for each service they provide. The fees may be charged to the plan sponsor, the plan participants, or both.

Companies should consider several factors when choosing a Third-Party Administrator (TPA) for their retirement plan, including the TPA's experience, expertise, reputation, and fees. Companies should also consider the level of customer service the TPA provides, as well as the range of services offered.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.