You can apply for a home loan even with bad credit. Approval depends on your full financial profile, not just your credit score. A lender will usually look at your credit history, income, employment, debt-to-income ratio, down payment, cash reserves, and the type of loan you are applying for. Federal mortgage rules also generally require lenders to make a reasonable, good-faith determination that you can repay the loan before they approve you. A low credit score may hurt your application, but it is only one piece of the file. A borrower with a 580 credit score, stable income, low debt, and money saved may be in a stronger position than someone with a higher score but unstable income and maxed-out credit cards. Bad credit also means different things to different lenders. One lender may deny you. Another may approve you with different terms. That is why shopping around is especially important if your credit is weak. This gives you a realistic view of where you stand. A borrower with a 500 score is in a very different position from a borrower with a 580, 620, or 660 score. Those differences can affect which loan programs are available, how much you may need for a down payment, and whether your application can be approved through automated underwriting. Look for: Late payments Collections Charge-offs High credit card balances Old bankruptcies Foreclosures Incorrect balances Accounts that do not belong to you Duplicate negative items If there are errors, dispute them before applying. A single incorrect late payment or collection account can affect your score and weaken your mortgage file. Before applying, estimate your monthly income, current debt payments, likely mortgage payment, property taxes, homeowners insurance, mortgage insurance, and other housing costs. If your debt-to-income ratio is already stretched, a lender may hesitate even if your credit score technically meets the minimum requirement. Also review your available cash. You may need money for a down payment, closing costs, prepaid taxes and insurance, reserves, inspections, moving expenses, and repairs after closing. This is where many borrowers get surprised. Getting approved is one thing. Having enough cash to close is another. Borrowers with bad credit should not assume a conventional mortgage is the only path. Depending on your situation, you may want to compare FHA, VA, USDA, conventional, and non-QM loan options. FHA loans are often the first place lower-credit borrowers look because the program allows lower credit scores than many conventional loans. VA loans may be powerful for eligible veterans, service members, and certain surviving spouses. USDA loans may help qualified borrowers buying in eligible rural or suburban areas. Conventional loans may still be possible, but they often become more expensive or difficult with lower credit. Non-QM loans may be available in some cases, but they can carry higher rates and fees. The right loan depends on your credit score, eligibility, income, property location, down payment, and long-term cost. Not every lender has the same appetite for risk. Even when a loan program allows a lower credit score, individual lenders may set stricter requirements. These are often called lender overlays. For example, FHA guidelines may allow a low score in some cases, but a specific lender may decide it only wants to approve borrowers above a higher threshold. That means one denial does not necessarily mean you cannot get a mortgage. Compare several lenders, especially lenders with experience in FHA, VA, USDA, or lower-credit mortgage files. The Consumer Financial Protection Bureau recommends comparing multiple Loan Estimates because they help borrowers evaluate cost, terms, and lender fit. A preapproval helps you understand what a lender may be willing to offer before you start making offers on houses. For bad-credit borrowers, this step is especially important. A preapproval can reveal whether your score is too low, your debt is too high, your income documentation is weak, or your down payment is not enough. It can also help you avoid wasting time looking at homes outside your realistic price range. A strong preapproval is not a final approval. The lender still has to verify the property, review documentation, order an appraisal, and complete underwriting. But it gives you a much clearer starting point. Lenders need documentation. Be ready before they ask. Common documents include recent pay stubs, W-2s, tax returns, bank statements, retirement or investment account statements, photo identification, rent history, debt statements, and explanations for major credit issues. If you are self-employed, expect more documentation. You may need business tax returns, profit and loss statements, bank statements, and proof that your income is stable. If you have past credit problems, the lender may ask for a letter of explanation. Keep it short, factual, and focused on what happened, how it was resolved, and why it is unlikely to happen again. The lender will review your income, assets, debts, credit, and the property itself. The file then moves through underwriting. During this stage, the lender may request additional documents or clarification. Do not panic if the lender asks for more information. That is normal. Respond quickly and clearly. After applying, protect your financial profile. Do not open new credit cards. Do not finance furniture. Do not buy a car. Do not make large unexplained deposits. Do not miss payments. Do not change jobs unless you have discussed it with your lender. A mortgage approval can be affected before closing if your credit score drops, your debt increases, or your income changes. The finish line is closing day, not preapproval day. Under FHA rules, borrowers with a credit score of 580 or higher may qualify for the 3.5% minimum down payment option. Borrowers with scores from 500 to 579 may be limited to a maximum loan-to-value ratio of 90%, which generally means at least 10% down. Borrowers below 500 are generally not eligible for FHA-insured financing. This makes FHA a major option for people rebuilding credit, especially if their score is too low for a conventional loan or they only have a modest down payment. FHA can also be helpful when a borrower has older credit issues but has recently shown more stable payment behavior. However, FHA is not always the cheapest option. FHA loans include mortgage insurance premiums, and those costs can make the loan more expensive over time. Borrowers still need to meet income, debt, property, and documentation requirements. An FHA loan may make sense if your credit score is too low for conventional financing, your income is steady, and the total monthly payment remains affordable. It may not be the best choice if mortgage insurance makes the payment too high, if you can qualify for a less expensive conventional loan, or if you are stretching your budget just to get approved. VA loans may be available to eligible veterans, active-duty service members, National Guard members, reservists, and certain surviving spouses. The VA does not set a universal minimum credit score for its home loan program, but lenders still review credit history and may set their own credit score requirements. VA loans can be especially valuable for eligible borrowers with imperfect credit because they may allow no down payment and do not require monthly private mortgage insurance. That can make the upfront and monthly cost of buying a home more manageable. However, many VA loans include a funding fee unless the borrower is exempt. The property must also meet VA standards, and the borrower still has to qualify based on income, credit, residual income, and overall ability to repay. A VA loan may make sense if you are eligible, have stable income, and want to buy with limited cash down. It may not be the best fit if the funding fee makes the loan too expensive, the property does not meet VA requirements, or a lender’s credit overlay prevents approval. USDA loans may help eligible borrowers buy homes in qualifying rural and some suburban areas. The USDA Single Family Housing Guaranteed Loan Program is designed for eligible low- to moderate-income borrowers purchasing eligible properties. These loans may offer no down payment, which can be attractive for buyers who have income stability but limited savings. USDA loans can be useful for borrowers with weaker credit if the rest of the file is strong. However, the program has important limits. The home must be in an eligible location, the borrower must meet income requirements, and the lender still has to approve the credit, income, debt, and property details. Interest rates and lender requirements can also vary, so comparison shopping matters. A USDA loan may make sense if the property is eligible, your income falls within program limits, and your main obstacle is saving a large down payment. It may not work if the home is outside an eligible area, your income is too high, your credit file is too weak for the lender, or you need to buy in a market that does not qualify. Conventional loans are not backed by the federal government. They are usually harder to qualify for with bad credit than FHA, VA, or USDA loans. Many conventional mortgage options are designed for borrowers with stronger credit profiles, lower debt-to-income ratios, and more consistent financial histories. That does not mean a conventional loan is impossible. A borrower with fair credit, enough savings, stable income, and a manageable debt load may still qualify. In some cases, a conventional loan can be cheaper than an FHA loan, especially if the borrower qualifies for reasonable pricing and can eventually remove private mortgage insurance after building enough equity. A conventional loan may make sense if your credit is closer to fair than poor, you have a stronger down payment, and the total cost is lower than FHA. It may not be the best option if your score is too low, your interest rate is much higher, your private mortgage insurance is expensive, or you cannot pass underwriting. Non-QM loans and portfolio loans may be options for borrowers who do not fit standard mortgage guidelines. These loans can sometimes help self-employed borrowers, borrowers with nontraditional income, borrowers with recent credit problems, or borrowers whose finances are strong but difficult to document through traditional underwriting. Some non-QM lenders may use bank statements, assets, rental income, or other alternative documentation to evaluate the borrower. Portfolio lenders may also keep loans on their own books instead of selling them, which can give them more flexibility in certain cases. However, these loans require caution. They can come with higher interest rates, larger down payments, higher fees, and less favorable terms. A non-QM or portfolio loan may solve an approval problem while creating a payment problem. It may make sense if you have strong income or assets but do not fit traditional underwriting rules. It may not be wise if it is the only way to force a purchase you cannot comfortably afford. A focused credit plan can make a meaningful difference. Pay every bill on time, reduce credit card balances, avoid new debt, and dispute any errors on your credit reports. If you have collections or charge-offs, ask a mortgage lender how those accounts may affect approval before paying or settling them. Once your score improves and your recent payment history looks stronger, you may qualify for more loan options, better pricing, or a lower down payment requirement. Down payment assistance programs may help eligible buyers cover part of the upfront cost of buying a home. These programs are often offered by state housing agencies, local governments, nonprofits, or approved lenders. They can be useful if your credit is close to qualifying but your savings are limited. However, they usually have income limits, homebuyer education requirements, purchase price limits, and loan program rules. They can help with cash to close, but they do not replace the need to qualify for the mortgage itself. If your application is being denied because the payment is too high, a lower purchase price may help. A smaller loan can reduce your monthly payment, lower your debt-to-income ratio, and decrease the amount you need for a down payment and closing costs. This does not mean giving up on homeownership. It may mean starting with a more affordable property so the mortgage fits your income instead of stretching your budget too thin. This can be especially useful for borrowers with limited credit history, nontraditional credit, or a recent financial setback that has since been resolved. The process usually requires more documentation, such as rent payment history, bank statements, letters of explanation, or proof of stable income. It is not easier approval, but it can give the lender a fuller picture of your ability to repay. Renting longer can be frustrating when you want to buy, but it can also be the smarter financial move. If the only mortgage available comes with a high rate, expensive fees, or a payment that leaves no room in your budget, waiting may protect you from a costly mistake. Use that time to build credit, save more cash, reduce debt, and prepare for a stronger application. A delayed home purchase can still be a successful one if it leads to better terms and a more affordable payment. Applying for a home loan with bad credit is possible, but it takes preparation. Your credit score matters, but lenders also review your income, debt, savings, employment history, down payment, and ability to repay the loan. Start by checking your credit reports, understanding your debt-to-income ratio, and comparing loan programs that may fit your situation. FHA, VA, USDA, conventional, non-QM, and portfolio loans can all serve different borrowers, but the right loan is not simply the one that gets approved. It is the one with a payment you can afford over time. If you cannot qualify yet, use the delay wisely. Pay bills on time, reduce debt, save more cash, dispute credit report errors, or consider a lower purchase price. Bad credit can make the mortgage process harder, but it does not automatically prevent homeownership. With the right plan, you can improve your chances of approval and choose a loan that supports long-term financial stability.Home Loan With Bad Credit: Overview

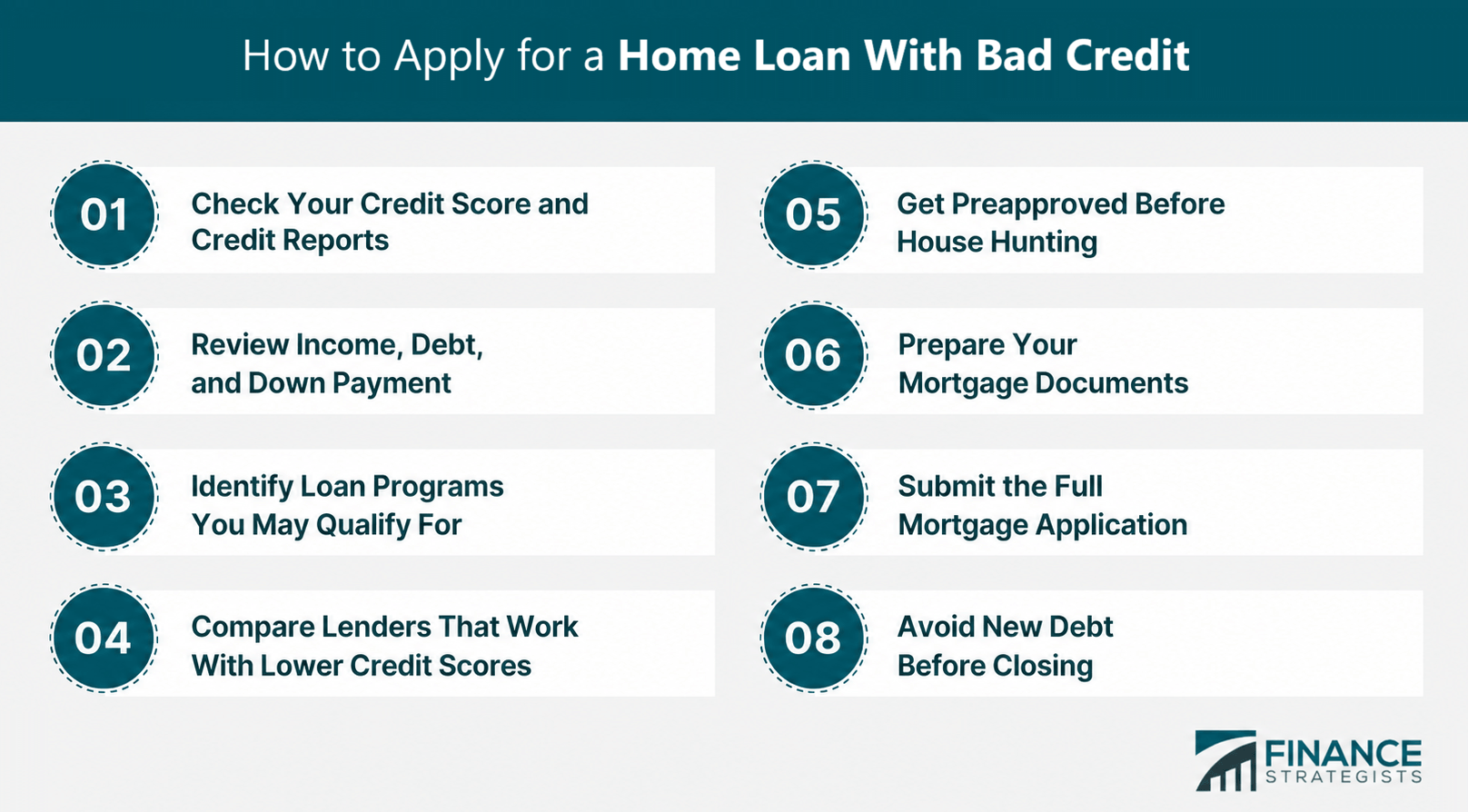

How to Apply for a Home Loan With Bad Credit

Check Your Credit Score and Credit Reports

Review Your Income, Debt, and Down Payment

Identify the Loan Programs You May Qualify For

Compare Lenders That Work With Lower Credit Scores

Get Preapproved Before House Hunting

Prepare Your Mortgage Documents

Submit the Full Mortgage Application

Avoid New Debt Before Closing

Best Home Loan Options for Bad Credit

FHA Loans

VA Loans

USDA Loans

Conventional Loans

Non-QM and Portfolio Loans

Alternatives If You Cannot Qualify Yet

Improve Your Credit and Reapply Later

Look for Down Payment Assistance

Consider a Lower Purchase Price

Use Manual Underwriting

Rent While You Rebuild

Final Thoughts

How to Apply for a Home Loan With Bad Credit FAQs

Yes. Bad credit can make approval harder, but lenders also review your income, debt, down payment, employment history, savings, and ability to repay the loan.

It depends on the loan type and lender. FHA loans may allow scores as low as 500 with a larger down payment, while many conventional loans require stronger credit.

FHA loans are often a common option for borrowers with lower credit, but VA, USDA, conventional, non-QM, and portfolio loans may also work depending on your situation.

Yes. One denial does not mean every lender will deny you. Some lenders have stricter requirements than others, so comparing multiple lenders matters.

Focus on improving your credit, reducing debt, saving more cash, disputing credit report errors, or considering a lower purchase price before reapplying.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.