A line of credit loan is a type of financing that allows borrowers to draw funds up to a predetermined limit. It provides borrowers with the flexibility to borrow and repay repeatedly within the agreed limit. Interest is typically charged only on the amount that is borrowed, not on the total limit. Line of credit loans can be unsecured or secured, depending on whether or not collateral is required. They function somewhat like credit cards, offering revolving credit that becomes available again once repayments are made, making them an excellent tool for managing cash flow and unexpected expenses. They provide the unique advantage of making funds available for unexpected costs or opportunities without the need to apply for multiple loans. This flexibility can be instrumental in navigating financial uncertainty, managing seasonal cash flow fluctuations, or quickly seizing growth opportunities. A personal line of credit is typically unsecured, meaning it doesn't require collateral. It's designed to finance personal expenditures such as home improvements, medical expenses, or consolidating higher-interest debt. Because they are unsecured, personal lines of credit generally require a strong credit history and may carry higher interest rates compared to secured lines of credit. Business lines of credit cater specifically to the needs of businesses, providing a cushion for managing cash flow, purchasing inventory, or handling unexpected expenses. Depending on the lender and the borrower's creditworthiness, a business line of credit may be secured or unsecured. The flexibility of a business line of credit can be particularly beneficial for businesses with fluctuating cash flow or seasonal operation cycles. A home equity line of credit, commonly referred to as a HELOC, is a secured line of credit. The borrower's home equity serves as collateral. HELOCs typically offer larger borrowing limits and lower interest rates than unsecured lines of credit. They are often used for large expenses like home renovations, education costs, or debt consolidation. However, borrowers should note that failure to repay a HELOC could result in loss of the home. Borrowers have the freedom to use the funds as needed and only pay interest on what they use. Additionally, as borrowers repay the principal, those funds become available to borrow again. This flexibility makes lines of credit ideal for handling unpredictable expenses or cash flow needs. Line of credit loans generally offers lower interest rates than credit cards, making them a more cost-effective solution for borrowing over a longer period. Secured lines of credit, like HELOCs, tend to have even lower rates due to the reduced risk to lenders. Certain types of line of credit loans may offer tax benefits. For example, the interest paid on a HELOC is typically tax-deductible if the funds are used for home improvements. However, tax laws can be complex and vary by location, so borrowers should consult with a tax advisor to understand potential tax benefits fully. While the flexibility of a line of credit loans can be advantageous, it also presents the risk of overborrowing. Because the available credit is replenished as the borrower makes payments, it can be tempting to continually draw from the line of credit, leading to potential debt accumulation. Many lines of credit feature variable interest rates, meaning the rate can increase or decrease over time based on market conditions. While this can be beneficial in a falling rate environment, it can also lead to higher costs when rates rise. This uncertainty can make it more difficult to budget for interest payments. Applying for and opening a line of credit can impact your credit score. A hard inquiry is typically made during the application process, which can lower your score temporarily. Additionally, if the line of credit leads to high credit utilization or missed payments, it can negatively impact your credit score. When applying for a line of credit loan, lenders will consider your credit score and credit history. A high credit score and a history of responsible borrowing typically lead to better loan terms and lower interest rates. A lower credit score or negative items on your credit history may result in higher rates or even denial of the application. Your income and financial stability are also crucial factors in the application process. Lenders need to be confident in your ability to repay the borrowed funds. Steady employment, a consistent income, and a low debt-to-income ratio can all improve your chances of qualifying for a line of credit loan and securing favorable terms. For secured lines of credit, such as a HELOC, collateral is required. The value of the collateral can impact the borrowing limit and the interest rate of the line of credit. Assets can sometimes be used to improve your chances of qualifying for an unsecured line of credit, as they may demonstrate your financial stability to potential lenders. Before applying for a line of credit loan, it's important to research various lenders and compare their offerings. Factors to consider include the maximum credit limit, interest rates, fees, and terms. Consider your specific needs and financial situation to determine the most suitable type of line of credit for you. When applying for a line of credit loan, you'll need to provide certain documents. These typically include proof of identity, proof of income, and financial statements. If you're applying for a secured line of credit, you'll also need documentation relating to the collateral. It's important to gather these documents in advance to ensure a smooth application process. Once you've chosen a lender and gathered all the required documentation, you can proceed with the application. This can typically be done online, over the phone, or in person. After submitting the application, the lender will review your financial situation, conduct a credit check, and decide whether to approve the line of credit and on what terms. Line of credit loans offers borrowers the flexibility to borrow and repay funds within a predetermined limit, making them valuable tools for managing cash flow and unexpected expenses. The advantages of a line of credit loans include flexible borrowing, lower interest rates compared to credit cards, and potential tax benefits. However, there are risks to consider, such as the temptation to overborrow and accumulate debt, variable interest rates that can increase costs, and the potential impact on credit scores. To qualify for a line of credit loan, lenders typically consider factors such as credit score and history, income and financial stability, and collateral or assets for secured loans. It's important for borrowers to research lenders, gather necessary documentation, and carefully submit their applications to increase their chances of approval. Overall, line of credit loans can be beneficial financial tools when used responsibly and with a clear understanding of the associated advantages and risks.What Is a Line of Credit Loan?

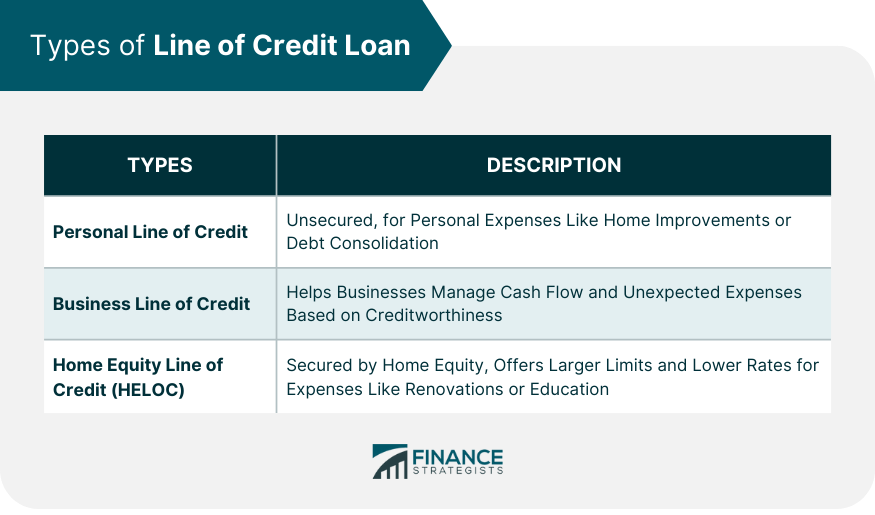

Types of Line of Credit Loans

Personal Line of Credit

Business Line of Credit

Home Equity Line of Credit (HELOC)

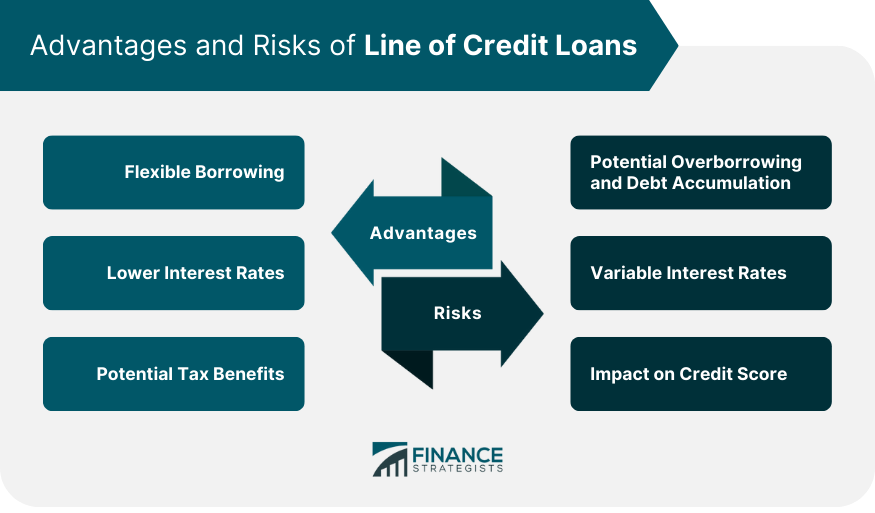

Advantages of Line of Credit Loans

Flexible Borrowing

Lower Interest Rates

Potential Tax Benefits

Risks of Line of Credit Loans

Potential Overborrowing and Debt Accumulation

Variable Interest Rates

Impact on Credit Score

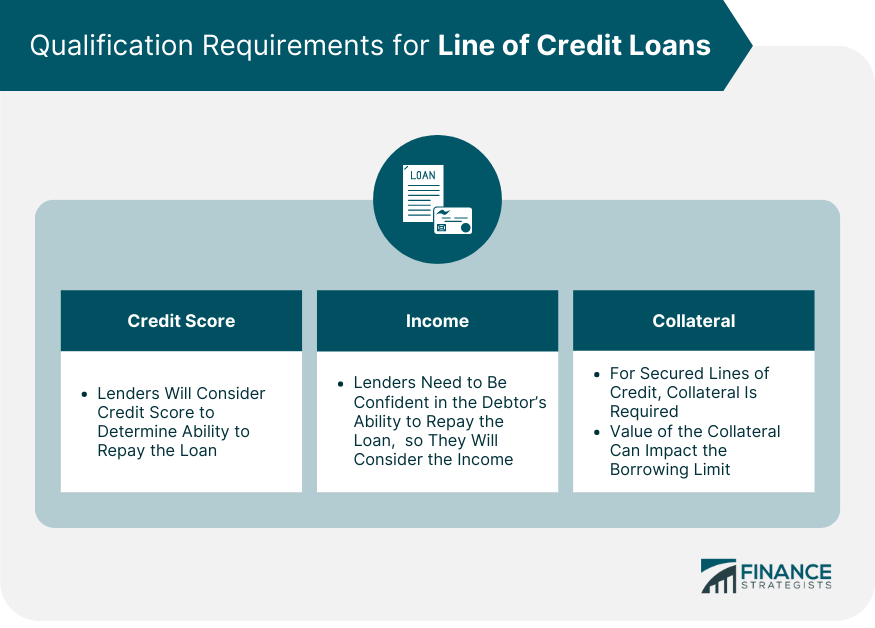

Qualification Requirements for Line of Credit Loans

Credit Score and History

Income and Financial Stability

Collateral and Assets

Application Process for Line of Credit Loans

Researching Lenders and Options

Gathering Required Documentation

Submitting the Application

Conclusion

Line of Credit Loan FAQs

A line of credit loan is a flexible form of financing that allows borrowers to draw funds up to a certain limit and repay them over time. The available credit is replenished as the borrower makes payments.

The main types of line of credit loans include personal lines of credit, business lines of credit, and home equity lines of credit (HELOCs).

Advantages of line of credit loans include flexible borrowing, lower interest rates compared to other forms of credit, and potential tax benefits.

Risks of line of credit loans include potential overborrowing and debt accumulation, variable interest rates, and a possible impact on your credit score.

The application process for a line of credit loan involves researching lenders and options, gathering required documentation, and submitting the application. The lender will review your financial situation and decide whether to approve the line of credit and on what terms.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.