Inflation-adjusted annuities play an essential role in retirement planning by providing a stable income stream that keeps up with the rising cost of living. An inflation-adjusted annuity is a financial product that provides a stream of income that increases with inflation. This type of annuity is designed to help individuals maintain their purchasing power over time, as the payments they receive will increase in response to rising prices. Inflation-adjusted annuities are typically offered by insurance companies and can be purchased as either a fixed or variable annuity. Inflation adjustment is crucial for preserving the purchasing power of annuity payments. By adjusting the payments for inflation, retirees can maintain their standard of living and protect themselves against the eroding effects of rising prices on their retirement income. There are two main types of inflation-adjusted annuities: fixed annuities and variable annuities. Fixed inflation-adjusted annuities provide a guaranteed income stream that increases by a certain percentage each year to keep pace with inflation. The initial payout for a fixed inflation-adjusted annuity is typically lower than that of a fixed annuity, but the payments will continue to increase over time to help maintain purchasing power. This type of annuity is suitable for individuals who prioritize stability and predictability in their retirement income. Variable inflation-adjusted annuities, on the other hand, offer a flexible income stream that fluctuates based on the performance of the underlying investments. The payments from a variable inflation-adjusted annuity may increase more quickly than those from a fixed annuity if the underlying investments perform well, but they may also decrease if the investments underperform. This type of annuity is suitable for individuals who are comfortable with investment risk and are looking for the potential for higher income growth. Inflation-adjusted annuities offer several advantages to retirees, including maintaining purchasing power, hedging against inflation risk, providing a stable income stream, and enhancing financial planning. One of the primary benefits of inflation-adjusted annuities is their ability to maintain purchasing power over time. As the cost of living increases, the annuity payments are adjusted to help retirees keep up with rising prices and maintain their standard of living. Inflation-adjusted annuities can help retirees hedge against inflation risk. By providing a guaranteed income stream that increases with inflation, these annuities protect retirees from the eroding effects of rising prices on their fixed-income investments. Inflation-adjusted annuities offer a stable income stream that can last a lifetime or a predetermined period. This can provide peace of mind for retirees, knowing that they will have a reliable source of income that will keep up with inflation throughout their retirement years. Inflation-adjusted annuities come with various features designed to protect retirees against inflation, such as Cost of Living Adjustments (COLA), annual increases based on inflation index, and different indexation methods. COLA is a common feature in inflation-adjusted annuities that automatically adjusts the annuity payments based on a specific inflation measure. This ensures that the annuity payments keep up with the cost of living, allowing retirees to maintain their purchasing power over time. Some inflation-adjusted annuities provide annual increases based on a specific inflation index, such as the Consumer Price Index (CPI). This ensures that the annuity payments are adjusted in line with the actual changes in the cost of living, offering more accurate protection against inflation. Inflation-adjusted annuities can use various indexation methods to adjust the annuity payments, such as fixed percentage increases, CPI, or custom indexes. Each method has its own advantages and disadvantages, and the choice depends on the retiree's goals and risk tolerance. When considering annuity options, it's essential to understand the differences between inflation-adjusted and fixed annuities in terms of initial payouts, income growth over time, risk and return considerations, and suitability for different retirement goals. Inflation-adjusted annuities typically have lower initial payouts compared to fixed annuities. This is because the insurance company must account for future increases in payments due to inflation. However, over time, the payouts from an inflation-adjusted annuity may surpass those from a fixed annuity as they continue to rise with inflation. Inflation-adjusted annuities offer income growth over time as the payments are adjusted for inflation, while fixed annuities provide a constant income stream that does not change. This means that inflation-adjusted annuities can help retirees maintain their purchasing power, while fixed annuities may lose value as the cost of living increases. Inflation-adjusted annuities can help retirees manage inflation risk by providing a guaranteed income stream that increases with inflation. Fixed annuities, on the other hand, may be more suitable for retirees who prioritize a higher initial income stream and are less concerned about the potential impact of inflation on their retirement income. Inflation-adjusted annuities may be a better fit for retirees who prioritize maintaining their purchasing power and hedging against inflation risk. In contrast, fixed annuities might be more suitable for those who prefer a higher initial income stream and are willing to accept the potential erosion of their purchasing power due to inflation. When evaluating inflation-adjusted annuities, it's essential to consider factors such as the financial strength of the insurer, fees and expenses, investment options, and payout options. It is crucial to choose an insurer with a strong financial rating to ensure the company's ability to meet its long-term obligations, especially when purchasing a product like an inflation-adjusted annuity designed to provide income over an extended period. Inflation-adjusted annuities may have higher fees and expenses compared to fixed annuities due to the additional complexity of adjusting the payments for inflation. It's essential to compare the fees and expenses of different annuity products to ensure that they align with your retirement goals and budget. Some inflation-adjusted annuities offer various investment options, allowing retirees to tailor their investments based on their risk tolerance and financial objectives. Understanding and comparing these investment options can help retirees make informed decisions when purchasing an inflation-adjusted annuity. Inflation-adjusted annuities can offer different payout options, such as lifetime payments, payments for a specific period, or joint and survivor payments. It's essential to carefully evaluate these options to select the one that best fits your retirement needs and goals. Understanding the tax implications of inflation-adjusted annuities, including tax-deferred growth, taxation of annuity payments, and the differences between qualified and non-qualified annuities, is essential when considering this financial product. Inflation-adjusted annuities offer tax-deferred growth, meaning that the earnings within the annuity are not taxed until they are withdrawn. This can be a significant advantage for retirees, as it allows their investments to grow without the drag of taxes. When annuity payments are received, a portion of each payment is considered a return of principal and is not taxable. The remaining portion, which represents the earnings, is subject to ordinary income tax. Understanding the tax treatment of annuity payments can help retirees plan for their tax liabilities during retirement. Inflation-adjusted annuities can be purchased with pre-tax (qualified) or after-tax (non-qualified) funds. Qualified annuities are purchased with funds from a tax-deferred retirement account, such as a 401(k) or IRA, and the entire annuity payment is taxable upon withdrawal. Non-qualified annuities are purchased with after-tax funds, and only the earnings portion of the payments is subject to taxes. It's important to understand the differences between these two types of annuities when planning for retirement. While inflation-adjusted annuities offer a guaranteed income stream that keeps up with inflation, there are alternative investments to consider, such as treasury inflation-protected securities (TIPS), dividend-paying stocks, real estate investments, and other inflation-hedging strategies. Treasury Inflation-Protected Securities are government-issued bonds that adjust their principal value based on changes in the Consumer Price Index. TIPS provide a low-risk way for investors to protect their investment principal from inflation while receiving a fixed interest rate. Dividend-paying stocks can be an effective way to generate income that may grow over time. Companies that consistently increase their dividend payments can help investors keep up with inflation, although the income generated by dividend stocks is not guaranteed and may fluctuate with market conditions. Real estate investments, such as rental properties or real estate investment trusts (REITs), can provide income that may keep pace with inflation. As property values and rental rates tend to rise with inflation, real estate investments can offer an effective hedge against inflation risk, although they come with their own set of risks and considerations. There are other strategies to hedge against inflation, such as investing in commodities or focusing on sectors that tend to perform well during periods of inflation, like energy or consumer staples. These strategies may involve higher risks and require more active management, but they can help protect your portfolio from the eroding effects of inflation. Inflation-adjusted annuities can play a valuable role in retirement planning by providing a stable income stream that keeps up with the cost of living. However, it's essential to carefully evaluate the features, benefits, fees, and tax implications of these financial products and consider alternative investments to create a diversified retirement portfolio that meets your financial goals and risk tolerance. Working with an experienced insurance broker can help you navigate the complex world of annuities and find the best solution for your retirement goals. Definition of Inflation-Adjusted Annuities

Types of Inflation-Adjusted Annuities

Fixed Inflation-Adjusted Annuities

Variable Inflation-Adjusted Annuities

Benefits of Inflation-Adjusted Annuities

Maintaining Purchasing Power

Hedging Against Inflation Risk

Providing a Stable Income Stream

Features of Inflation-Adjusted Annuities

Cost of Living Adjustments

Annual Increases Based on Inflation Index

Different Indexation Methods

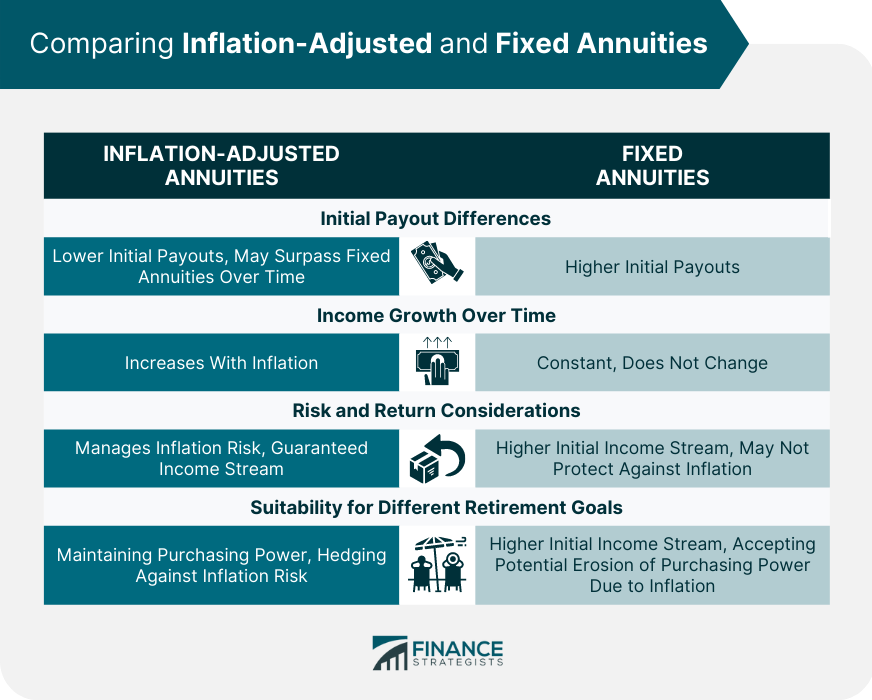

Comparing Inflation-Adjusted and Fixed Annuities

Initial Payout Differences

Income Growth Over Time

Risk and Return Considerations

Suitability for Different Retirement Goals

Factors to Consider When Purchasing Inflation-Adjusted Annuities

Financial Strength of the Insurer

Fees and Expenses

Investment Options

Payout Options

Tax Implications of Inflation-Adjusted Annuities

Tax-Deferred Growth

Taxation of Annuity Payments

Qualified vs. Non-Qualified Annuities

Alternatives to Inflation-Adjusted Annuities

Treasury Inflation-Protected Securities (TIPS)

Dividend-Paying Stocks

Real Estate Investments

Other Inflation-Hedging Strategies

Bottom Line

Inflation-Adjusted Annuities FAQs

Inflation-adjusted annuities are financial products that provide a stream of income that increases with inflation, helping to maintain purchasing power over time.

The two main types of Inflation-adjusted annuities are fixed annuities and variable annuities.

The benefits of Inflation-adjusted annuities include protecting against inflation, providing a guaranteed income stream, and potentially reducing taxes.

Yes, the taxation of Inflation-adjusted annuities can vary depending on the type of annuity and the individual's tax bracket. It is important to consult with a tax professional for specific guidance.

It depends on the terms of the annuity contract. Some Inflation-adjusted annuities may have penalties for early withdrawal, while others may allow for limited access to funds.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.