Retirement and estate planning are two critical financial aspects that need to be planned early enough in life to ensure a comfortable retirement and provide for your loved ones after your demise. Retirement planning involves saving enough money to sustain your living expenses when you stop working, while estate planning involves preparing for the distribution of your assets upon your death. Integrating the two planning processes can significantly maximize your wealth and legacy. Integrating retirement and estate planning can help ensure that you have enough retirement savings to last throughout your retirement. Retirement planning involves estimating your expenses during retirement and determining the amount of money needed to meet those expenses. Estate planning involves considering how your assets will be distributed and minimizing the tax burden on your heirs. By integrating the two processes, you can determine how much money is needed for retirement and how much money can be set aside for estate planning purposes. You can also identify investment strategies that generate enough income to sustain your retirement lifestyle and provide for your heirs. Integrating retirement and estate planning can help ensure that your loved ones are provided for after your death. Estate planning involves arranging for the distribution of your assets, while retirement planning involves determining how much money is needed for retirement expenses. By integrating the two processes, you can ensure that your assets are distributed according to your wishes, provide for your heirs, and minimize family conflict. You can also identify estate planning strategies that reduce estate taxes and transfer assets efficiently to your beneficiaries. Integrating retirement and estate planning can help minimize the tax burden on your heirs and maximize benefits. Estate planning involves minimizing estate taxes and ensuring that your beneficiaries receive the maximum benefit from your assets. Retirement planning involves identifying income streams that generate tax-efficient income. By integrating the two processes, you can identify tax-efficient investment strategies that generate income during retirement and reduce the tax burden on your heirs. You can also identify estate planning strategies that reduce estate taxes. Retirement and estate planning integration requires careful consideration of a variety of factors. These factors include asset distribution, beneficiary designations, healthcare and long-term care, and legacy planning. Asset distribution is a critical component of retirement and estate planning integration. It is important to determine how assets will be distributed upon death to ensure that your wishes are carried out and that your loved ones are provided for. A thorough understanding of asset distribution is especially important for individuals with complex asset portfolios. One key consideration is how assets will be distributed to beneficiaries. There are many options available, including lump sum payments, annuities, and structured payouts. It is also important to consider how assets will be divided among multiple beneficiaries, and whether certain beneficiaries will receive a greater share than others. Another important factor to consider is the tax implications of asset distribution. It is important to work with a financial professional to ensure that your assets are distributed in the most tax-efficient manner possible. Beneficiary designations are another important factor to consider in retirement and estate planning integration. Beneficiary designations are the instructions you provide to financial institutions regarding who will receive your assets upon your death. It is important to review and update your beneficiary designations regularly, as your life circumstances may change. Failure to update beneficiary designations can lead to unintended consequences, such as leaving assets to an ex-spouse or estranged family member. Additionally, it is important to ensure that beneficiary designations are consistent with the provisions of your will and other estate planning documents. Conflicts between beneficiary designations and other estate planning documents can lead to legal disputes and complications for your beneficiaries. Retirement and estate planning integration also involves planning for healthcare and long-term care needs. This includes planning for potential medical expenses in retirement, as well as the possibility of needing long-term care in the future. Long-term care can be a significant expense, with the cost of nursing home care often exceeding $100,000 per year. It is important to consider options for funding long-term care, such as long-term care insurance or Medicaid planning. In addition to planning for long-term care, it is important to have advance directives in place, such as a living will or healthcare power of attorney. These documents ensure that your wishes regarding medical treatment are respected if you become incapacitated and unable to make decisions for yourself. Finally, legacy planning is an important factor to consider in retirement and estate planning integration. Legacy planning involves the creation of a plan for leaving a meaningful legacy for future generations. Legacy planning can take many forms, such as charitable giving, creating a family foundation, or leaving a family business to future generations. It is important to work with a financial professional to ensure that your legacy planning goals are aligned with your overall retirement and estate planning goals. Retirement and estate planning integration can be achieved through the use of a variety of tools and strategies. These include trusts, wills, retirement accounts, and life insurance. Trusts are a powerful estate planning tool that can help protect assets and ensure their proper distribution. There are several types of trusts, including revocable living trusts, irrevocable trusts, and special needs trusts. Revocable living trusts are one of the most commonly used trusts because they allow the grantor to maintain control over the assets while alive, and the assets can easily pass to beneficiaries after the grantor's death. Irrevocable trusts can provide asset protection from creditors and minimize estate taxes, but once the assets are transferred to the trust, they cannot be retrieved. Special needs trusts can provide for beneficiaries with disabilities while preserving their eligibility for government benefits. A will is a legal document that directs how an individual's assets will be distributed after their death. A will can also designate guardians for minor children, specify funeral arrangements, and name an executor to manage the estate. Wills are an essential part of estate planning, and it's important to keep them up to date as life circumstances change. Retirement accounts are an important tool for retirement planning, and they can also be used for estate planning purposes. Some retirement accounts, such as traditional individual retirement accounts (IRAs) and 401(k)s, allow for tax-deferred growth, which can help maximize savings. Additionally, retirement accounts can be used to pass assets to beneficiaries after death. It's important to consider the tax implications of retirement accounts when developing an estate plan. Life insurance is another tool that can be used in both retirement and estate planning. Life insurance policies can provide a source of income for loved ones after the policyholder's death, which can help provide financial security. Additionally, life insurance can be used to pay estate taxes or provide liquidity to an estate. Retirement and estate planning can be complex, and it's often helpful to work with professionals in the field. Financial advisors, attorneys, and accountants can provide guidance and advice to ensure that retirement and estate planning goals are met. Financial advisors can help develop retirement and estate plans that align with individual financial goals. They can also provide advice on investments and strategies to maximize retirement savings. Additionally, financial advisors can help identify potential tax implications of retirement and estate planning decisions. Attorneys are essential in estate planning, and they can help develop wills and trusts that accurately reflect an individual's wishes. They can also provide guidance on how to minimize taxes and ensure that assets are properly distributed after death. Attorneys can also help with the legal aspects of retirement planning, such as developing durable power of attorney documents. Accountants can provide guidance on the tax implications of retirement and estate planning decisions. They can help minimize taxes and ensure that retirement accounts and other assets are distributed in the most tax-efficient way possible. Additionally, accountants can help with the financial aspects of legacy planning and charitable giving. While retirement and estate planning integration is important, there are potential challenges and pitfalls that individuals should be aware of. One common mistake is failing to regularly update estate planning documents, such as wills and trusts. As life circumstances change, it is important to review and update these documents to ensure that they accurately reflect the individual's wishes. Another challenge is inadequate retirement savings. Many individuals may not be saving enough for retirement, which can lead to financial hardship later in life. It is important to set retirement savings goals and regularly review and adjust them as needed. Finally, lack of communication with beneficiaries can also pose a challenge. It is important to communicate with loved ones about estate planning decisions to avoid misunderstandings and disputes after the individual's death. In conclusion, retirement and estate planning integration is an important part of financial planning that can help ensure adequate retirement savings, provide for loved ones after death, minimize taxation and maximize benefits, and avoid probate. By considering factors such as asset distribution, beneficiary designations, healthcare and long-term care, and legacy planning, individuals can create a comprehensive retirement and estate plan that meets their unique needs and goals. It is also important to seek the assistance of professionals, such as financial advisors, estate planning attorneys, and accountants, and to be aware of potential challenges and pitfalls, such as failing to update estate planning documents, inadequate retirement savings, and lack of communication with beneficiaries. By following these recommendations and creating a comprehensive retirement and estate plan, individuals can achieve financial security and peace of mind for themselves and their loved ones.Overview of Retirement and Estate Planning Integration

Importance of Retirement and Estate Planning Integration

Ensuring Adequate Retirement Savings

Providing for Loved Ones After Death

Minimizing Taxation and Maximizing Benefits

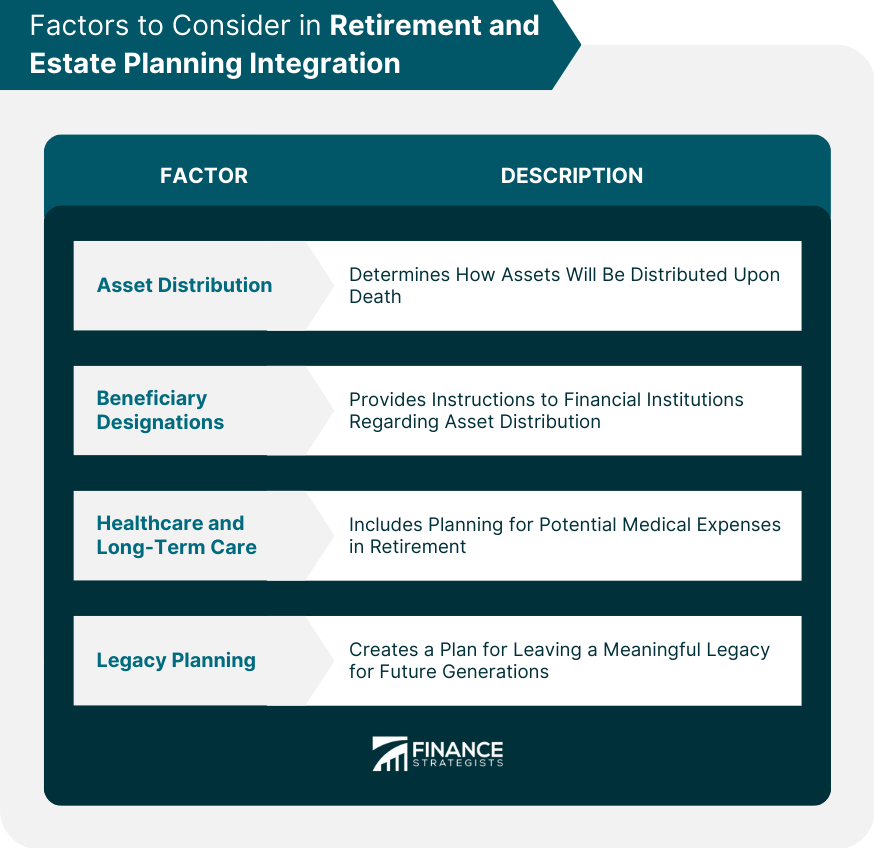

Factors to Consider in Retirement and Estate Planning Integration

Asset Distribution

Beneficiary Designations

Healthcare and Long-Term Care

Legacy Planning

Retirement and Estate Planning Tools and Strategies

Trusts

Wills

Retirement Accounts

Life Insurance

Professional Assistance in Retirement and Estate Planning Integration

Financial Advisors

Attorneys

Accountants

Potential Challenges and Pitfalls

Bottom Line

Retirement and Estate Planning Integration FAQs

Retirement and estate planning integration is the process of creating a comprehensive plan that maximizes your savings, minimizes taxes, and protects your legacy for both your retirement and estate planning goals.

Retirement and estate planning integration is important because it ensures that your retirement goals and estate planning goals are aligned, and that you are prepared for any unforeseen circumstances that may arise.

Strategies for retirement and estate planning integration include creating a will, establishing a trust, reviewing your beneficiaries, considering long-term care insurance, and developing a comprehensive retirement income plan.

It's never too early to start thinking about retirement and estate planning integration. Ideally, you should start thinking about it in your 40s or 50s, but it's never too late to start.

While it's possible to create a retirement and estate plan on your own, it's highly recommended to seek the advice of a professional financial planner or estate planning attorney who can help you navigate the complexities of the process and ensure that your plan is tailored to your specific needs and goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.