Family Wealth Transfer Planning refers to the process of creating a strategic and comprehensive plan for transferring wealth from one generation to the next within a family. It involves assessing the current financial situation of the family, identifying goals and objectives, and developing a plan that takes into account tax implications, legal considerations, and the specific needs and preferences of each family member. The goal of family wealth transfer planning is to minimize taxes, ensure that the assets are distributed according to the family's wishes, and maintain the financial security of future generations. It may involve the use of trusts, gifting, estate planning, and other financial strategies to achieve these goals.

The first step in family wealth transfer planning is to create an inventory of all assets and liabilities. This includes real estate, investments, business interests, personal property, and debts. By having a clear understanding of the family's financial situation, it becomes easier to develop a comprehensive plan for transferring wealth to the next generation. For families with business interests, it is essential to determine the fair market value of the business. This may involve hiring an appraiser or business valuation expert to provide an accurate assessment. This information will be crucial for developing strategies for transferring ownership and control to the next generation. In addition to identifying and valuing assets, families should also analyze their investment portfolios to ensure they align with their long-term goals and risk tolerance. This may involve rebalancing investments, diversifying holdings, or seeking professional advice on investment strategies. One strategy for transferring wealth is through annual exclusion gifts. These gifts can be made to any number of individuals without incurring a gift tax, up to a specified limit per recipient per year. This allows families to transfer wealth incrementally and minimize tax implications. For larger gifts that exceed the annual exclusion limit, families may consider making taxable gifts. Although these gifts may incur gift tax, they can help reduce the overall value of the estate and potentially minimize estate taxes in the future. Grantor Retained Annuity Trusts (GRATs) are specialized trusts that allow the grantor to transfer assets to beneficiaries while retaining an annuity for a specified term. At the end of the term, the remaining assets in the trust pass to the beneficiaries, often with significant tax savings. Irrevocable Life Insurance Trusts (ILITs) are trusts specifically designed to hold life insurance policies. By transferring ownership of a life insurance policy to an ILIT, families can potentially minimize estate taxes and provide additional financial security for beneficiaries. Charitable Remainder Trusts (CRTs) are trusts that provide a stream of income to the grantor or other designated beneficiaries for a specified period, with the remaining assets ultimately passing to a designated charity. CRTs can offer significant tax benefits, including income tax deductions and avoidance of capital gains taxes. Family Limited Partnerships (FLPs) are legal entities that allow families to transfer business interests or other assets to younger generations while maintaining control over the assets. This can be an effective strategy for minimizing taxes and providing for the orderly transfer of wealth. When transferring wealth to the next generation, families must consider the potential impact of gift and generation-skipping transfer taxes. These taxes can be significant, but proper planning can help minimize their effect on the overall value of the assets being transferred. Transferring assets can also trigger capital gains tax implications. Families should work with tax professionals to understand and minimize the potential tax impact of wealth transfers. In addition to gift and capital gains taxes, income tax considerations must be taken into account when planning wealth transfers. This may involve structuring trusts or other wealth transfer vehicles to minimize income tax implications for both the grantor and the beneficiaries. When planning for wealth transfer, it is essential to consider the family's values and legacy. This may involve discussing the family's philanthropic goals, educational priorities, or other long-term objectives. By incorporating these values into the wealth transfer plan, families can help ensure their legacy is preserved for future generations. Involving the next generation in the wealth transfer planning process can help them develop a sense of responsibility and understanding of the family's financial goals. This may involve educating them about the family's assets, discussing their role in the management of the wealth, and providing opportunities for them to participate in decision-making processes. Family conflicts can arise during the wealth transfer planning process, particularly when decisions involve the distribution of assets among family members. Addressing these conflicts proactively, through open communication and a commitment to fairness, can help preserve family harmony and ensure the successful transfer of wealth. For families with a strong commitment to philanthropy, establishing a family foundation can be an effective way to support charitable causes and leave a lasting legacy. Family foundations can offer significant tax benefits and provide a platform for family members to work together to achieve their philanthropic objectives. Donor-advised funds are another option for families looking to support charitable causes. These funds allow families to make tax-deductible contributions to a sponsoring organization, which then distributes the funds to the family's chosen charities over time. Donor-advised funds can be a flexible and cost-effective alternative to establishing a family foundation. In addition to establishing a family foundation or donor-advised fund, families may consider other charitable giving strategies, such as making direct gifts to charities, creating charitable remainder trusts, or incorporating charitable bequests into their wills. For families with business interests, developing a comprehensive succession plan is a crucial component of wealth transfer planning. This may involve identifying potential successors, training and mentoring future leaders and establishing a timeline for the transfer of ownership and control. In addition to identifying successors, families must also invest in preparing the next generation of leaders for their roles within the family business. This may involve providing them with education, training, and opportunities to gain experience and develop their skills. As part of the business succession planning process, families should also consider their exit strategies. This may include selling the business, merging with another company, or transitioning to a new ownership structure. Planning for these eventualities can help ensure the family's financial well-being and the continued success of the business. Wealth transfer plans should be reviewed and adjusted regularly to account for changes in family circumstances, financial goals, and tax laws. By keeping plans up-to-date, families can ensure they remain effective and aligned with their objectives. As tax laws and regulations change, families must adjust their wealth transfer strategies accordingly. Working with professional advisors can help families stay informed about these changes and make the necessary adjustments to their plans. Changes in family circumstances, such as marriages, divorces, births, or deaths, can also have an impact on wealth transfer plans. Families should update their plans to reflect these changes and ensure their objectives continue to be met. Successful family wealth transfer planning often requires the expertise of a team of professionals, including attorneys, tax advisors, financial planners, and investment advisors. These experts can provide guidance and support throughout the planning process, helping families navigate the complexities of wealth transfer and minimize potential pitfalls. Once a team of professional advisors is assembled, it is essential to ensure effective communication and coordination among them. This will help ensure that all aspects of the wealth transfer plan are integrated and working towards the family's overall objectives. Professional advisors play a crucial role in implementing and managing wealth transfer plans. They can help families set up trusts, draft legal documents, manage investments, and handle tax filings. By working closely with these experts, families can help ensure the seamless execution of their wealth transfer plans and safeguard their financial legacy for future generations. To measure the success of wealth transfer plans, families should establish Key Performance Indicators (KPIs) that align with their goals and objectives. These KPIs can help track progress over time and provide valuable insights into the effectiveness of the plan. Regularly reviewing KPIs and making necessary adjustments to wealth transfer strategies can help ensure that the plan remains on track and continues to meet the family's objectives. This may involve reallocating assets, adjusting trust structures, or modifying charitable giving strategies based on performance and changing circumstances. Involving family members in the evaluation process can help ensure that the wealth transfer plan remains relevant and meaningful to all stakeholders. This may involve holding family meetings, sharing KPI reports, and discussing potential adjustments to the plan. Educating future generations about wealth management is crucial for the long-term success of wealth transfer plans. This may involve providing financial literacy education, discussing investment strategies, and teaching younger family members about the responsibilities associated with managing family wealth. Families can help prepare future generations for their roles in managing family wealth by encouraging active participation in family finances. This may involve involving younger family members in financial decision-making processes, assigning them responsibilities related to the family's investments, or providing opportunities for them to gain hands-on experience in managing assets. By instilling a sense of stewardship and responsibility in future generations, families can help ensure the successful transfer of wealth and the preservation of their financial legacy. This may involve discussing the family's values and objectives, emphasizing the importance of prudent wealth management, and fostering a culture of fiscal responsibility within the family. Family wealth transfer planning is a critical process that ensures the successful transfer of assets and the preservation of financial legacy for future generations. This comprehensive approach involves assessing family wealth, employing various wealth transfer strategies, understanding tax implications, and addressing family dynamics and communication. Furthermore, incorporating philanthropic goals, business succession planning, and working with professional advisors contribute to a well-rounded wealth transfer plan. Regular review and adjustment of these plans, along with educating and involving future generations in wealth management, are crucial for maintaining the plan's effectiveness and relevance. By carefully considering these key concepts and fostering a sense of stewardship and responsibility, families can effectively navigate the complexities of wealth transfer and secure their financial legacy for generations to come.What Is Family Wealth Transfer Planning?

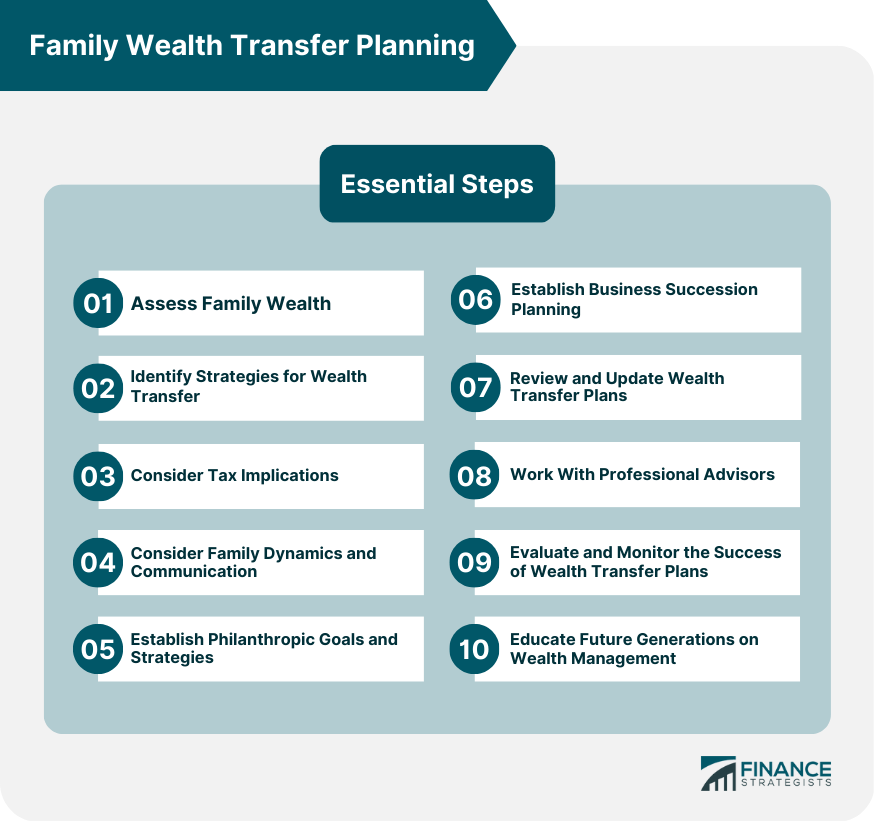

Assessing Family Wealth

Identifying Assets and Liabilities

Valuing Family Business Interests

Analyzing Investment Portfolios

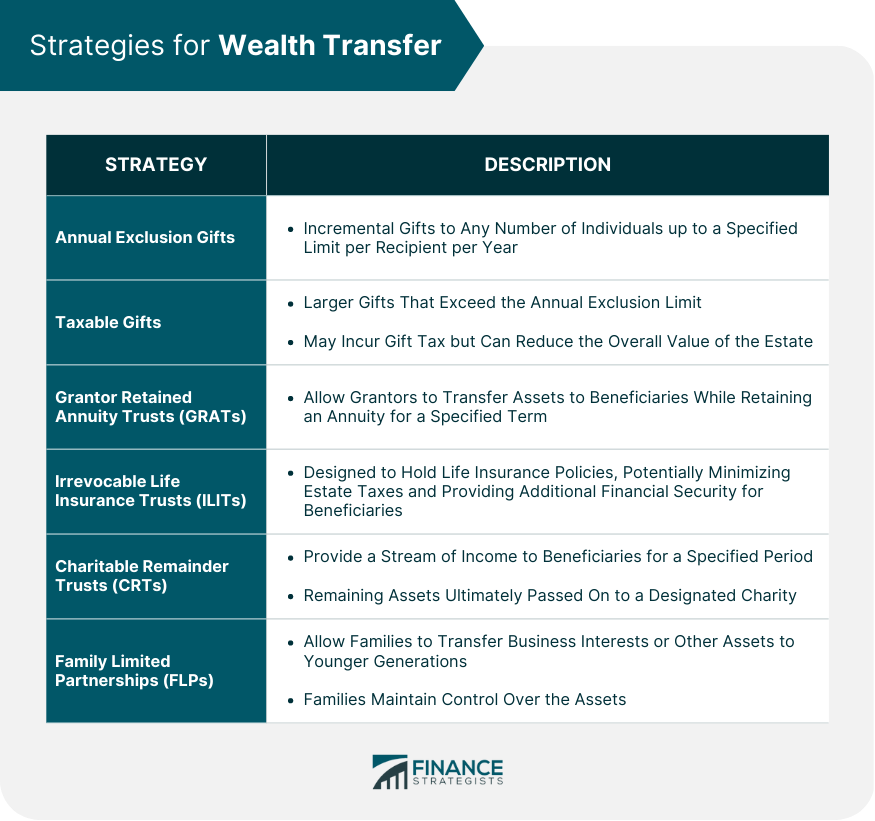

Strategies for Wealth Transfer

Gifting and Lifetime Transfers

Annual Exclusion Gifts

Taxable Gifts

Grantor Retained Annuity Trusts (GRATs)

Trusts and Other Wealth Transfer Vehicles

Irrevocable Life Insurance Trusts (ILITs)

Charitable Remainder Trusts (CRTs)

Family Limited Partnerships (FLPs)

Tax Considerations

Gift and Generation-Skipping Transfer Taxes

Capital Gains Tax Implications

Income Tax Considerations

Family Dynamics and Communication

Addressing Family Values and Legacy

Involving the Next Generation

Managing Family Conflicts

Philanthropic Goals and Strategies

Establishing a Family Foundation

Donor-Advised Funds

Charitable Giving Strategies

Business Succession Planning

Developing a Succession Plan

Preparing the Next Generation of Leaders

Exit Strategies

Review and Update Wealth Transfer Plans

Regularly Review and Adjust Strategies

Responding to Changes in Tax Laws and Regulations

Addressing Changes in Family Circumstances

Working With Professional Advisors

Assembling a Team of Experts

Coordinating With Legal, Tax, and Financial Advisors

Ensuring Seamless Implementation and Management of Plans

Evaluating and Monitoring the Success of Wealth Transfer Plans

Establishing Key Performance Indicators (KPIs)

Periodic Review of KPIs and Adjustments

Involving Family Members in the Evaluation Process

Educating Future Generations on Wealth Management

Financial Literacy and Education

Encouraging Active Participation in Family Finances

Fostering a Sense of Stewardship and Responsibility

Conclusion

Family Wealth Transfer Planning FAQs

The main purpose of family wealth transfer planning is to strategically allocate assets and resources to minimize tax liabilities, maximize the value passed down to heirs, and preserve the family's financial legacy for future generations.

Family wealth transfer planning involves employing various strategies, such as gifting, setting up trusts, and creating family limited partnerships, to minimize gift, estate, and capital gains taxes, ultimately maximizing the value of the assets transferred to the next generation.

Addressing family dynamics and communication is crucial in family wealth transfer planning because it helps preserve family harmony, ensures the plan aligns with the family's values and objectives, and involves the next generation in the decision-making process, fostering a sense of responsibility and understanding.

Professional advisors, such as attorneys, tax advisors, financial planners, and investment advisors, provide expert guidance and support throughout the wealth transfer planning process. They help families navigate the complexities of wealth transfer, minimize potential pitfalls, and ensure seamless implementation and management of plans.

Business succession planning is a vital component of family wealth transfer planning for families with business interests. It involves developing a comprehensive plan for transferring ownership and control to the next generation, identifying and preparing successors, and establishing exit strategies, ensuring the family's financial well-being and the continued success of the business.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.