Closing a bank account is a decision often prompted by several factors. Poor customer service can be a significant deterrent, leading customers to seek banks that prioritize their needs. High fees or hidden charges, such as those for maintenance, ATM usage, or overdraft, can become burdensome over time. Better interest rates, beneficial features, or offers from other banks can also draw individuals to close their current accounts in favor of a more advantageous one. Moreover, if a bank's technology is outdated and lacks modern conveniences like mobile banking or instant alerts, customers may move to more tech-savvy banks. Life events can also dictate this choice; relocating to a region where your current bank doesn't have a presence or coalescing accounts after marriage might necessitate account closure. Lastly, simplifying finances by consolidating multiple accounts into one could be another compelling reason. Your journey to closing a bank account begins with a simple step: initiating the closure process. Depending on your bank, you can either visit your local branch or call their customer service hotline. To ensure you have a seamless experience, make sure your account has no negative balance. Remember, you cannot close an account with pending debts. Your bank will appreciate timely communication and may provide additional guidance during this initial phase. The next critical step is transferring the remaining funds from the account you want to close. This process can be accomplished through an online transfer, writing a check, or a cash withdrawal. If possible, consider transferring the funds to another account under your name to ensure the money remains within your control. Before moving funds, make sure all pending transactions have cleared to avoid an account overdraft. Understanding your bank's transfer timelines can prevent any unforeseen challenges during this step. Before you close your account, take time to review your transaction history. You want to ensure there are no pending transactions or automatic payments tied to the account. Any overlooked bills or subscriptions could potentially hinder your closure process and even result in charges. Redirect automatic payments and direct deposits to your new account to ensure continuity of payments and income. This thorough check can save you from future headaches related to unpaid bills or unnoticed transactions. Once you've transferred your funds and checked for pending transactions, you can now formally request your account closure. This step may involve submitting a written request or filling out an account closure form. Ensure you obtain a confirmation of your account closure request. This document will be important in case there are any discrepancies or disputes later. It's also wise to inquire about the estimated time frame for the closure to set your expectations right. After the formal request to close the account, it's a good practice to destroy any debit or credit cards linked to the account. Shred or cut up the cards to avoid potential misuse. Remember, merely cutting up your cards does not close your account; it's an additional step for your financial security. Safely disposing of physical cards also ensures you're not leaving any room for potential identity theft. Closing a bank account is not a decision to take lightly. Several factors need your attention before you finalize the closure. Before you proceed with the account closure, familiarize yourself with any potential fees and penalties. Some banks impose an early closure fee, especially if the account is closed shortly after it was opened. Additionally, be aware of any monthly maintenance fees if you're keeping a minimal balance in the account before closure. Reading through your bank's terms and conditions or consulting a representative can give you clarity on any hidden charges. Take into consideration how much interest you might lose or gain by closing the account. If the account has a significant accrued interest, weigh the benefits of transferring your funds to a similar interest-bearing account versus the potential losses. Interest can accumulate daily, so consider the time frame of your closure to maximize your benefits. It's essential to have another bank account ready to replace the crucial functions of the one you're closing. This step ensures that you have a place to deposit funds, pay bills, and handle other financial transactions without interruption. This backup can act as a financial safety net, ensuring that your monetary flow remains undisrupted. Closing a bank account might feel like the only option in certain situations, but it's worth considering some alternatives. If the issue is related to account fees or account complexity, ask your bank if you can downgrade to a simpler, potentially less expensive account. This option can save you the hassle of changing account numbers and moving money around. Many banks offer a variety of account types tailored to different needs; you might find a perfect fit. Consider switching to a different type of account within the same bank. For instance, if a checking account no longer serves your needs, you could switch to a savings or money market account. This can offer benefits like better interest rates or reduced fees tailored to your changing financial needs. If your concern is about account misuse, consider temporarily freezing the account. This option prevents new charges while allowing recurring transactions to continue. It's a practical choice if you believe you might need the account in the near future or are uncertain about closing it permanently. Even after your account is closed, you need to ensure everything is in order with a post-closure checklist. Monitor your closed account for any unexpected activity or charges. If you spot any, contact your bank immediately. The bank should resolve any unauthorized transactions, but only if they are identified promptly. Monitoring can be done through online banking platforms or periodic statements, ensuring your peace of mind. It's crucial to update all payment methods associated with the old account. Replace old account details for services, subscriptions, and utilities to ensure continuity. Consistency in payments helps in maintaining a good credit score and ensures you don't miss out on any essential services. Always keep your closure documentation for future reference. This paperwork serves as proof that you've taken all necessary steps to close your account and can be helpful if disputes arise. A well-organized financial record is also beneficial for any future banking or financial endeavors you might undertake. After closing a bank account, make sure there are no negative marks on your credit report related to the account closure. Mistakes can happen, and early detection allows you to rectify them with the credit bureau or your bank. Regularly reviewing your credit report helps you stay on top of your financial standing. Closing a bank account requires careful consideration and attention to detail. Factors like poor customer service, high fees, outdated technology, and life events influence this decision. Follow immediate steps like initiating closure, transferring funds, checking transactions, requesting closure, and destroying cards. Consider fees, interest, and have a backup account before finalizing closure. Explore alternatives like downgrading or switching accounts within the same bank or temporarily freezing the account. After closure, monitor for activity, update payment methods, keep documentation, and review your credit report. By following these steps, individuals can effectively close their bank accounts and smoothly transition to new financial arrangements. Take control of your banking experience and explore a wide range of banking services that cater to your needs. Find a bank that prioritizes customer service, offers lower fees, and utilizes advanced technology.Understanding the Reasons for Closing a Bank Account

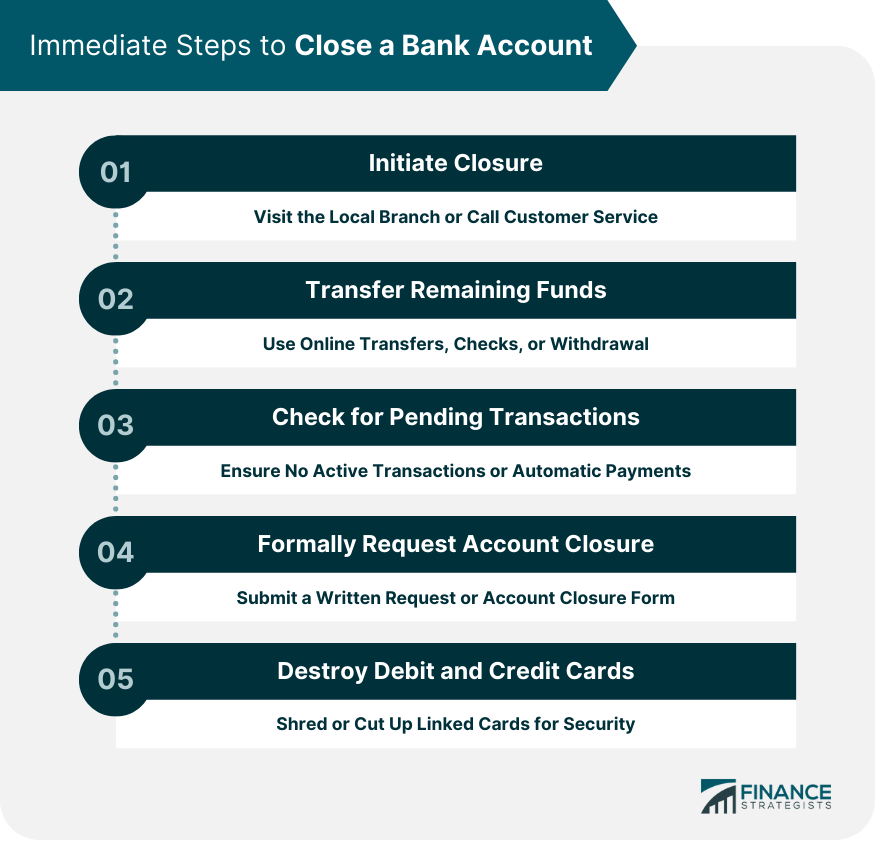

Immediate Steps to Close a Bank Account

Initiate the Closing Process

Transfer Remaining Funds

Check for Pending Transactions or Automatic Payments

Formally Request Account Closure

Destroy Debit and Credit Cards

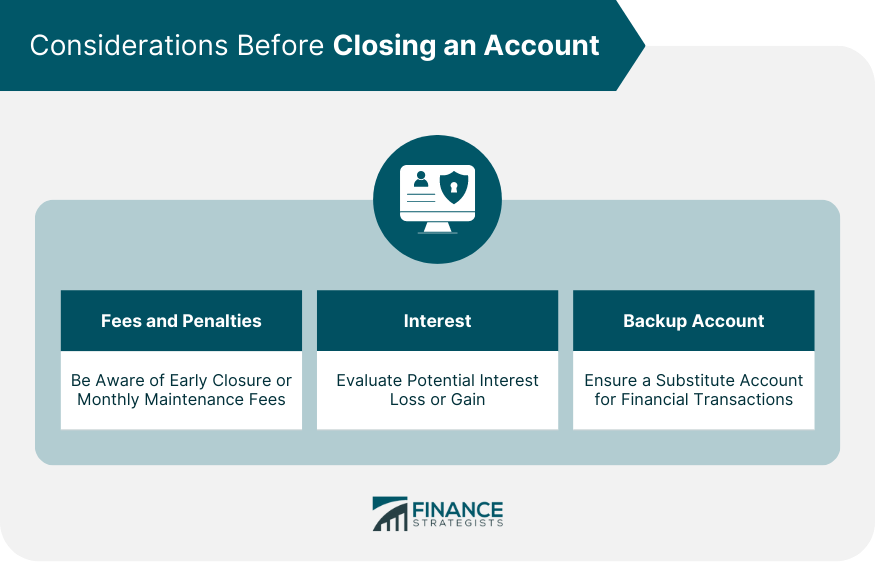

Considerations Before Closing an Account

Fees and Penalties

Interest

Backup Account

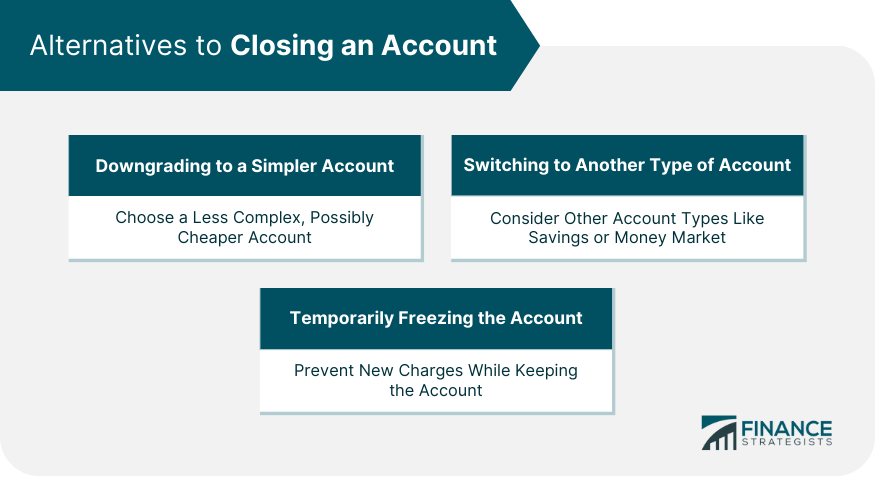

Alternatives to Closing an Account

Downgrading to a Simpler Account

Switching to Another Type of Account

Temporarily Freezing the Account

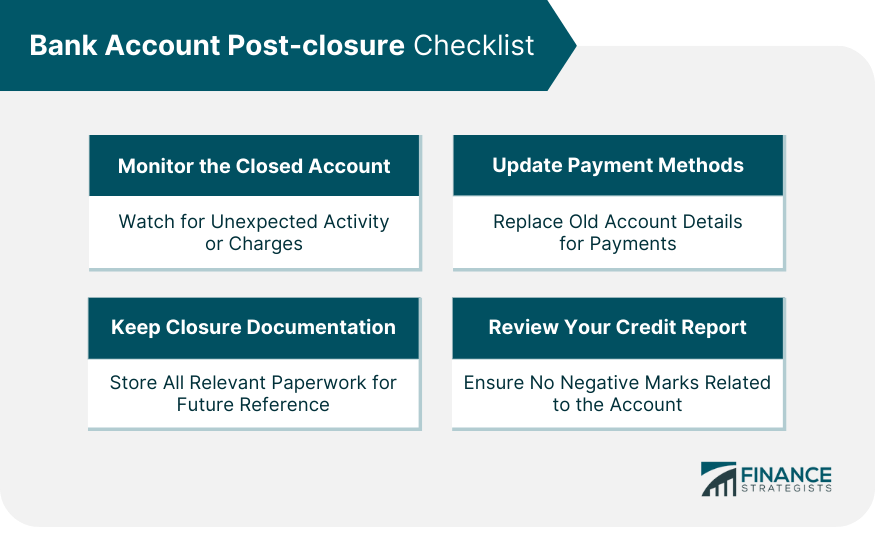

Bank Account Post-closure Checklist

Monitor the Closed Account

Update Payment Methods

Keep Closure Documentation

Review Your Credit Report

Bottom Line

How to Close a Bank Account FAQs

Initiate the closure by visiting your local branch or calling the bank's customer service hotline.

Transfer the remaining funds to another account, ensuring all pending transactions have cleared.

Some banks might impose early closure or monthly maintenance fees. Always check the terms before proceeding.

Alternatives include downgrading to a simpler account, switching to another type of account, or temporarily freezing the account.

Monitoring ensures there are no unauthorized transactions, allowing timely rectification if any issues arise.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.