Blockchain-based timestamping is a method of verifying the exact time and date at which a certain digital event took place. This technology is rooted in the capabilities of blockchain technology - a decentralized, distributed ledger that can store data across multiple nodes in a network. A blockchain-based timestamping system can record timestamps on data, documents, and transactions, providing proof of their existence and state at a particular point in time. This form of timestamping uses cryptographic algorithms to provide a secure, verifiable, and tamper-proof timestamp. Blockchain’s decentralized nature further ensures that these timestamps cannot be changed or manipulated by any single entity, thereby enhancing the integrity of the timestamped data. Blockchain is renowned for its security and ability to create tamper-proof timestamps. The security of blockchain timestamps is grounded in its distributed, decentralized architecture and the use of cryptographic mechanisms. Each piece of data in a blockchain network is hashed and added to a block, which is then linked to the previous block in a chronological chain. This structure, combined with cryptographic functions, ensures that once a block is added to the chain, its content, including the timestamp, cannot be altered without changing the content of all subsequent blocks. Additionally, blockchain's consensus mechanisms further bolster the security of timestamps. These mechanisms require network participants to agree on the validity of new blocks before they are added to the chain. This process prevents fraudulent transactions or data manipulation, thus ensuring the accuracy and immutability of blockchain timestamps. The consensus mechanism in blockchain technology serves a critical role in ensuring that all nodes in the network agree on the validity of transactions and timestamps. Essentially, it is a protocol that maintains the reliability, security, and integrity of the blockchain by making sure all participating nodes agree on the state of the distributed ledger. There are several types of consensus mechanisms, including Proof of Work (PoW), Proof of Stake (PoS), and Delegated Proof of Stake (DPoS), among others. Each type has its strengths and weaknesses, but they all serve the same fundamental purpose: maintaining consensus across the blockchain network. Cryptographic hashing is a function that takes an input and returns a fixed-size string of bytes, typically a hash code. This process is integral to blockchain-based timestamping as it provides a unique identifier for every transaction and timestamp. In the context of blockchain, hashing serves two main purposes: ensuring data integrity and securing data. It guarantees that the data contained in each block has not been tampered with. If any change occurs, the hash of the block changes significantly, alerting the network to potential fraud. Distributed Ledger Technology is the foundation upon which blockchain technology is built. DLT is a decentralized database managed by multiple participants, known as nodes. In the case of blockchain-based timestamping, DLT allows the timestamp to be stored on multiple nodes across the network, making it near-impossible to alter or tamper with the data. Moreover, DLT provides transparency to all network participants. Every node in the network has access to the entire blockchain and can verify the timestamps independently. This distributed and transparent nature of the ledger reinforces the security and trustworthiness of blockchain-based timestamps. Because every transaction and its associated timestamp are stored on a blockchain, they can be viewed by all participants in the network. This feature increases the level of trust among users and allows for a high degree of auditability. When it comes to auditing, blockchain-based timestamps provide a clear, immutable history of transactions. This quality can significantly simplify the audit process, as auditors can trace and verify transactions quickly and accurately. The transparency and traceability provided by blockchain-based timestamping can thus improve accountability and confidence in digital transactions. Blockchain technology ensures that once a record has been written onto the blockchain, it cannot be altered or deleted. This immutability characteristic is particularly valuable for timestamping, as it guarantees the integrity of the timestamped data, ensuring that records remain unaltered and intact over time. The immutability of blockchain also reinforces the validity and reliability of data. It ensures that once a timestamp has been recorded, it will provide a truthful and unalterable reference to when the associated data or transaction was recorded. The risk of fraudulent activity or data manipulation is significantly reduced. Blockchain-based timestamping can significantly improve verification and authentication processes. Since the blockchain stores a verifiable and immutable record of transactions and their associated timestamps, users can quickly verify the authenticity of the data. Moreover, since all transactions are timestamped and stored on the blockchain, it becomes easier to authenticate and validate the sequence of events. In addition to this, the decentralized nature of blockchain technology eliminates the need for third-party intermediaries for verification purposes. This decentralization can result in faster, more efficient authentication processes, as it allows for direct peer-to-peer verification. Blockchain-based timestamping can provide a transparent, immutable, and verifiable record of transactions, which can be incredibly beneficial for financial institutions that must comply with stringent regulations. For example, the timestamps can serve as an immutable audit trail, allowing financial institutions to demonstrate to regulators that they have adhered to the required processes at the required times. Furthermore, the immutable nature of the blockchain ensures that all records and evidence of compliance cannot be tampered with or altered, thus providing robust proof of compliance. One of the key challenges facing blockchain-based timestamping is scalability. As the number of transactions increases, so too does the size of the blockchain. This growth can lead to increased computational requirements, which in turn can lead to performance issues, especially in terms of transaction speed and storage capacity. Moreover, certain consensus mechanisms, such as Proof of Work, can be computationally intensive and slow, particularly as the network grows. This intensity can limit the number of transactions that can be processed per second, potentially slowing down the system and making it less suitable for applications that require high-speed data processing. While blockchain-based timestamping can assist with regulatory compliance, it also raises new regulatory and legal issues. Since blockchain is a decentralized system, it lacks a central authority, which can create challenges in terms of jurisdiction and oversight. Moreover, as a relatively new technology, there is often a lack of clear regulation and legal precedent relating to blockchain. This lack of clarity can create uncertainties and potential legal risks for users. Additionally, the immutable nature of blockchain data can conflict with data protection laws, such as the right to be forgotten stipulated by the General Data Protection Regulation (GDPR) in the EU. Blockchain’s transparency, while being one of its strengths, also raises privacy concerns. In a public blockchain, all transactions and associated timestamps are visible to all participants in the network. This visibility could potentially expose sensitive information, leading to privacy issues. Data protection is also a concern, particularly in relation to personal data. While the data on a blockchain is secure from tampering, it does not prevent the data from being viewed if the network is public. Furthermore, since the data on the blockchain is immutable, it could potentially conflict with data protection laws that require the ability to correct or delete personal data. Despite the potential benefits of blockchain-based timestamping, there are significant challenges related to its adoption and integration into existing systems. For many organizations, the shift to blockchain can be complex and costly, requiring a significant investment in technology and skills. In addition, interoperability can be an issue. Integrating blockchain-based timestamping with existing IT systems may be a complex task, and incompatibility issues can arise. There are also challenges associated with ensuring that different blockchain systems can work together effectively, particularly in industries like finance, where seamless interaction between different systems is crucial. Blockchain-based timestamping can revolutionize financial transactions by providing a secure, transparent, and tamper-proof record of when each transaction was made. This feature can help prevent fraud and double-spending, enhancing the overall integrity of financial systems. Moreover, timestamping can simplify the reconciliation process. As each transaction is timestamped and recorded on the blockchain, discrepancies between different parties' records can be easily identified and resolved. This transparency can significantly reduce disputes and enhance trust among parties. Blockchain-based timestamping can be instrumental in verifying the authenticity of financial documents and contracts. By timestamping a document or contract at the time of its creation or modification, the blockchain can provide a tamper-proof record that can prove its validity and the time of its existence. This feature can be particularly useful in the case of smart contracts – self-executing contracts with the terms of the agreement directly written into code. Blockchain-based timestamping can provide an immutable record of the terms at the point of contract initiation and any changes that may have occurred, thereby enhancing the security and trustworthiness of such contracts. Blockchain-based timestamping can significantly enhance the verification of the origin and ownership of financial assets. By timestamping asset transactions, blockchain can provide a transparent, immutable record of asset provenance and ownership changes. This capability is particularly valuable for assets such as securities, real estate, and even digital assets like cryptocurrencies. It can prevent fraudulent activities like double-spending and counterfeiting, and it can also streamline the due diligence process during asset transfers. Blockchain-based timestamping can significantly simplify regulatory reporting and compliance in the financial sector. It can provide an immutable, auditable record of transactions and their associated timestamps, which can be used as solid evidence for regulatory reporting. This feature can prove to financial regulators that transactions were performed in compliance with regulations. By providing an immutable audit trail, blockchain-based timestamping can increase transparency, reduce the risk of regulatory breaches, and potentially decrease the time and resources spent on regulatory reporting. Blockchain-based timestamping is the method of verifying the exact time and date of a digital event, offers numerous benefits and brings forth several limitations in the realm of finance. Blockchain-based timestamping uses blockchain technology, a decentralized ledger, to record timestamps on data, documents, and transactions, providing proof of their existence and state at a specific time. The benefits of blockchain-based timestamping include enhanced transparency and auditability, immutable record-keeping, efficient verification and authentication processes, and streamlined regulatory compliance. However, limitations such as scalability and performance issues, regulatory and legal considerations, privacy and data protection concerns, and adoption and integration challenges exist. Blockchain-based timestamping has found valuable use cases in finance, including timestamping financial transactions, ensuring the authenticity of documents and contracts, and verifying the origin and ownership of assets.What is Blockchain-Based Timestamping?

How Blockchain Ensures Secure and Tamper-Proof Timestamps

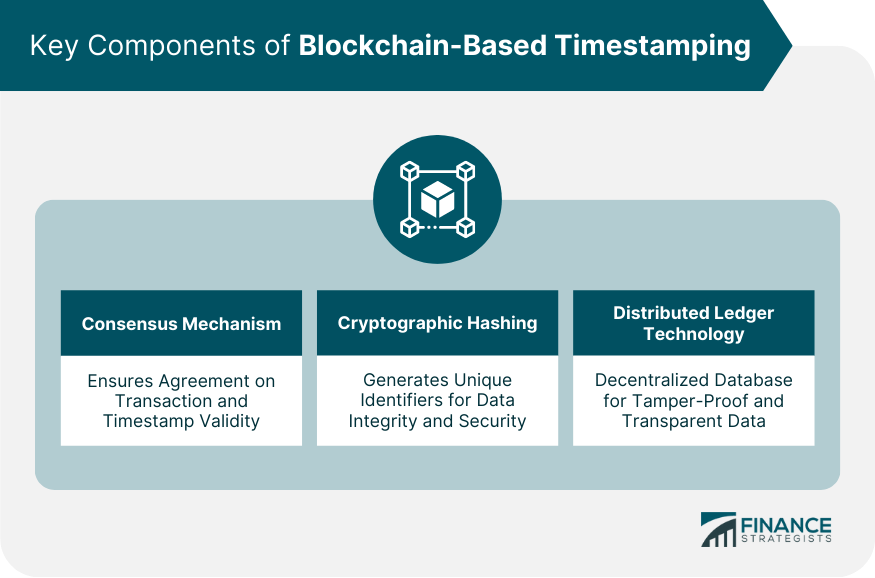

Key Components of Blockchain-Based Timestamping

Consensus Mechanism

Cryptographic Hashing

Distributed Ledger Technology

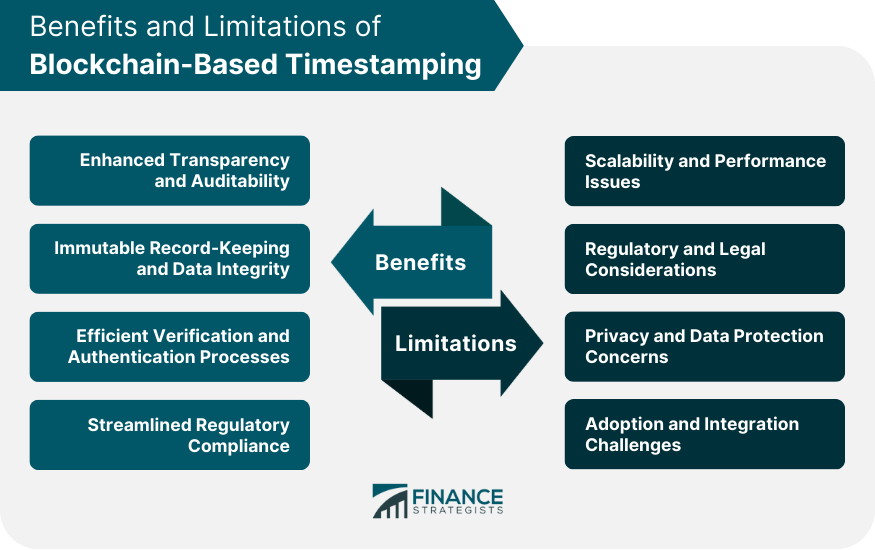

Benefits of Blockchain-Based Timestamping

Enhanced Transparency and Auditability

Immutable Record-Keeping and Data Integrity

Efficient Verification and Authentication Processes

Streamlined Regulatory Compliance

Limitations of Blockchain-Based Timestamping

Scalability and Performance Issues

Regulatory and Legal Considerations

Privacy and Data Protection Concerns

Adoption and Integration Challenges

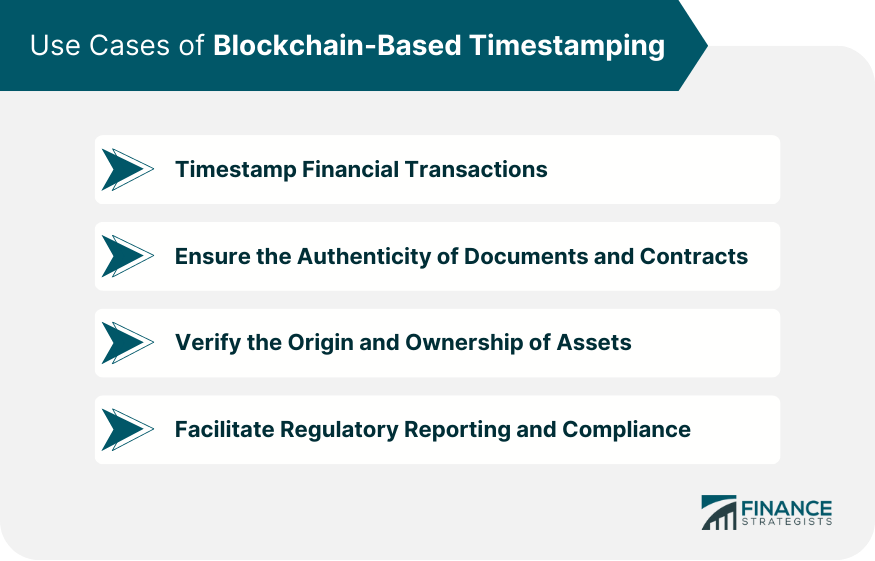

Use Cases of Blockchain-Based Timestamping

Timestamping Financial Transactions

Ensuring the Authenticity of Documents and Contracts

Verifying the Origin and Ownership of Assets

Facilitating Regulatory Reporting and Compliance

Conclusion

Blockchain-Based Timestamping FAQs

Blockchain-based timestamping is a method that uses blockchain technology to verify the exact time and date at which a certain digital event occurred. It provides a secure, verifiable, and tamper-proof timestamp for data, documents, and transactions.

The security of blockchain timestamps is grounded in its distributed, decentralized architecture and the use of cryptographic mechanisms. The data in a blockchain is hashed and added to a block, which is then linked to the previous block in a chronological chain. This structure, combined with the consensus mechanisms, ensures the accuracy and immutability of blockchain timestamps.

Blockchain-based timestamping enhances transparency and auditability, ensures immutable record-keeping and data integrity, facilitates efficient verification and authentication processes, and streamlines regulatory compliance.

Some limitations of blockchain-based timestamping include scalability and performance issues, regulatory and legal uncertainties, privacy and data protection concerns, and adoption and integration challenges.

In finance, blockchain-based timestamping can be used to timestamp financial transactions, ensuring the authenticity of documents and contracts, verifying the origin and ownership of assets, and facilitating regulatory reporting and compliance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.